The coronavirus pandemic surfaced the urgency of expanded digital and remote banking. With this in mind, Lightico conducted a study of US banking and credit union consumers to determine which banks are winning on the digital battleground, and which are lagging behind.

While all banks made adjustments to provide services for their customers during the “Great Lockdown,” consumers’ views on the ease and abilities of the banks differed significantly.

What we found was some very good news for credit unions and local banks. The study revealed that these institutions punched above their weight and are positioned to stay competitive, with rankings similar to digital-only banks and behemoths like Capital One and JPMorgan Chase. Read on to discover what customers really think about their local banks and credit unions.

Study results reveal: Credit unions and local banks are winning at digital transformation

Lightico conducted an anonymous study of 1,007 Americans representing a cross-section of the population. All of the questions were asked within the context of the past four months during the COVID-19 pandemic. Consumers were asked to identify their current bank out of top ten banks in the United States, while “local bank” “credit union” and “digital-only bank” were grouped into three separate options.

The study revealed that credit unions and local banks shine in the areas that characterize a strong bank: ease of account openings, lending experience, and completeness of the digital journey. In most of these areas, they far outpace their richer and larger competitors.

Easy account opening

Recent research by Deloitte found that 40% of consumers have abandoned a bank account opening process in the middle. Most of the time, it was due to too much paperwork and an excessive number of personal questions asked. Losing potential customers before they’ve even onboarded is costly to banks, as all the marketing and sales dollars that were poured into attracting them effectively goes down the drain.

Smooth digital onboarding is perhaps the best way of preventing failure to convert during the onboarding process. After all, a customer that tries to open an account has every intention of doing so. Easy digital onboarding became an especially important issue during the coronavirus, when customers are concerned about having to go into a physical location and potentially expose themselves to the pathogen.

