Report Reveals How Banks Have Managed New Loans Over the COVID-19 Period

By Leor Melamedov

As in most areas of life, the COVID-19 pandemic has shone a light on what’s working and what’s not at banks across America. Specifically, the pandemic led to a surge in new loan activity, showing banks’ strengths and weaknesses in the loan application process.

A new survey conducted by Lightico surfaced these strengths and weaknesses based on customers’ responses, revealing how banks measure up against growing expectations for a fully remote and digital experience.

Read till the end for two interactive experiences just for CBA members, where your bank’s lending process will be put to the test.

Lending is lucrative but has high digital friction

The loans granted by U.S. commercial banks in May 2020 amounted to approximately $14.88 trillion USD. Given that one of the primary ways banks make a profit is through interest, it’s critical that financial institutions ensure the maximum number of businesses and individuals successfully take out loans.

The coronavirus represented an unprecedented opportunity to give banking customers the loans they so desperately needed. Yet a recent Lightico survey of 1,006 Americans found that many Americans struggled to take out their most recent loan during the crisis. While loan issues are sometimes related to a person’s qualifications, the data here reflected missed opportunities due to the friction of the loan process itself.

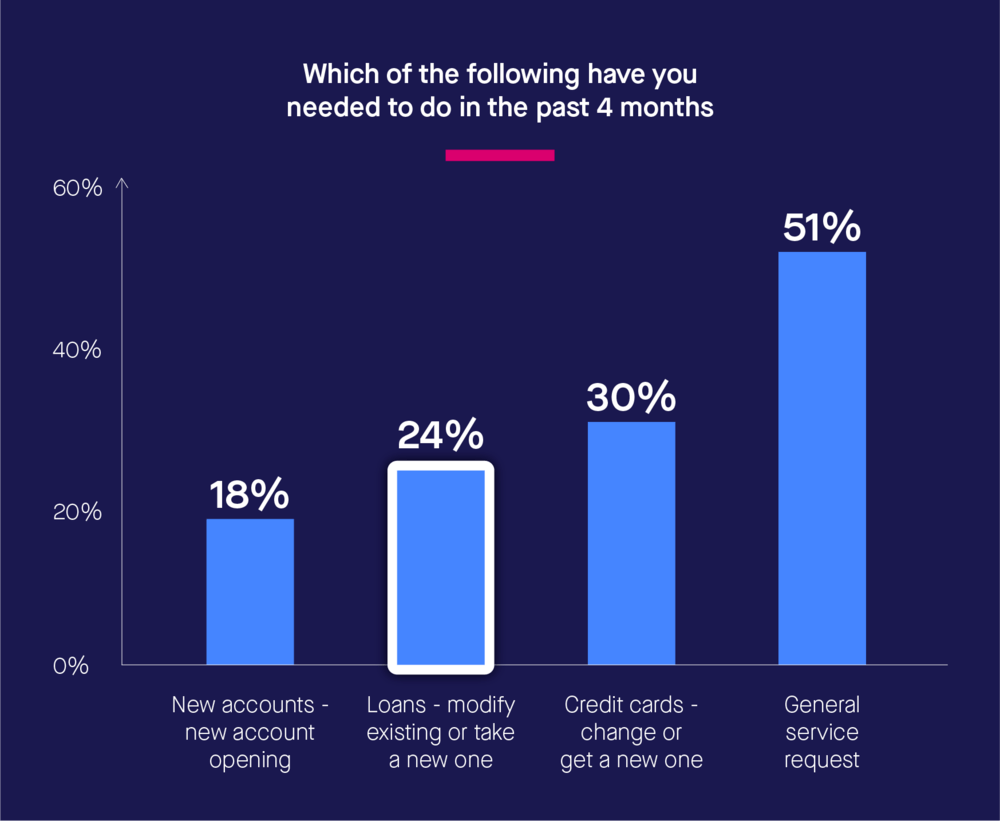

24% of respondents said they have either modified an existing loan or taken out a new one in the past four months –– representing a very high proportion of all banking customers and consequently deserving of our attention.

