Banking Professionals’ Survey Uncovers Futile Mobile Banking – & How to Fix It

By Gaby Young

Speed is becoming the key competitive differentiator for banks and financial institutions to onboard and delight customers who are constantly on-the-go and juggling busy work and personal lives.

This means catching up with them from wherever they are and on the device that’s with them 24/7 - their mobile smartphone: 85% of Americans today own a smartphone, and 57% spend 5 hours or more on them every day.

Intuitive, simple and fast banking experiences have become the expectation for these consumers - be they signing up for a new account, applying for a loan, or looking for a quick resolution on a service issue. This new digital reality has been rapidly accelerated since the Covid-19, with a post-pandemic survey showing that 79% of customers want their bank to provide them with more all-digital processes, while 55% plan to visit branches less often in the future.

Mobile Banking Critical to Fulfilling Customers’ Need for Speed

Fintech services like Nerdwallet and neobanks like Dave are a couple of many digital challengers that have invaded the banking industry, focusing on bringing consumer demand for Amazon-like ease and speed by enabling not just onboarding and self-service options, but also the ability to process loans and high-value transactions.

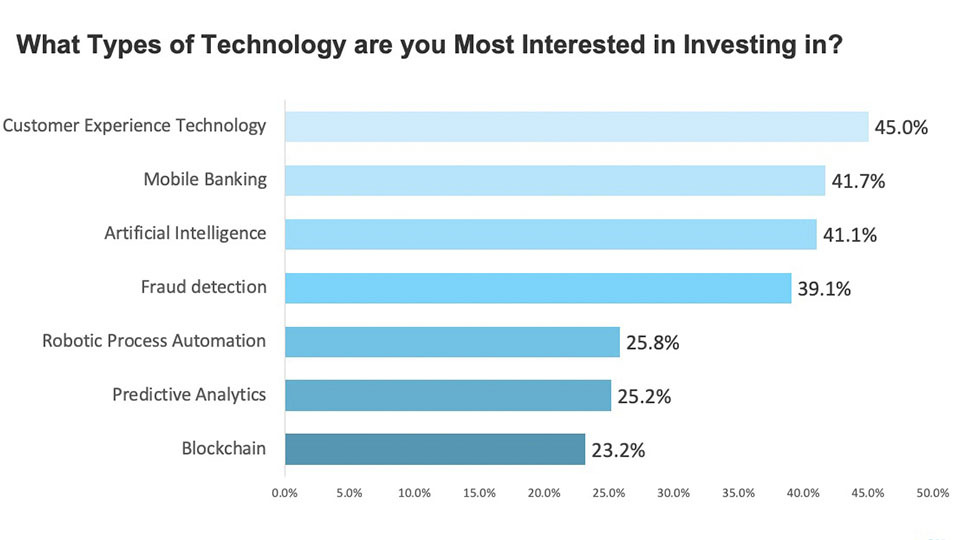

To compete, traditional banks are acutely aware of the need to answer this challenge - and the call from customers. It’s no wonder that customer experience technology and mobile banking topped the priority list in our recent survey of banking professionals across national and community banks and credit unions.

Indeed traditional banks have invested substantial time and money into multiple point solutions to help accelerate loan originations and servicing.

But are these investments paying off?

Customers Still Being Forced to the Branch Despite Mobile Banking Investments

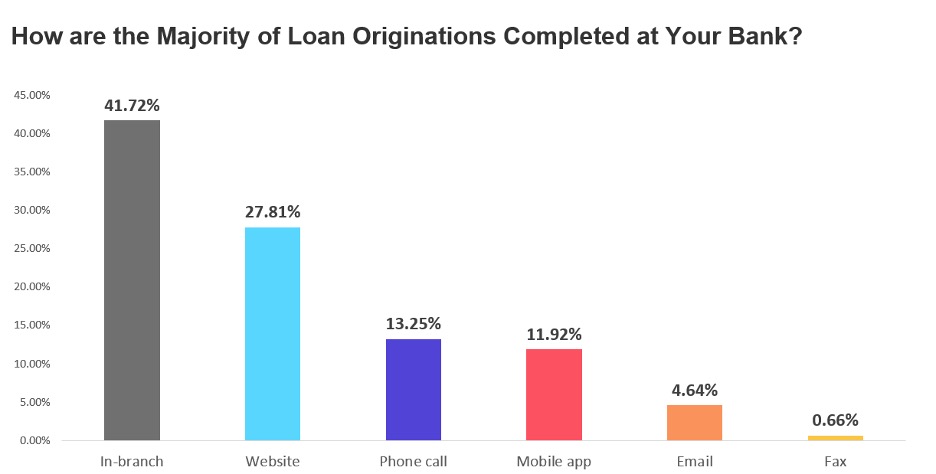

Despite all of the investments poured into digital banking and mobile app projects, only 11% of banking professionals indicated that this is the main way they are processing new loans, while just 27% said they can complete new loans via their website. For the majority, completing loans still requires the customer to make the trip to the branch.

Just as troubling? Customers can’t have their request to open a new loan resolved via a mobile. Only 4% of professionals state that all of their loan originations process can be completed from their bank’s mobile app.

Even for comparatively simpler servicing requests such as change of address or adding a cosigner, just 11% indicated their mobile apps can resolve those requests.

Low Mobile Adoption Means Slow Completion Times for Banks

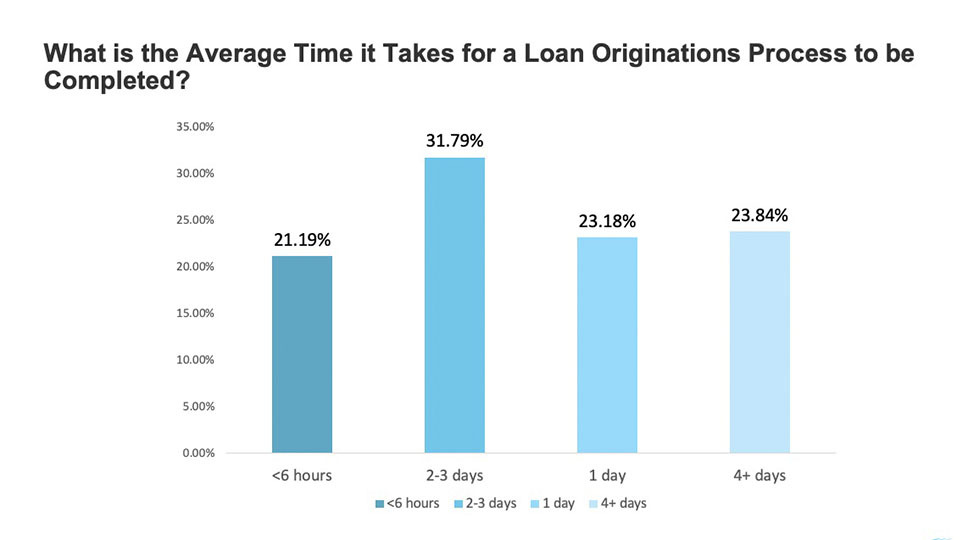

Mobile adoption is so inseparable to quick completion times - and the absence of this was also reflected by banking professionals when asked how long it takes their bank to process new loans. The vast majority, over 55%, shared that completing a loan origination process takes them 2 or more days. Only 21% are able to process loans for new customers in 6 hours or less.

Mobile Apps Fail to Reduce Touchpoints & Customer Frustration

Days-long processes try the patience of customers today - especially with so many viable digital alternatives. So do high-effort interactions that force them to engage with multiple touchpoints just to become a new customer or open a loan.

Yet despite banks’ digital investments being bounced across several channels is still the customer experience norm. A leading 44% of banking professionals indicate that 3-4 touchpoints are required to complete the loan origination process, with a further 33% requiring 5 or more. Just 21% said loans can be processed in 1-2 days.

Multiple touchpoints generate work and friction for banking customers and employees alike and stand in the way of financial institutions’ ability to deliver on their customers’ needs quickly and efficiently - risking the loss of these customers to the competition.

But why are they still so necessary despite all of the resources banks have devoted towards rolling out digital channels and mobile banking apps?

Digital Silos & Legacy Processes Doom Banks to Friction-Filled Customer Interactions

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Indeed traditional banks have invested substantial time and money into multiple point solutions to help accelerate loan originations and servicing.

But are these investments paying off?

Indeed traditional banks have invested substantial time and money into multiple point solutions to help accelerate loan originations and servicing.

But are these investments paying off?

Just as troubling? Customers can’t have their request to open a new loan resolved via a mobile. Only 4% of professionals state that all of their loan originations process can be completed from their bank’s mobile app.

Even for comparatively simpler servicing requests such as change of address or adding a cosigner, just 11% indicated their mobile apps can resolve those requests.

Just as troubling? Customers can’t have their request to open a new loan resolved via a mobile. Only 4% of professionals state that all of their loan originations process can be completed from their bank’s mobile app.

Even for comparatively simpler servicing requests such as change of address or adding a cosigner, just 11% indicated their mobile apps can resolve those requests.

Marrying these channels with a Digital Completion solution helps banks guide them swiftly through all requirements needed to complete their application - while also giving them live agent support to assist them with any questions they have regarding the terms and conditions of the loan or any specific documents they need to provide to process the application.

Completing every customer-facing action in one seamless mobile session allows banks to eliminate the multiple steps and channels that can be so infuriating for their customers. It also eliminates the frustration and productivity drain of paperwork for employees, enabling them to process loans faster and maximize ROI while cutting costs.

And delivering mobile banking in-tandem with live agent assistance provides a transparent and efficient journey for customers, and gives them the confidence and peace of mind that traditional banks need to boost satisfaction and loyalty.

Marrying these channels with a Digital Completion solution helps banks guide them swiftly through all requirements needed to complete their application - while also giving them live agent support to assist them with any questions they have regarding the terms and conditions of the loan or any specific documents they need to provide to process the application.

Completing every customer-facing action in one seamless mobile session allows banks to eliminate the multiple steps and channels that can be so infuriating for their customers. It also eliminates the frustration and productivity drain of paperwork for employees, enabling them to process loans faster and maximize ROI while cutting costs.

And delivering mobile banking in-tandem with live agent assistance provides a transparent and efficient journey for customers, and gives them the confidence and peace of mind that traditional banks need to boost satisfaction and loyalty.