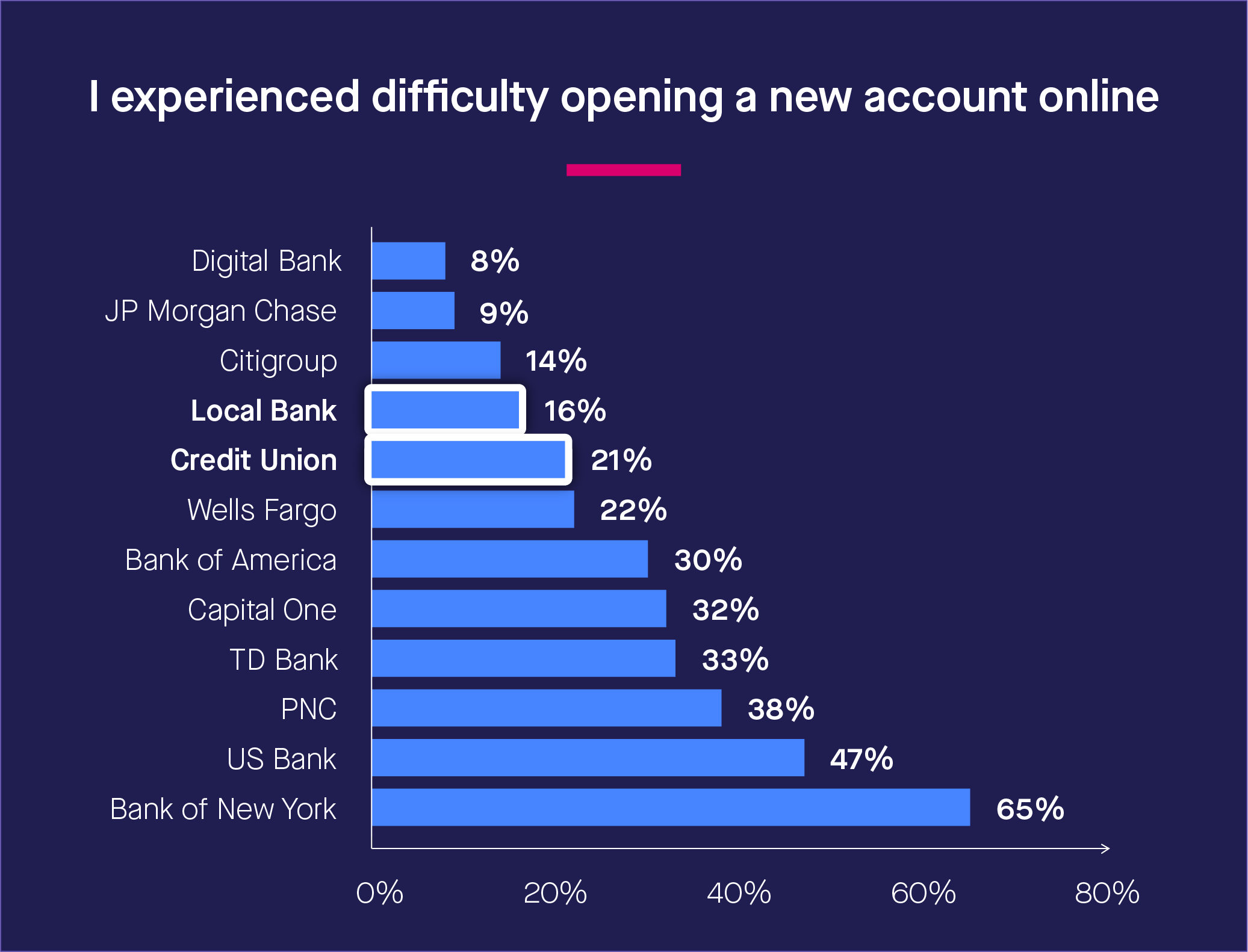

Amazingly, local banks and credit unions were among the leaders of the pack when it came to an easy online account opening process. This is quite an accomplishment seeing as these institutions are sitting on significantly smaller budgets than larger banks.

Obviously, digital banks provided the smoothest online account opening process (only 8% of respondents cited difficulties), but local banks (14%) and credit unions (21%) were also associated with low levels of online onboarding friction and high levels of customer satisfaction with account opening.

There could be many explanations for this success; perhaps customer-focused credit unions and local banks were more in tune with their customers’ needs during the coronavirus. Perhaps the smaller size of these institutions made it easier for them to digitize in a fast and agile way. Whatever the reason, it just goes to show that huge funds aren’t needed to provide customers with the kind of onboarding experience they expect.

