Automated digital workflows require document collection, eForms, eSignatures, and T&C consent in order to stay compliant with stringent KYC requirements. Unfortunately, many banks still rely on cumbersome and manual processes — all leading to prolonged time to funding, missed opportunities, and damaged NPS.

eKYC promises to reduce the KYC paperwork burden. But it’s not enough to just go digital. To eliminate ambiguity, speed up processes, and ensure compliance, banks need to switch to digital loan workflows.

With automated workflows, bankers are instantly aware of which customers need which forms based on variables like risk profile and loan type. This makes it easier for bank employees to stay compliant without sacrificing efficiency.

Why Should Banks Automate Loan Workflows?

The Challenge: Staying Compliant WIth Changing KYC Requirements

KYC and AML requirements are frequently changed, which means that banks need to keep their lending processes up-to-date. Failure to do so can leave banks vulnerable to loan fraud and defaulting.

The penalties for compliances lapses are great: In 2019 alone, banks worldwide were fined $10 billion for non-compliance with AML, KYC, and sanctions regulations. And these penalties are growing by the year, despite banks scrambling to keep up.

In fact, regulatory change was reported as the top regulatory challenge of the year, according to a 2020 report by Thomson Reuters. Survey respondents also anticipated more information to be published by regulators within the next 12 months.

Yet even as banks are bracing for tougher regulatory demands, they are not planning on hiring more compliance staff in response. Only 34% of banks in the recent survey expect to grow their compliance teams in the coming year, compared to 43% who expected their compliance teams to expand in 2018.

The takeaway is clear: today’s bank executives expect to be able to do more with less. Banking technology allows banks to stay compliant with less employee overhead. It can also allow banks to easily adapt to changing regulations — addressing the number one challenge of today’s banks.

But not any banking technology will do. For example, traditional business process management (BPM) tools require development and IT involvement every time a loan process needs to be tweaked. This prevents banks from quickly updating processes to reflect new regulations and business demands.

Traditional solutions also fail to accommodate the complexity of loan originations. These tools aren’t able to identify all the needed steps and chart a complete workflow before approval is granted. And it’s not just agents who struggle when they are forced to scramble to pinpoint precisely what is required during the current or next step.

Customers, too, suffer from ambiguous and opaque processes, both when in the middle of a task and during the transition to the next task. This lack of visibility negatively impacts NPS and can lead to application abandonment.

Even if the applicant ends up completing the loan process, they will remember whether the bank served them efficiently or not — and this will influence their choices next time they need to take out a loan. According to Raddon Research, nearly 40% of small businesses choose a lender at least partly based on anticipated “speed of approval.”

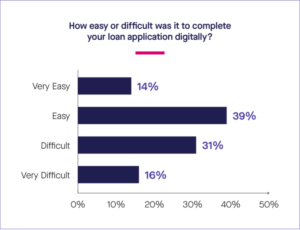

Currently, banks aren’t providing sufficiently streamlined loan processes. A recent Lightico study found that 47% of borrowers felt it was either “difficult” or “very difficult” to apply for a loan during the coronavirus pandemic.

The good news is that with today’s banking technology, banks no longer have to choose between staying compliant and staying efficient.

The Solution: No-Code Business Process Automation Software

Unlike older types of software, no-code business process automation requires zero IT involvement. It allows banks to adjust servicing workflows on the fly in response to changing business and regulatory needs. And given an unpredictable regulatory environment and growing customer demands for streamlined processes, agility is a priority for most banks.

Workflows make it easy for customers to complete and submit:

Personal information (e.g., addresses, tax returns)

Financial statements (e.g., balance sheets, cash flow statements, income statements)

Here are some of the greatest benefits of automating the full customer loan origination and modification process:

Simplified processes: A single system controls the entire loan cycle process with a simple drag-and-drop interface.

Streamlined processes: Easy and intuitive conditional rules can be set to ensure business logic at every stage of the loan process.

Digital tools in one digital suite: At various stages of the workflow, rules trigger the sending of requests for loan application/modification forms, documents, eSignatures, and photo ID, as well as sharing disclosures such as T&Cs for customer approval.

Optimized: Each interaction can be optimized across touchpoints and existing systems.

More visibility: Digital workflows come with dashboards that allow bank leaders to gain visibility into the KPIs that matter most, such as average time to funding and loan application completion rate.

Zero coding required: Admins adjust the business rules according to their needs without requiring IT support or coding.

Seamless integration: The workflow can be a standalone or seamlessly integrated into the bank’s core system via APIs.

7 Key Elements For Automating Loan Originations and Modifications

Automated digital workflows for banking trigger requests for new customer information or action based on the account type (e.g., commercial vs. retail), risk profile, and number of account holders.

Bank employees can instantly request the relevant documents and ID, generate pertinent forms, and send T&Cs. In addition, there are options for self-service. Admins can quickly make modifications to any of these steps without the need for coding.

These workflows can all be carried out digitally through collaboration between the bank employee’s console and the customer’s mobile phone or computer.

Here are seven workflow functionalities that correspond with key bank loan requirements:

1. ID Verification

Before bankers can collect financial statements and accept a loan application, they must verify the customer’s government-issued ID. This is easy to do as part of a digital workflow.

The next generation of ID verification uses facial recognition to confirm a person really is who they claim to be. To determine the authenticity of a person’s claimed identity, the customer must send two images: a snapshot of their photo ID, and a selfie taken in live mode. The customer can also be asked to hold the ID in their hand as they take the selfie for added authenticity.

These are the steps involved in ID verification during a loan origination workflow:

The customer takes a picture of their photo ID, and then a selfie using live mode.

The customer uploads both images — the selfie and photo ID — to the interactive digital session.

