How Can Banks Speed Loan Deferments & Extensions While Minimizing Customer Stress?

By Gaby Young

By the time most banking customers request a deferment or extension of their loan, they’ve already been handling the stress of dealing with financial challenges for some time.

Handling these requests efficiently is critical for banks to avoid process gaps and misunderstandings with customers that can waste time and frustration for both sides, drag them into collections processes, and escalate into disputes.

Why Do Good Banking Customers Turn to Banks to Defer or Extend Their Loans?

With many Americans still regrouping from the economic effects of COVID, The Consumer Financial Protection Bureau (CFPB) recently issued a new rule to help make loan modifications easier for homeowners.

In the vast majority of cases however, when a customer picks up the phone and asks about a bank loan extension, loan deferment, or how they may modify loan terms, they’re proactively taking steps to manage temporary financial hardship and avoid falling into delinquency.

Whether it’s loss of income due to unemployment, a sudden illness or health concern, the death of a spouse or secondary wage earner, a struggling business venture, or an environmental disaster, customers are looking to stop the bleeding early with their bank’s help and they want to do so without significantly harming their credit rating.

For banks and financial institutions, loan deferments and extensions are critical to:

Avoiding loans, mortgages, credit cards and many other banking products from falling into delinquency or even default

Preventing money and time resources expended on collection processes, disputes, and even legal escalation or regulatory complaints

Retaining the long-term loyalty and lifetime value they can reap from good customers by helping them stay in good standing during their time of need.

Banks can help customers by allowing them to skip a certain number of payments and attach them to the end of the term instead, extending the term to lower monthly payment amounts, or refinance loans at a lower interest rate.

But timing is especially of the essence for these loan modifications: In many cases a customer officially becomes delinquent after falling behind just 30 days on a credit card payment.

That can already trigger collection processes, calls and letters that inflame customers who are actually trying to take responsibility and work with their bank. Not only can this sour relationships and risk churn, it can lead irate customers to escalate the matter by reporting disputes and complaints, tying up the time and resources of multiple departments - all scenarios that would have been needless and preventable if the loan modification process was completed efficiently.

Avoiding this unwanted friction means the process for loan deferment or extension requests must be as swift and seamless as possible.

Digital Silos & Legacy Processes Add Hassle & Irritation to Loan Deferments & Extensions

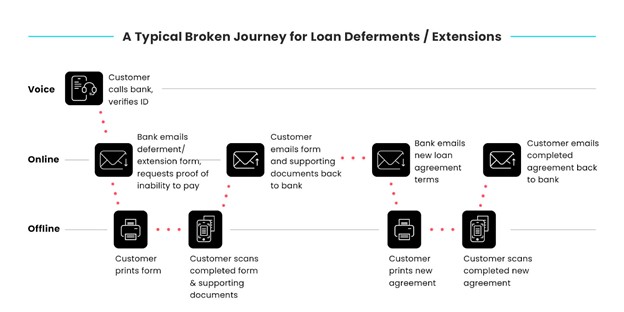

Banks’ current processes for handling these requests is made up of a patchwork of digital point solutions that are not integrated with one another and demand multiple steps in order to verify ID, obtain signed and completed forms and customer consent on new terms and conditions, and receive supporting documents needed to approve deferring loan payments. These digital silos make it impossible to accelerate the process for both banks and their customers.

Further complicating and delaying this journey are legacy processes, like PDF-based forms, and outdated tech like printers, fax machines, scanners, and snail mail that repeatedly force customers offline just to complete their requests.

To review and process complete loan deferments or extensions banks need to:

Confirm the customer’s identity

Review the customer’s outstanding balance

Collect proof of the borrower’s inability to pay - i.e. income and expenses - and capture the reasons they’re asking for deferment/extension

Draw up a new loan (extension/deferment) agreement that details how many payments can be deferred, the new payment schedule, any changes to the loan terms, and any penalty fees

Send a new loan agreement and terms for the customer to sign and accept

Receive signed consent to the new loan terms

The steps and paperwork that come with them mean that engaging with multiple touchpoints is inevitable for banking customers.