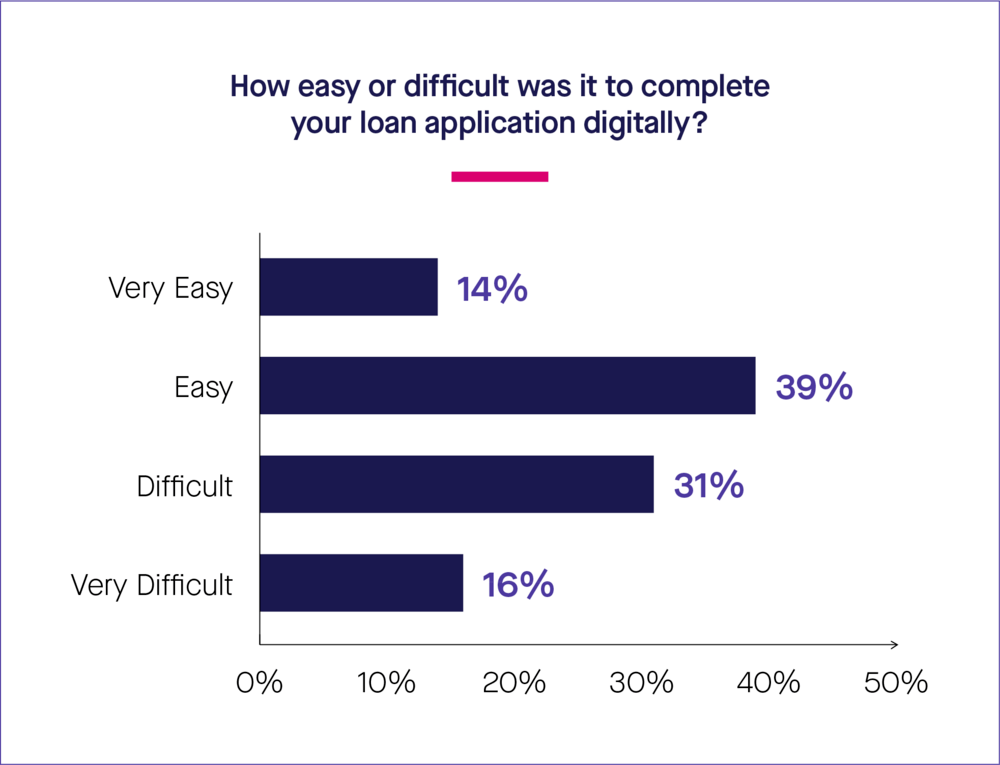

Across all banks, of those who applied for a loan during this period, 47% found the process to be either “difficult” or “very difficult” to undertake digitally. In contrast, a significantly lower proportion of consumers said they found it difficult to complete general service requests online.

This is concerning because it suggests that banks’ efforts to encourage digital banking during the Great Lockdown did not extend to all areas of banking equally. Given that loans can be a matter of great urgency for customers, and a source of great opportunity for the banks who give them, a smoother digital journey would have been beneficial to customers and lucrative for banks.

Evaluation for CBA Members: How did your bank’s loan process fare during COVID-19?

What are the bumps in the digital lending road?

The survey asked additional questions that revealed what exactly customers struggled with during their digital loan application process. 32% of customers who attempted to complete a banking process online were redirected to a branch. And a similar number (33%) said they were “asked to print, sign, and email/fax papers” during what they expected to be a purely digital banking interaction.

So while digital banking continuity has improved, there is still work to be done in this area.

The lack of a fully digital loan process is troubling considering that nearly 50% of customers said that they would forgo taking out a loan if it required coming into a physical branch. This represents a huge loss of income for digitally lagging banks, whose customers are likely to find another bank that does provide an easy way to apply for loans remotely.

Why digital loans matter — and not just as a stopgap

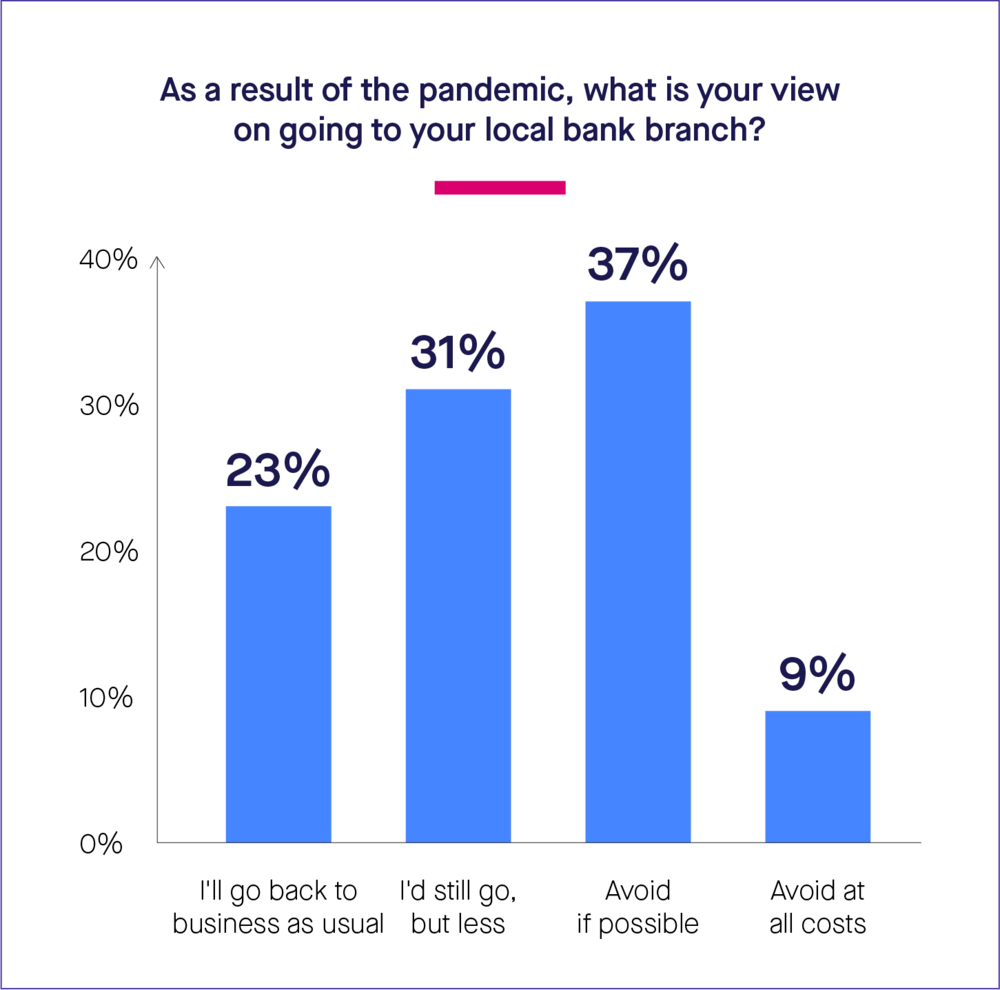

Much of the current resistance to taking out loans at a branch can be chalked up to concerns about the continued spread of the coronavirus. Fears of virus transmission are still keeping customers reticent about spending time in enclosed spaces with other people. But banks shouldn’t conclude that all they have to do is wait for the coronavirus to pass, and customers will want to go back to taking out loans at a physical branch.

The survey found that a mere 23% of consumers think they’ll go back to “business as usual” and continue to visit their bank branch regularly as things open up again, while 46% would avoid it if possible or at all costs going to the bank branch. It may be that physical branches have a diminished role to play in the future of banking transactions. What’s certainly clear is banks that choose to invest in fully digital journeys today will reap the benefits of that investment long after the virus has faded.

In fact, a smooth digital loan process (or the lack of one) can make or break a customer’s loyalty. When Lightico asked banking customers what would get them to change banks, 67% cited “better remote or digital offerings” or “better customer service.” Furthermore, the data showed a strong correlation between high digital ability and customer satisfaction and loyalty.

Safety concerns may have led banking customers to demand more and better digital services, but the newly discovered convenience factor is likely to keep demand for digital high. Remember, many Americans, particularly older generations, only had their first real taste of digital banking during the pandemic. This has significantly increased their comfort levels with it as they experienced a more efficient alternative to traditional banking.

The banks that get digital lending right

The good news is that many banks are getting digital loan applications right — even if there is room for improvement at other institutions.

For instance, banks across the country successfully switched from manual to automated processes to ensure PPP loans were quickly deployed to qualified small businesses. They were able to make this change in record time, allowing those businesses to continue to employ people and serve their communities.

Other banks focused on overhauling their front end to ensure a frictionless and remote lending experience. For example, early on in the pandemic, Happy State Bank created a unique URL for loan deferrals that customers could apply to through a mobile-optimized form. This allowed customers to complete their entire loan modification process from the safety and comfort of their homes.

Consumers are demanding full digital journeys with their banks, an expectation that has skyrocketed since the pandemic began. This calls for digital frontend solutions that are easy to implement and easy for agents and customers to use.

Experience for yourself how frictionless digital-first loan originations and servicing can be. Try this interactive mobile experience, and let us know what you think:

The bottom line

The coronavirus has revealed that while banks have successfully enabled digital transactions for many everyday tasks, lending is still an area that suffers from broken digital journeys. Yet customers are taking out and modifying loans at higher levels than before, making this a prime time for banks to stand out by offering streamlined, fully remote lending options.

Efficient banking experiences can make or break conversions and loyalty. This by now is evident. As customer interest in remote banking keeps surging, the time has come to prioritize digitization for all banking activities.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

The loans granted by U.S. commercial banks in May 2020 amounted to approximately $14.88 trillion USD. Given that one of the primary ways banks make a profit is through interest, it’s critical that financial institutions ensure the maximum number of businesses and individuals successfully take out loans.

The coronavirus represented an unprecedented opportunity to give banking customers the loans they so desperately needed. Yet a recent Lightico survey of 1,006 Americans found that many Americans struggled to take out their most recent loan during the crisis. While loan issues are sometimes related to a person’s qualifications, the data here reflected missed opportunities due to the friction of the loan process itself.