2. Smooth online lending experience

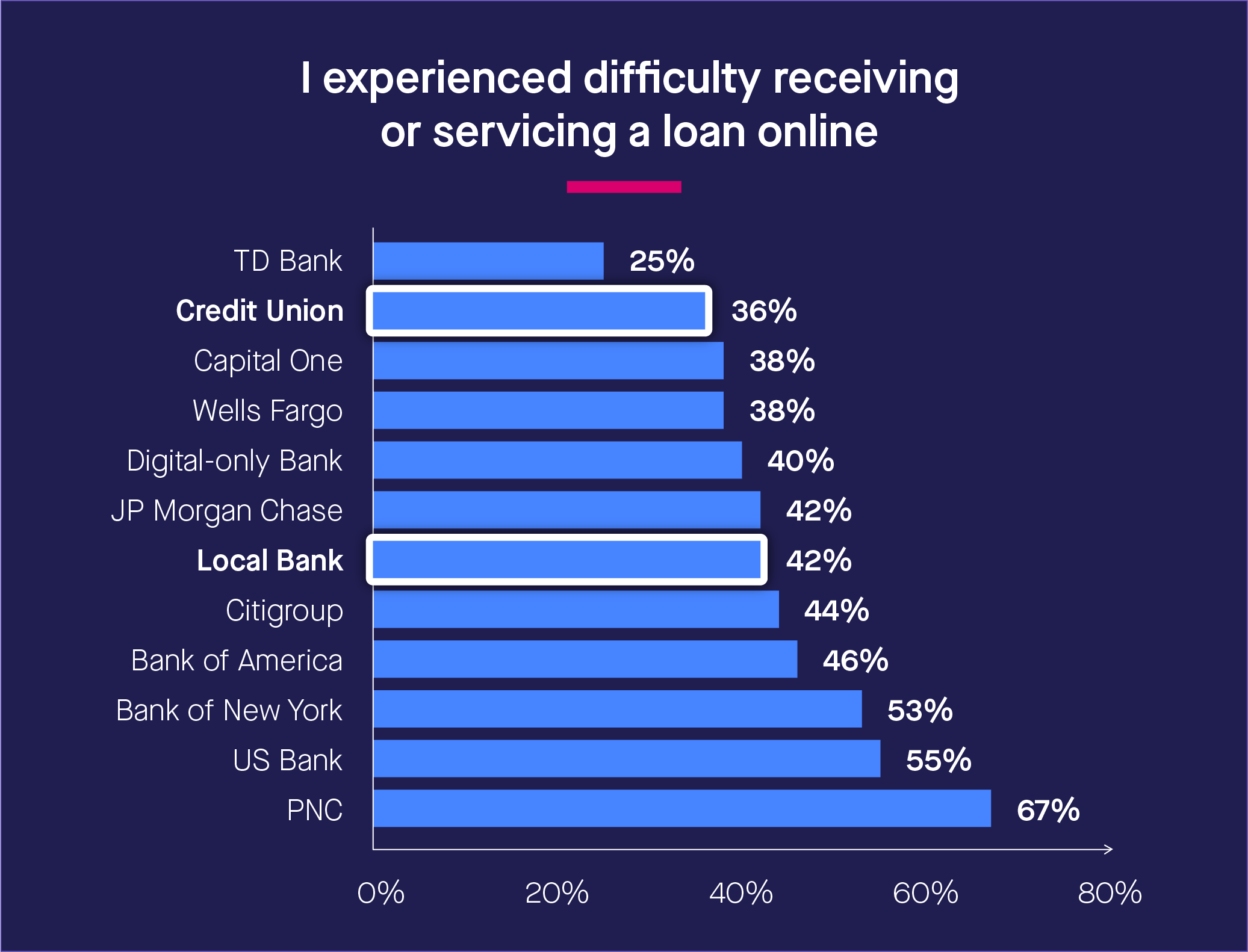

Credit unions ranked at an impressive second place out of 12 banks when it came to ease of online lending experience. Local banks came out in the middle, ranking in seventh place. Considering that 24% of respondents either modified a loan or took out a new loan in the past four months, this is an issue that affected a rather significant number of banking customers.

In the case of local banks (though not credit unions), interest is a critical source of income. So it’s critical to ensure those loans get into customers’ hands. Failure to provide a fully digital loan application process risks those customers taking their business elsewhere.

In fact, almost 50% of banking customers claimed they would pass on taking out a loan if it required them to go to an in-person branch.

The last thing banks want, especially during these economically rocky times, is to miss out on opportunities to provide loans to qualified customers. Fortunately, credit unions and to a lesser extent, local banks are performing well in this area.