They need to spend time connecting with a contact center agent so they can verify ID and update them on why they need help with their loan. Filling out and signing a loan deferment form means they’ll need to hop to their inbox and download one or more documents to complete. If the customer is on their mobile, digitally signing a lengthy form is particularly uncomfortable, and many will wait until they can get to their laptop or PC. Many customers will go the old school route and print them out - but this means having to find a scanner or fax machine so they can email back a completed soft copy to the bank.

Going from phone calls, to downloading PDF forms, and using printers, fax machines or scanners is not fast or convenient for banking today’s banking digital-first customers. Neither is pushing, tracking, and chasing paperwork for bank employees.

And if bouncing from these channels isn’t already frustrating enough, many banking security policies may view email as not a secure enough channel to send sensitive financial data back and forth. Instead they’ll play it safe and send paper loan deferment agreements by snail mail - making the customer wait much longer just to receive them.

Instead of providing solutions, siloed systems and legacy processes delay their completion and pain for banks and customers all along the way.

The Pain for Customers

Exacerbate customers already stressed by financial challenges, complicating and prolonging the process of requesting deferments or extensions on their loan payments.

Forces them to use several manual outdated processes rather than the digital channels most convenient for them

Create gaps in communication in between each step that delay the process and can and result in the customer falling into delinquency - further inflaming customer frustration

The Pain for Banks

Employees can spend days or even weeks chasing customers to complete pdf and paper forms

Delinquency can overlap the customer account with collections processes and deteriorate, needlessly sparking disputes and complaints while exhausting staff time and resources

Human errors in collecting signatures, consent on terms and conditions, and processing forms can risk non-compliance

Cutting the Stress & Complexity Out of Loan Deferments with Digital Completion

To avoid these painful and costly broken journeys banks can make use of emerging Digital Completion technology that connects all customer-facing steps involved in loan deferments and extensions in the one place today’s customers turn to get things done: Their mobile phones.

Instead of sending customers on assignments to download forms and agreements, banks can instead send a simple SMS link that opens an interactive digital session optimized for mobile that walks them through every step in real time, including eSignatures, ID verification, document collection, and digital consent of new loan terms and conditions from one integrated platform.

Project managers can use intelligent and automated workflows to define all required aspects of modifying existing loans and customize the journey for each scenario - making sure customers only see and complete the terms and conditions needed to approve new loan agreements.

Collecting all forms and new loan terms digitally also helps avoid repeat calls to contact center agents to answer follow-up questions about details of new loan agreements. Live in-session agent assistance can review these questions on the spot and help customers complete the entire request.

Banks and financial institutions currently accelerating their loan deferment and extensions processes are:

Resolving loan modification requests 67% faster

Reducing touchpoints by 60%

Ensuring 100% Compliance

Streamlining loan deferment and extension processes enable banks to support good banking customers when they need it most and do this painlessly without the hassle of bouncing across online and physical channels or the delays that can be especially frustrating when their stress is already elevated.

Making difficult times easier helps strengthen loyalty and lifetime value with these customers in the future. It also eliminates hours if not weeks of employee time and resources spent on admin and paperwork, prevents activating unwarranted collection processes, and reduces human errors so they can minimize compliance risks.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Going from phone calls, to downloading PDF forms, and using printers, fax machines or scanners is not fast or convenient for banking today’s banking digital-first customers. Neither is pushing, tracking, and chasing paperwork for bank employees.

And if bouncing from these channels isn’t already frustrating enough, many banking security policies may view email as not a secure enough channel to send sensitive financial data back and forth. Instead they’ll play it safe and send paper loan deferment agreements by snail mail - making the customer wait much longer just to receive them.

Instead of providing solutions, siloed systems and legacy processes delay their completion and pain for banks and customers all along the way.

The Pain for Customers

Going from phone calls, to downloading PDF forms, and using printers, fax machines or scanners is not fast or convenient for banking today’s banking digital-first customers. Neither is pushing, tracking, and chasing paperwork for bank employees.

And if bouncing from these channels isn’t already frustrating enough, many banking security policies may view email as not a secure enough channel to send sensitive financial data back and forth. Instead they’ll play it safe and send paper loan deferment agreements by snail mail - making the customer wait much longer just to receive them.

Instead of providing solutions, siloed systems and legacy processes delay their completion and pain for banks and customers all along the way.

The Pain for Customers

Banks and financial institutions currently accelerating their loan deferment and extensions processes are:

Banks and financial institutions currently accelerating their loan deferment and extensions processes are: