COVID-19 Survey: Insurance Challenges and Opportunities During Crisis

By Leor Melamedov

The insurance industry is under tremendous pressure from small businesses to pay business interruption insurance –– a difficult if not impossible demand to meet. Policyholders are struggling to keep up with insurance payments. And pressure is rising from seemingly all directions.

Yet results from our latest Covid-19 survey of 1,028 American consumers conducted in mid-May suggests that not all is doom and gloom for insurers. In fact, despite consumers’ increasing financial strain, more people than ever are shopping for insurance policies. And a significant number of existing policyholders are considering purchasing more products and benefits.

The people have spoken: they’re willing to cut back on expenses in practically every area of their life –– except insurance. This means especially during the coronavirus pandemic, insurance companies have a unique opportunity to prove their value to existing customers, and win over new business.

The financial and health impact of COVID-19 is growing

Despite initial signs that we are starting to emerge from the coronavirus, we aren’t out of the woods yet. Far from it. Americans are still reeling from the health and economic impact COVID-19 has had on their lives:

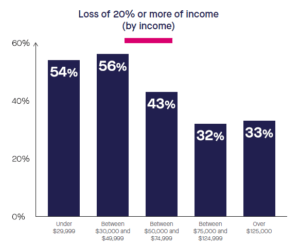

A whopping 47% of customers we surveyed reported a drop of income of 20% or more.

18% reported a loss of 50% or more.

60% of customers are worried about covering household expenses and/or loans in the coming months (up from 51% in March).

While lower-income respondents took the biggest financial hit as a group, higher income earners weren’t spared either:

In addition to consumers’ greater financial burden, they are also grappling with health concerns. The economy may be reopening, but that hasn’t allayed fears surrounding a potential second wave of infections, the uncertain role of antibodies, and mysterious new symptoms that seems to crop up every few weeks.

Thus, it shouldn’t come as a surprise that 78% of consumers surveyed are concerned about running routine errands, such as in-person banking and grocery shopping.

In addition to financial and health concerns, consumers are worried about their insurance coverage. The United States isn’t renowned for its strong social safety net compared to many other Western countries, which perhaps exacerbates policyholders' sense of vulnerability.

Our survey found that:

25% are concerned that they will not be able to take advantage of their employee insurance benefits.

14% are concerned about their ability to pay life-insurance premiums.

17% are concerned about the long-term effects that the coronavirus is having on their annuity contract.

14% are concerned that they’ll be declined coverage because of age/associated risk of COVID-19.

Many of these concerns are financial, which presents an opportunity for insurance companies to proactively offer help like deferred payments while still providing coverage, and extended grace periods for those who’ve already fallen behind. It may not be possible to cover things like business continuity insurance, but insurers can still be their customers’ heroes in other ways.

The crisis has surfaced new insurance needs

Despite customers’ widespread financial concerns, interest in purchasing insurance isn’t going anywhere. In fact, 21% of all consumers are actively searching for new home or auto insurance, and 19% are looking to add more life insurance-related products.

It also seems that consumers who were directly impacted by COVID-19 are twice as likely to increase their spend on property, health, and life insurance. This makes intuitive sense: witnessing or experiencing the fragility of life first-hand makes worst-case scenarios seem less distant, and more real –– which demands risk-reducing action like taking out insurance.

But even consumers who haven’t been directly touched by COVID-19 seem to perceive insurance as indispensable.

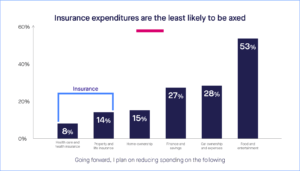

As the graph below demonstrates, insurance expenditures are the least likely to be cut. In fact, customers would sooner reduce spending on home and car ownership –– widely considered essentials –– than on insurance.

The future of insurance sales and servicing? Better digital communication

As we’ve seen, the silver lining for insurers is that customers perceive the product they offer as essential –– and they are willing to pay for it.

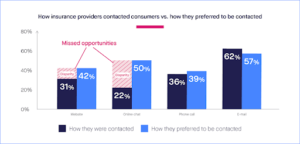

But insurers must improve the way they communicate with existing customers and prospects. As things stand, there is a major gap between how customers prefer to be contacted, and how insurers are actually communicating with them.

Only 34% have been able to easily connect with their insurers to ask questions or make modifications to their policy.

And while consumers are eager to communicate with insurers online, insurers aren’t meeting that need, with 50% behind on consumer demand for online chat servicing and 25% behind on consumer demand for website servicing.

Customers are ready, willing, and able to buy insurance –– but providers must make it easy for them, especially during these remote times when people are still practicing social distancing. Face-to-face sales and inconvenient, non-digital channels such as fax machines and printers are inhibiting potential sales.

Insurers Need to Act Swiftly in This COVID Crisis

Insurance is essential during the pandemic and always, and the good news is that customers see it that way. But there are ample opportunities for insurers to truly cement their existing customers’ loyalty while winning over new deals. It will require anticipating and accommodating consumer financial concerns, and adapting to consumer preferences for communication.

While only insurance companies can help with the former, here at Lightico we can help with the latter. Our remote customer transaction solution allows insurers to collect eSignature, eForms, and eDocuments from policyholders via a simple smartphone link. It has been proven to lower the time to settle a claim by 85%, reduce touchpoints per policy by 60%, and increase customer satisfaction by 15%.

Read the full story here.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

In addition to consumers’ greater financial burden, they are also grappling with health concerns. The economy may be reopening, but that hasn’t allayed fears surrounding a potential second wave of infections, the uncertain role of antibodies, and mysterious new symptoms that seems to crop up every few weeks.

Thus, it shouldn’t come as a surprise that 78% of consumers surveyed are concerned about running routine errands, such as in-person banking and grocery shopping.

In addition to consumers’ greater financial burden, they are also grappling with health concerns. The economy may be reopening, but that hasn’t allayed fears surrounding a potential second wave of infections, the uncertain role of antibodies, and mysterious new symptoms that seems to crop up every few weeks.

Thus, it shouldn’t come as a surprise that 78% of consumers surveyed are concerned about running routine errands, such as in-person banking and grocery shopping.