3. Complete digital journey

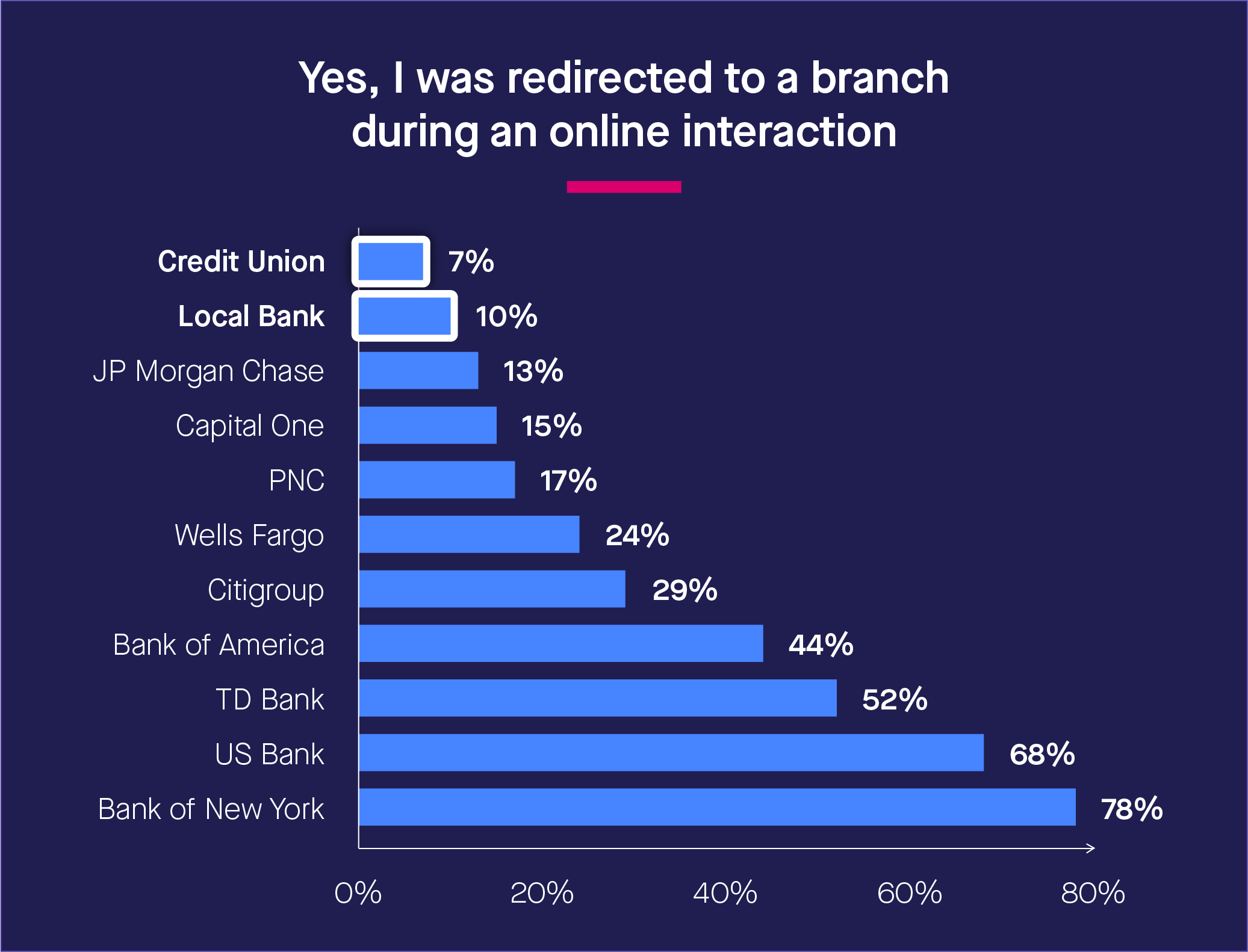

Offering customers a complete digital journey is where credit unions and local banks really shine. Customers of both types of financial institutions report being very satisfied with the completeness of their online journeys for all banking tasks. A mere 7% of credit union customers and 10% of local bank customers said they were “redirected to a branch during an online interaction” sometime in the last four months.

In stark contrast, a significant proportion of large bank customers reported being bounced to a branch while attempting to complete a task online.

During ordinary circumstances, this would be unacceptable. Customers who go online to complete a banking task expect to complete it there; sudden redirection to a physical location is jarring, a source of frustration, annoyance, and confusion.

Yet in the shadow of the “Great Lockdown,” such broken digital journeys are even more upsetting to customers. Banks are not just misleading and inconveniencing them, which is bad enough, but are making them feel uncomfortable in terms of safety due to the continued threat of COVID-19.

Fortunately, customer-centric credit unions and local banks have proven their empathy for their customers yet again by providing truly complete digital journeys.