An AI algorithm scans the two photos, and a match is confirmed or denied.

Additional security measures such as one-time passwords and knowledge-based authentication (KBA) can also be used to augment the ID verification process.

2. KYC Document Gathering

Automated digital workflows make it easy to collect customer documents using conditional logic and business rules.

KYC questionnaires allow banks to understand the customer’s risk profile, assets, and credit history. Based on the information gathered, the banker can request the exact documents needed during a single phone call.

For example, compliance requirements may demand that banks collect different supporting documents from higher-risk clients, business clients, or for certain loan types (e.g, secured loans vs. unsecured loans).

All of this can be set up in the admin’s console and instantly deployed to bank representatives, ensuring an efficient and personalized loan process.

A typical document collection procedure works as follows:

Formulas built into the workflow allow the admin to determine which document requests are sent to which customers.

The appropriate documents are requested from the customer.

The customer snaps smartphone pictures of their documents, which are automatically sent to the banker for review.

3. Smart Client Loan Application eForms

Smart eForms based on conditional logic allow bankers to generate dynamic, highly relevant loan forms for their retail and commercial bank customers. Fields only appear when a customer ticks a checkbox or selects a particular option from a dropdown, indicating that a specified condition is met.

Here is a typical process for setting up smart forms based on conditional logic:

Create a rule for the trigger field. (E.g., If the customer selects “Employed” under the drop-down list “Employment Status,” then another field will appear asking for the applicant’s monthly income).

Select which additional fields to show if the customer’s response in the trigger field complies with the rule (the fields can be of any type: checkboxes, radio buttons, dropdowns, or text responses can all trigger a conditional workflow).

Create additional rules for a trigger field based on the customer’s response. (E.g., If the loan amount requested exceeds X% of the customer’s monthly income, then additional fields requesting a guarantor’s details will appear).

If needed, a request for an eSignature is also triggered once the form is completed.

By showing and hiding fields depending on the customer’s responses, applicants can get pre-approved faster, form completion time is reduced, and the likelihood of errors or blank fields is reduced.

In addition to streamlining the in-form process, logic can be applied to determine if a form needs to be presented based on the customer inputs on previous forms or in an API.

4. Single-Page Terms and Conditions (T&Cs)

The details of what appears in terms and conditions (T&Cs) may vary based on the account type or loan type. While it’s possible to save every T&C document in a separate PDF template, this needlessly prolongs the loan application process.

With automated digital workflows, there is no need for bankers to manually search for the right T&C template.

Using dynamic documents, bankers can create multiple sections on the same HTML document, add a section for each T&C paragraph, mark those paragraphs as objects, and apply conditions on them.

This allows bankers to send a single dynamic document that includes all the T&Cs straight to the customer’s cell phone for approval.

Here is how the disclosure procedure works:

The workflow automatically generates a T&C based on the loan terms, such as APR, length of loan term, and responsibility of joint account holders (if applicable).

The T&C PDF or web form appears on the customer’s cell phone, where they can read it and check the approval checkbox.

The banker is instantly notified of the customer’s approval.

5. Digital Self-Service

In contrast to mortgage applications, applying for and modifying personal loans tends to be more straightforward. Therefore, banks should give customers the option of applying for personal loans and modifying loan terms from within an email body or website.

This can significantly boost application and modification completion rates, as it eliminates practically all friction in the lending process. And by allowing customers to apply for loans or modify personal information online, banks can save on the manpower and processing costs associated with speaking with a banker on the phone.

Self-service workflows also instantly populate the information of existing customers into forms, allowing them to complete tasks without having to repeat already-known personal details.

A typical self-service experience can look like this:

Customer goes to the bank’s webpage or calls into an IVR, and a lending form appears (e.g., loan application, loan modification, loan deferral).

If the customer already exists in the system, the digital form is pre-populated with their existing details, so they only have to fill out new details.

6. Customizable User Interface

No matter where customers start their process from, whether it’s the bank’s mobile app, website, or simply text message, the look and feel of the portal should reflect the bank’s brand.

Here are a few things banks can do to easily customize their user interface and functionalities:

Add images sized to HTML templates and font colors.

Change the color of the templates.

Push data to the workflow via URL or API.

Build and manage hundreds of workflow URLs.

Redirect to a page when the workflow is completed, or notify the parent window that the workflow is complete.

7. Dynamic Product Selection

Once the customer has applied for or modified a loan, there are still opportunities to continue the customer relationship. Banks can take the invaluable customer data gained during the loan application process (e.g., risk profile, assets, history, account type, loan type), and use it to automatically generate recommendations for other products and services like savings, investments and other loan products.

For example, if a customer requests a payday loan, then the bank can automatically generate a recommendation to join an overdraft protection plan. Or if the customer applies for engagement ring financing, then the bank automatically recommends taking out a wedding loan. The possibilities for automated personalization are endless.

Seamless Client Lending Starts With Business Process Automation

Automated digital workflows help banks dynamically build and adjust processes to meet constantly changing business and regulatory demands. Conditional workflows allow bankers to breeze through the process with low-risk loans and collect more KYC and AML collateral for higher-risk loans.

The capacity to tailor lending workflows to different account and loan types ensures that banks find the optimal balance between compliance and speedy lending. Automated workflows are built on the premise that each banking customer fits a unique profile, and lending processes should reflect that.

Lightico offers such a business process automation solution that uses conditional logic to streamline end-to-end bank lending processes. The platform includes eSignatures, smart eForms, digital T&Cs, self-service, and many more capabilities. Learn more at Lightico.com.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

The good news is that with today’s banking technology, banks no longer have to choose between staying compliant and staying efficient.

The good news is that with today’s banking technology, banks no longer have to choose between staying compliant and staying efficient.