One of the main reasons why consumers choose to bank at credit unions is the promise of more personal financial services. For so long, “personal” has been practically synonymous with “face-to-face.” Yet as the world adjusts to a new, more remote reality due to the coronavirus, customers are understandably reluctant to visit physical branches. Our research also indicates that customers are in no rush to go back to branches—now seen primarily as cumbersome and inconvenient relics––even after the coronavirus threat passes.

In light of these changes in customer needs, how can credit unions structure critical remote banking offerings without sacrificing the human touch that differentiates them from traditional banks?

And how can credit unions ensure that their call centers and online agents are equipped to provide remote and delightful experiences — at scale and cost-effectively?

These are the questions we will explore and attempt to address below.

The Imperative For Credit Unions to Serve Customers Remotely

Despite official lockdowns being lifted around the country, consumers are reluctant to return to physical banking.

A recent survey of 1,028 Americans found that consumers spanning all demographics continue to prefer digital and remote banking options––and many will simply skip banking activities that require in-person interaction. For example, as many as 49% of consumers indicate they would avoid taking a loan out if it required a physical visit to a credit union.

This hesitance about going back to “normal” isn’t just about fears of virus transmission. During the lockdown, digital banking went from being a nice alternative to a must. As a result, even groups such as senior citizens who normally would shy away from digital banking had the opportunity to get comfortable with it.

The mandatory lockdowns have shown consumers just how many errands and tasks can be done remotely, on their own time and at their own convenience. Note the following findings:

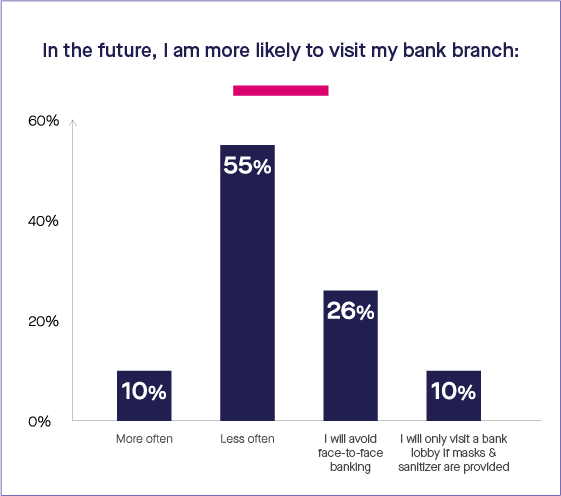

55% of consumers say they plan to visit credit union branches less often in the future.

26% say they will avoid face-to-face banking altogether.

Just 10% say they would only visit a branch if masks and hand sanitizers are available there.

For credit union customers, the promise of remote, instant banking is highly attractive. This creates both a challenge and a significant unique opportunity for credit unions to save on costs and maximize their competitive advantage.

Not Just a Member Experience Issue: How Credit Unions Stand to Save Through Digitization

Credit unions work differently than traditional banks, typically maintaining more pared-down operations. Therefore credit union executives who are committed to an effective digital transformation will need to allocate funds to operations that have a tangible and direct ROI. Moving to serving customers effectively online or through call centers, rather than investing in costly location-specific services, will ensure the scalability credit unions need in our newly remote world.

Scalable digital services pack a significant punch when it comes to cost-effectiveness. McKinsey found that banking institutions can reduce their costs by 20 to 25% by switching to digital customer-facing processes and services.

Additional research shows that the average customer transaction at a physical branch costs banks $4, while banking on a website costs just $0.09 per transaction. Mobile banking is the most cost-effective channel at just $0.019 per transaction. Digitizing means maximizing modest resources.

The Challenge: Smaller Budgets, More Reliance on Human Touch at Credit Unions

As non-profit institutions, credit unions do not always have access to the same expansive budgets and offerings of traditional banks. Indeed, the feeling of community and service, rather than ultra-streamlined contact centers, has driven credit union membership. Online and call center agents may feel newly burdened by an influx of remote customer requests, many of which they were accustomed to dealing with in-person.

The Opportunity: A Limited Branch Network Is No Longer a Liability

Despite challenges, credit unions potentially have an added advantage in the rapid transition to remote banking. That’s because a previous “shortcoming” of credit unions––fewer branches than traditional banks––is less of an issue now. In fact, it can make switching to digital transactions a way of filling a gap.

Moreover, credit unions’ long-standing dedication to ensuring equal access to good service can be enhanced through greater digital options. For instance, rural customers who live far from branches and shift workers who lack schedule flexibility are particularly well-served by digital services that are available 24/7 regardless of location.

The Potential of Digitization to Augment the Human Touch

Given that customers seek out credit unions for special rates and more personalized service, some may worry that digitization would compromise credit unions’ unique strengths.

To be sure, digitization won’t work if it means leaving as much as possible to self-service, with chatbots and mobile apps replacing human agents. That’s because human agents have a critical role to play in guiding customers through digital processes, such as assisting with digital form filling or document collection via phone call. This helps members complete processes correctly the first time, prevents time-consuming and frustrating bouncing between channels, and preserves the human element.

Digitization also won’t work if credit unions institute partially digitized processes that begin online and eventually redirect customers to a physical branch. This defeats the purpose of having digital channels in the first place and puts the burden back on agents who are thrust into the position of helping customers navigate choppy and incomplete processes.

But if done right, digitization can enhance rather than detract from the human interactions credit unions pride themselves on fostering. Digital platforms that enable members to complete all tasks via intuitive computer or mobile interfaces benefit from the guidance of an on-call agent who can move the activity to completion in a single call.

Member Experience and Digital Performance: No Longer At Odds

Customers expect a higher caliber of digital service in light of the coronavirus, and credit unions stand to gain a great deal from accommodating these digital expectations. By adopting agile and scalable customer-facing technologies that incorporate remote agent involvement, credit unions can ensure that a warm human experience and digital journeys co-exist harmoniously.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

For credit union customers, the promise of remote, instant banking is highly attractive. This creates both a challenge and a significant unique opportunity for credit unions to save on costs and maximize their competitive advantage.

For credit union customers, the promise of remote, instant banking is highly attractive. This creates both a challenge and a significant unique opportunity for credit unions to save on costs and maximize their competitive advantage.