CUs and local banks are greatly exceeding customers’ great expectations

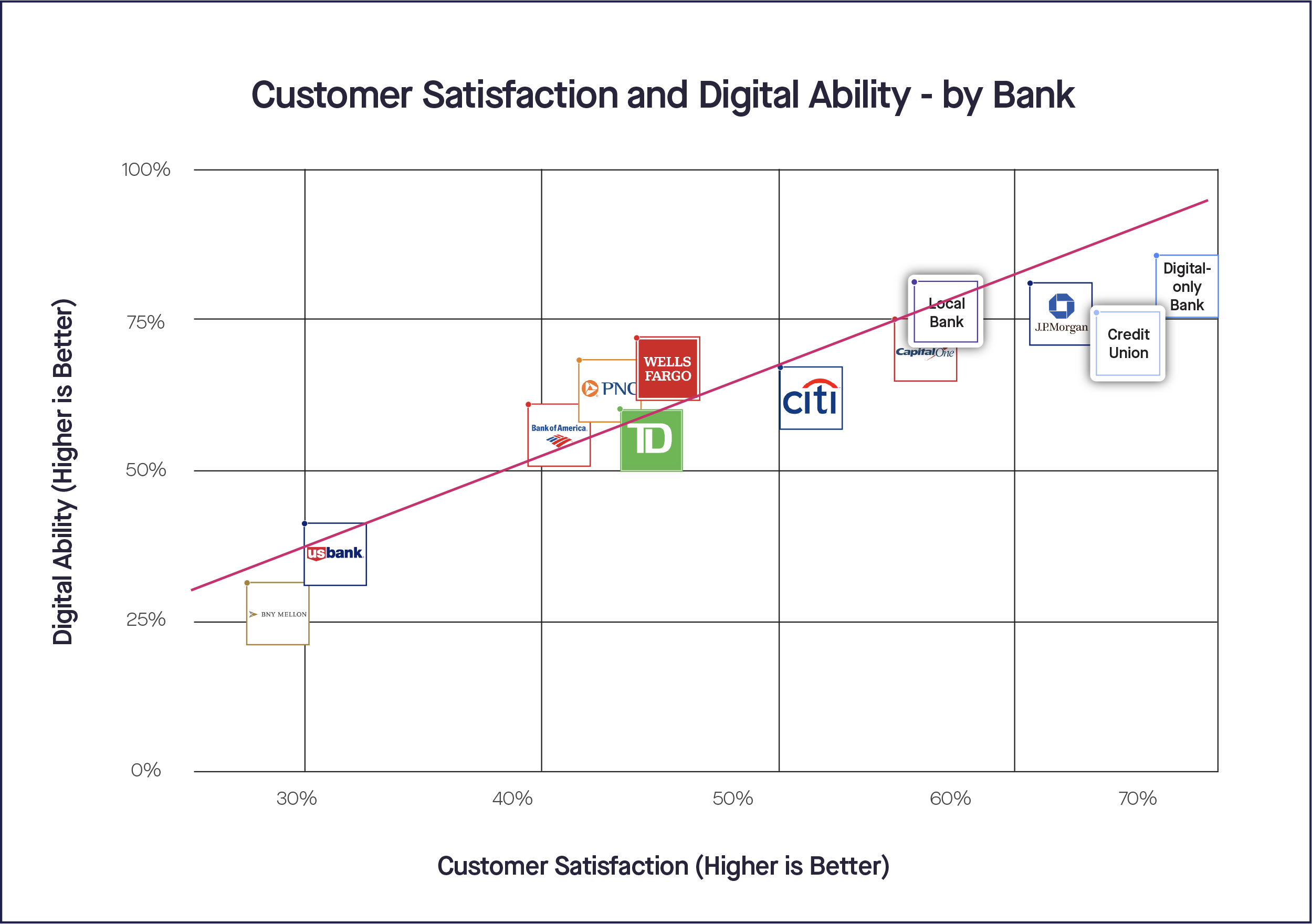

The study allowed us to put together a quadrant graph demonstrating where banks fall across two measures: customer experiencesatisfaction and digital ability.

Customer experience satisfaction was calculated by averaging customers’ ratings of their bank over the past four months and willingness to change banks right now (a signifier of loyalty).

Digital ability was calculated by averaging online interactions that had to be completed at a physical branch or required printing/scanning/faxing/e-mail to complete the journey. It also took into account the difficulty of opening a new account, taking or servicing a loan, and opening a new credit card online during the past four months.

When mapped out, a strong correlation emerged between banks’ CX and digital ability. The chart clearly shows that banks with favorable digital ratings tend to have more loyal and satisfied customers.

Predictably, digital-only banks received the highest scores. But credit unions trailed them only slightly, and local banks performed better than average. This is quite an extraordinary accomplishment, and a testament to credit unions’ and local banks’ commitment to delivering an excellent and digital customer experience.

