eSignatures play a mission-critical role in the lifecycle of an auto lender. It’s the essential consent that allows loan applications, modifications, and collections actions to take place in an efficient manner. Here, we’ll take a look at how the auto finance industry can harness eSignatures to enable instant customer consent from any location.

eSignatures Are Indispensable for Auto Lenders

Given how much time auto lenders spend collecting customer documents and forms, as well as underwriting and presenting approvals, every minute counts. And the best way of ensuring speedy turnaround times for customer-facing lending tasks is by going digital at every opportunity.

Customers agree. One Lightico study found that 58% of borrowers believe an auto loan should be able to be completed entirely online. This is a strong indication of how much convenience, and therefore speed, is a priority for auto loan applicants. 73% of customers listed ease of loan application process as a decisive factor when looking for an auto loan. Crucially, borrowers say that the company issuing the loan is largely inconsequential if they do not provide the ease that customers expect. Being forced to show up to a physical branch and provide a wet signature on stacks of documents is not acceptable to today’s customers.

Inconvenient analog experiences are also detrimental to auto lenders’ bottom line. According to our survey, excessive time to funding leads customers to drop out of the loan application process. In fact, an astounding 42% of respondents who abandon their loan applications do so because the process “took too long.”

Another 62% put the blame on a poor digital experience, too many touchpoints, and the necessity of going to a physical location — all direct contributors to a lengthy process.

By moving away from wet signatures and adopting eSignatures, both lending officers and customers save valuable time and effort. These are some of the use cases where this time-saving capability can be employed.

eSignature Use Case #1: Loan Originations

When potential borrowers apply for an auto loan, they are often forced to go into their dealer (or straight to the lender) and sign off on their application form. This slows down the process significantly as it requires coordinating schedules ahead of time and cannot be undertaken remotely.

With eSignatures, affirming the veracity of a loan application form or agreeing to a contract can be done from any location, at any time. New customers can consent that the information they’re providing is accurate -- without the burden of adding a wet signature. In the case of co-borrowers, multi-sign can be used to allow different users to consent simultaneously.

eSignatures and other related digital capabilities allow borrowers to breeze through the origination process, from application to final agreement.

eSignature Use Case #2: Loan Modifications

It’s a fact of life that some borrowers will need to change the terms of their loan. Whether it’s for lower interest rates, spreading out the loan across a longer period of time, or increasing monthly payments to shorten the loan term, borrowers sometimes need to make modifications. With eSignatures, it’s easy for them to consent to new contracts from the comfort of their mobile phones. No need to go into a physical location or even email signed documents. So loan modification contracts can go into effect immediately.

eSignature Use Case #3: ACH

Getting borrowers to complete ACH authorization so that they can make automatic recurring payments is a goal for most auto loan providers. Using ACH for loan repayments drops the delinquency rate by as much as 80%. Smart eForms for ACH authorization, along with a mobile-optimized eSignature line, can significantly improve the likelihood of borrowers signing up for ACH.

eSignature Use Case #4: Delinquency and Collections

If a customer does, however, fail to pay back their loan on time, the collections process begins. Digitizing collections is also worthwhile, as it reduces the time it takes for collections officers to chase customers to agree to new terms. With eSignatures, collections officers can get delinquent borrowers to consent to new terms while on the phone with them. Instant, mobile eSignatures prevent delinquent borrowers from slipping away.

Automated Digital Workflows and eSignatures

eSignatures are generally the last, or one of the last, elements of an automated workflow. But they are so important to get right. Once the end-customer has got their ID verified, applied for the loan or loan modification, and sent their stips, they need to provide that final, all-important consent. Make it too cumbersome for them to sign, and a lender risks losing a borrower that was so close to the finish line.

Adding eSignature software to an automated digital workflow should be relatively easy, provided the workflow is dynamic and configurable.

But depending on the eSignature provider, industry, company size, how many agents will be using the platform, and existing workflow, the implementation may take more or less time.

To ensure implementation goes smoothly, it’s critical that the company works very closely with the vendor, who should provide hands-on or remote training to optimize usage.

Stakeholders should make sure the users of the eSignature, as well as relevant executive management, see the value in the solution. Be sure to speak to employees about the goals the company hopes to meet through adopting the eSignature, and emphasize ease of use and productivity benefits. Employees who understand the “why” will be more receptive to training, and more eager to use the solution in their job.

The Auto Lending eSignature Process

Once agents and executives are aligned on using the eSignature software, and once agents have been trained, the next part is to set them up in the greater digital workflow.

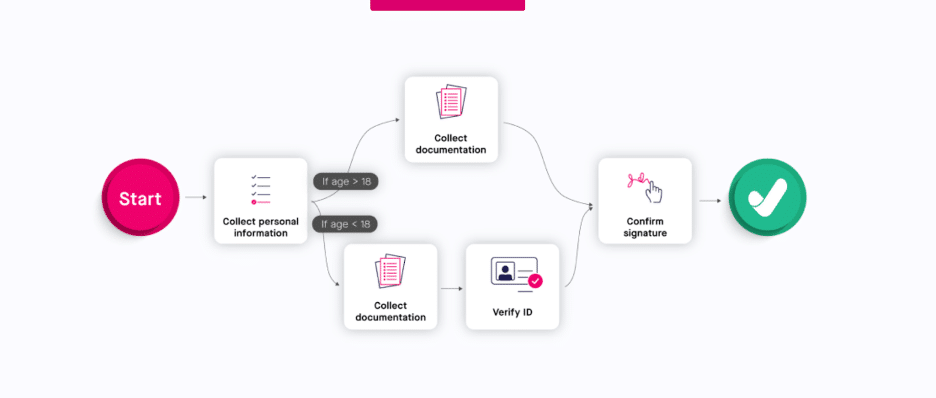

It’s easier than it sounds. An admin simply enters into a console with a drag-and-drop interface, configuring business rules to trigger requests for eSignatures. For example, customers may be required to add their eSignature to some digital documents, but not others. Admins can set up relevant rules based on conditional logic (“if”/”then”).