24% of respondents said they have either modified an existing loan or taken out a new one in the past four months –– representing a very high proportion of all banking customers and consequently deserving of our attention.

The loans granted by U.S. commercial banks in May 2020 amounted to approximately $14.88 trillion USD. Given that one of the primary ways banks make a profit is through interest, it’s critical that financial institutions ensure the maximum number of businesses and individuals successfully take out loans.

The coronavirus represented an unprecedented opportunity to give banking customers the loans they so desperately needed. Yet a recent Lightico survey of 1,006 Americans found that many Americans struggled to take out their most recent loan during the crisis. While loan issues are sometimes related to a person’s qualifications, the data here reflected missed opportunities due to the friction of the loan process itself.

24% of respondents said they have either modified an existing loan or taken out a new one in the past four months –– representing a very high proportion of all banking customers and consequently deserving of our attention.

Across all banks, of those who applied for a loan during this period, 47% found the process to be either “difficult” or “very difficult” to undertake digitally. In contrast, a significantly lower proportion of consumers said they found it difficult to complete general service requests online.

This is concerning because it suggests that banks’ efforts to encourage digital banking during the Great Lockdown did not extend to all areas of banking equally. Given that loans can be a matter of great urgency for customers, and a source of great opportunity for the banks who give them, a smoother digital journey would have been beneficial to customers and lucrative for banks.

Across all banks, of those who applied for a loan during this period, 47% found the process to be either “difficult” or “very difficult” to undertake digitally. In contrast, a significantly lower proportion of consumers said they found it difficult to complete general service requests online.

This is concerning because it suggests that banks’ efforts to encourage digital banking during the Great Lockdown did not extend to all areas of banking equally. Given that loans can be a matter of great urgency for customers, and a source of great opportunity for the banks who give them, a smoother digital journey would have been beneficial to customers and lucrative for banks.

Evaluation for CBA Members: How did your bank’s loan process fare during COVID-19?

Evaluation for CBA Members: How did your bank’s loan process fare during COVID-19? Evaluation for CBA Members: How did your bank’s loan process fare during COVID-19?

Evaluation for CBA Members: How did your bank’s loan process fare during COVID-19? Much of the current resistance to taking out loans at a branch can be chalked up to concerns about the continued spread of the coronavirus. Fears of virus transmission are still keeping customers reticent about spending time in enclosed spaces with other people. But banks shouldn’t conclude that all they have to do is wait for the coronavirus to pass, and customers will want to go back to taking out loans at a physical branch.

The survey found that a mere 23% of consumers think they’ll go back to “business as usual” and continue to visit their bank branch regularly as things open up again, while 46% would avoid it if possible or at all costs going to the bank branch. It may be that physical branches have a diminished role to play in the future of banking transactions. What’s certainly clear is banks that choose to invest in fully digital journeys today will reap the benefits of that investment long after the virus has faded.

In fact, a smooth digital loan process (or the lack of one) can make or break a customer’s loyalty. When Lightico asked banking customers what would get them to change banks, 67% cited “better remote or digital offerings” or “better customer service.” Furthermore, the data showed a strong correlation between high digital ability and customer satisfaction and loyalty.

Safety concerns may have led banking customers to demand more and better digital services, but the newly discovered convenience factor is likely to keep demand for digital high. Remember, many Americans, particularly older generations, only had their first real taste of digital banking during the pandemic. This has significantly increased their comfort levels with it as they experienced a more efficient alternative to traditional banking.

Much of the current resistance to taking out loans at a branch can be chalked up to concerns about the continued spread of the coronavirus. Fears of virus transmission are still keeping customers reticent about spending time in enclosed spaces with other people. But banks shouldn’t conclude that all they have to do is wait for the coronavirus to pass, and customers will want to go back to taking out loans at a physical branch.

The survey found that a mere 23% of consumers think they’ll go back to “business as usual” and continue to visit their bank branch regularly as things open up again, while 46% would avoid it if possible or at all costs going to the bank branch. It may be that physical branches have a diminished role to play in the future of banking transactions. What’s certainly clear is banks that choose to invest in fully digital journeys today will reap the benefits of that investment long after the virus has faded.

In fact, a smooth digital loan process (or the lack of one) can make or break a customer’s loyalty. When Lightico asked banking customers what would get them to change banks, 67% cited “better remote or digital offerings” or “better customer service.” Furthermore, the data showed a strong correlation between high digital ability and customer satisfaction and loyalty.

Safety concerns may have led banking customers to demand more and better digital services, but the newly discovered convenience factor is likely to keep demand for digital high. Remember, many Americans, particularly older generations, only had their first real taste of digital banking during the pandemic. This has significantly increased their comfort levels with it as they experienced a more efficient alternative to traditional banking.