Conclusion: Digital CX is possible even on a lean budget

Despite smaller budgets and fewer resources, credit unions and local banks have managed to provide their customers with a better digital experience than even the largest national banks. In fact, many traditional national banks disappointed their customers while CUs and local banks cemented their loyalty during this unprecedented period. As we emerge from the “Great Lockdown,” there is no doubt that CU and local bank customers will remember the high-quality, digital experience they received when they needed it most.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Recent research by Deloitte found that 40% of consumers have abandoned a bank account opening process in the middle. Most of the time, it was due to too much paperwork and an excessive number of personal questions asked. Losing potential customers before they’ve even onboarded is costly to banks, as all the marketing and sales dollars that were poured into attracting them effectively goes down the drain.

Smooth digital onboarding is perhaps the best way of preventing failure to convert during the onboarding process. After all, a customer that tries to open an account has every intention of doing so. Easy digital onboarding became an especially important issue during the coronavirus, when customers are concerned about having to go into a physical location and potentially expose themselves to the pathogen.

Recent research by Deloitte found that 40% of consumers have abandoned a bank account opening process in the middle. Most of the time, it was due to too much paperwork and an excessive number of personal questions asked. Losing potential customers before they’ve even onboarded is costly to banks, as all the marketing and sales dollars that were poured into attracting them effectively goes down the drain.

Smooth digital onboarding is perhaps the best way of preventing failure to convert during the onboarding process. After all, a customer that tries to open an account has every intention of doing so. Easy digital onboarding became an especially important issue during the coronavirus, when customers are concerned about having to go into a physical location and potentially expose themselves to the pathogen.

Amazingly, local banks and credit unions were among the leaders of the pack when it came to an easy online account opening process. This is quite an accomplishment seeing as these institutions are sitting on significantly smaller budgets than larger banks.

Obviously, digital banks provided the smoothest online account opening process (only 8% of respondents cited difficulties), but local banks (14%) and credit unions (21%) were also associated with low levels of online onboarding friction and high levels of customer satisfaction with account opening.

There could be many explanations for this success; perhaps customer-focused credit unions and local banks were more in tune with their customers’ needs during the coronavirus. Perhaps the smaller size of these institutions made it easier for them to digitize in a fast and agile way. Whatever the reason, it just goes to show that huge funds aren’t needed to provide customers with the kind of onboarding experience they expect.

Amazingly, local banks and credit unions were among the leaders of the pack when it came to an easy online account opening process. This is quite an accomplishment seeing as these institutions are sitting on significantly smaller budgets than larger banks.

Obviously, digital banks provided the smoothest online account opening process (only 8% of respondents cited difficulties), but local banks (14%) and credit unions (21%) were also associated with low levels of online onboarding friction and high levels of customer satisfaction with account opening.

There could be many explanations for this success; perhaps customer-focused credit unions and local banks were more in tune with their customers’ needs during the coronavirus. Perhaps the smaller size of these institutions made it easier for them to digitize in a fast and agile way. Whatever the reason, it just goes to show that huge funds aren’t needed to provide customers with the kind of onboarding experience they expect.

Credit unions ranked at an impressive second place out of 12 banks when it came to ease of online lending experience. Local banks came out in the middle, ranking in seventh place. Considering that 24% of respondents either modified a loan or took out a new loan in the past four months, this is an issue that affected a rather significant number of banking customers.

In the case of local banks (though not credit unions), interest is a critical source of income. So it’s critical to ensure those loans get into customers’ hands. Failure to provide a fully digital loan application process risks those customers taking their business elsewhere.

In fact, almost 50% of banking customers claimed they would pass on taking out a loan if it required them to go to an in-person branch.

The last thing banks want, especially during these economically rocky times, is to miss out on opportunities to provide loans to qualified customers. Fortunately, credit unions and to a lesser extent, local banks are performing well in this area.

Credit unions ranked at an impressive second place out of 12 banks when it came to ease of online lending experience. Local banks came out in the middle, ranking in seventh place. Considering that 24% of respondents either modified a loan or took out a new loan in the past four months, this is an issue that affected a rather significant number of banking customers.