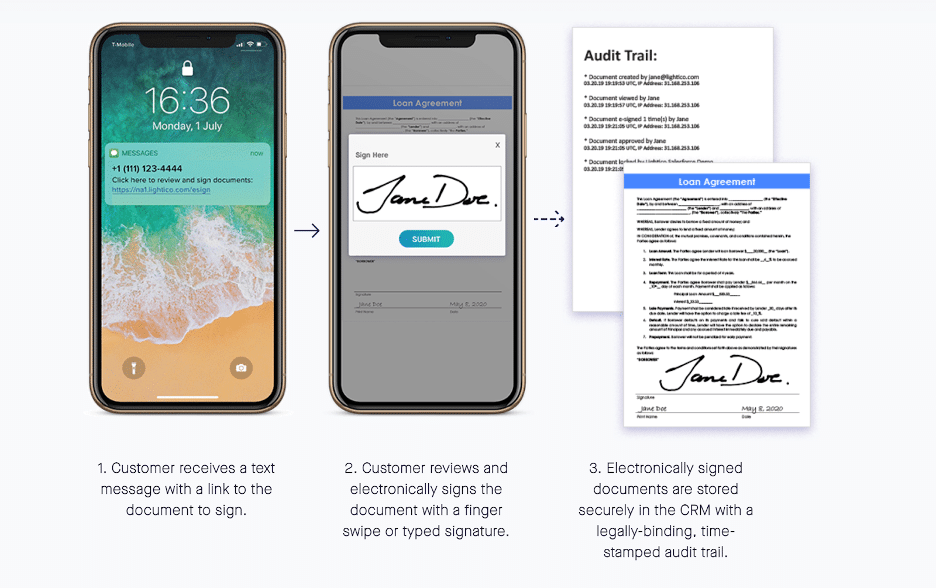

Here is what the eSignature flow looks like once configured:

Not only is it very easy for customers to sign from any digital channel, from any location, it’s easy for agents to receive them in the moment, when they are instantly stored for future reference. There is zero lag time between any of these steps, allowing eSignatures to be a seamless part of the customer-facing workflow.

The Bottom Line

Whether a borrower is applying for a loan, modifying an existing one, authorizing ACH, or dealing with delinquent payments, eSignatures help create forward momentum. eSignatures are most effective when they’re part of a larger automated workflow including ID verification, eForms, digital document collection, and digital payments. To learn more about Lightico’s full digital offering for auto lenders, visit Lightico.com.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

eSignatures are generally the last, or one of the last, elements of an automated workflow. But they are so important to get right. Once the end-customer has got their ID verified, applied for the loan or loan modification, and sent their stips, they need to provide that final, all-important consent. Make it too cumbersome for them to sign, and a lender risks losing a borrower that was so close to the finish line.

Adding eSignature software to an automated digital workflow should be relatively easy, provided the workflow is dynamic and configurable.

But depending on the eSignature provider, industry, company size, how many agents will be using the platform, and existing workflow, the implementation may take more or less time.

To ensure implementation goes smoothly, it’s critical that the company works very closely with the vendor, who should provide hands-on or remote training to optimize usage.

Stakeholders should make sure the users of the eSignature, as well as relevant executive management, see the value in the solution. Be sure to speak to employees about the goals the company hopes to meet through adopting the eSignature, and emphasize ease of use and productivity benefits. Employees who understand the “why” will be more receptive to training, and more eager to use the solution in their job.

eSignatures are generally the last, or one of the last, elements of an automated workflow. But they are so important to get right. Once the end-customer has got their ID verified, applied for the loan or loan modification, and sent their stips, they need to provide that final, all-important consent. Make it too cumbersome for them to sign, and a lender risks losing a borrower that was so close to the finish line.

Adding eSignature software to an automated digital workflow should be relatively easy, provided the workflow is dynamic and configurable.

But depending on the eSignature provider, industry, company size, how many agents will be using the platform, and existing workflow, the implementation may take more or less time.

To ensure implementation goes smoothly, it’s critical that the company works very closely with the vendor, who should provide hands-on or remote training to optimize usage.

Stakeholders should make sure the users of the eSignature, as well as relevant executive management, see the value in the solution. Be sure to speak to employees about the goals the company hopes to meet through adopting the eSignature, and emphasize ease of use and productivity benefits. Employees who understand the “why” will be more receptive to training, and more eager to use the solution in their job.

Not only is it very easy for customers to sign from any digital channel, from any location, it’s easy for agents to receive them in the moment, when they are instantly stored for future reference. There is zero lag time between any of these steps, allowing eSignatures to be a seamless part of the customer-facing workflow.

Not only is it very easy for customers to sign from any digital channel, from any location, it’s easy for agents to receive them in the moment, when they are instantly stored for future reference. There is zero lag time between any of these steps, allowing eSignatures to be a seamless part of the customer-facing workflow.