In the case of local banks (though not credit unions), interest is a critical source of income. So it’s critical to ensure those loans get into customers’ hands. Failure to provide a fully digital loan application process risks those customers taking their business elsewhere.

In fact, almost 50% of banking customers claimed they would pass on taking out a loan if it required them to go to an in-person branch.

The last thing banks want, especially during these economically rocky times, is to miss out on opportunities to provide loans to qualified customers. Fortunately, credit unions and to a lesser extent, local banks are performing well in this area.

Offering customers a complete digital journey is where credit unions and local banks really shine. Customers of both types of financial institutions report being very satisfied with the completeness of their online journeys for all banking tasks. A mere 7% of credit union customers and 10% of local bank customers said they were “redirected to a branch during an online interaction” sometime in the last four months.

In stark contrast, a significant proportion of large bank customers reported being bounced to a branch while attempting to complete a task online.

During ordinary circumstances, this would be unacceptable. Customers who go online to complete a banking task expect to complete it there; sudden redirection to a physical location is jarring, a source of frustration, annoyance, and confusion.

Yet in the shadow of the “Great Lockdown,” such broken digital journeys are even more upsetting to customers. Banks are not just misleading and inconveniencing them, which is bad enough, but are making them feel uncomfortable in terms of safety due to the continued threat of COVID-19.

Fortunately, customer-centric credit unions and local banks have proven their empathy for their customers yet again by providing truly complete digital journeys.

Offering customers a complete digital journey is where credit unions and local banks really shine. Customers of both types of financial institutions report being very satisfied with the completeness of their online journeys for all banking tasks. A mere 7% of credit union customers and 10% of local bank customers said they were “redirected to a branch during an online interaction” sometime in the last four months.

In stark contrast, a significant proportion of large bank customers reported being bounced to a branch while attempting to complete a task online.

During ordinary circumstances, this would be unacceptable. Customers who go online to complete a banking task expect to complete it there; sudden redirection to a physical location is jarring, a source of frustration, annoyance, and confusion.

Yet in the shadow of the “Great Lockdown,” such broken digital journeys are even more upsetting to customers. Banks are not just misleading and inconveniencing them, which is bad enough, but are making them feel uncomfortable in terms of safety due to the continued threat of COVID-19.

Fortunately, customer-centric credit unions and local banks have proven their empathy for their customers yet again by providing truly complete digital journeys.

The study allowed us to put together a quadrant graph demonstrating where banks fall across two measures: customer experience satisfaction and digital ability.

Customer experience satisfaction was calculated by averaging customers’ ratings of their bank over the past four months and willingness to change banks right now (a signifier of loyalty).

Digital ability was calculated by averaging online interactions that had to be completed at a physical branch or required printing/scanning/faxing/e-mail to complete the journey. It also took into account the difficulty of opening a new account, taking or servicing a loan, and opening a new credit card online during the past four months.

When mapped out, a strong correlation emerged between banks’ CX and digital ability. The chart clearly shows that banks with favorable digital ratings tend to have more loyal and satisfied customers.

Predictably, digital-only banks received the highest scores. But credit unions trailed them only slightly, and local banks performed better than average. This is quite an extraordinary accomplishment, and a testament to credit unions’ and local banks’ commitment to delivering an excellent and digital customer experience.

The study allowed us to put together a quadrant graph demonstrating where banks fall across two measures: customer experience satisfaction and digital ability.

Customer experience satisfaction was calculated by averaging customers’ ratings of their bank over the past four months and willingness to change banks right now (a signifier of loyalty).

Digital ability was calculated by averaging online interactions that had to be completed at a physical branch or required printing/scanning/faxing/e-mail to complete the journey. It also took into account the difficulty of opening a new account, taking or servicing a loan, and opening a new credit card online during the past four months.

When mapped out, a strong correlation emerged between banks’ CX and digital ability. The chart clearly shows that banks with favorable digital ratings tend to have more loyal and satisfied customers.

Predictably, digital-only banks received the highest scores. But credit unions trailed them only slightly, and local banks performed better than average. This is quite an extraordinary accomplishment, and a testament to credit unions’ and local banks’ commitment to delivering an excellent and digital customer experience.