So much of what goes into earning the loyalty of your banking customers comes down to one word: Trust. And no scenario tests trust between bank and customer than when a dispute arises.

That’s why what at first thought appears as an edge-case scenario that banks should simply minimize is actually ever-critical to retaining customers for banking and financial institutions. Resolving a banking dispute quickly and painlessly will give your customers peace of mind and increase the likelihood they will stay with your brand for the long haul. Put them through a long and inconvenient process, and chances are high they will seek a banking alternative — and walk.

In the digital era, banks have invested in automated workflows to help make that journey seamless and convenient. But today's banking dispute processes have it backwards: Instead of taking the opportunity to show their customers why they’re in good hands, many dispute processes today make their customers jump through hoops and work hard just to solve the issue.

If banks are working so hard to improve digital processes and delight customers, why are these customers experiencing anything but during the banking dispute resolution process?

The Main Culprits? Digital Silos Systems and Legacy Processes

Banks invest in several point solutions to digitize customer-facing processes, including ID verification, digital signatures and eforms, and solutions that help customers upload supporting documents.

But piecing together these steps of the process using siloed solutions forces their customers on a broken journey that bounces them around from one channel to another.

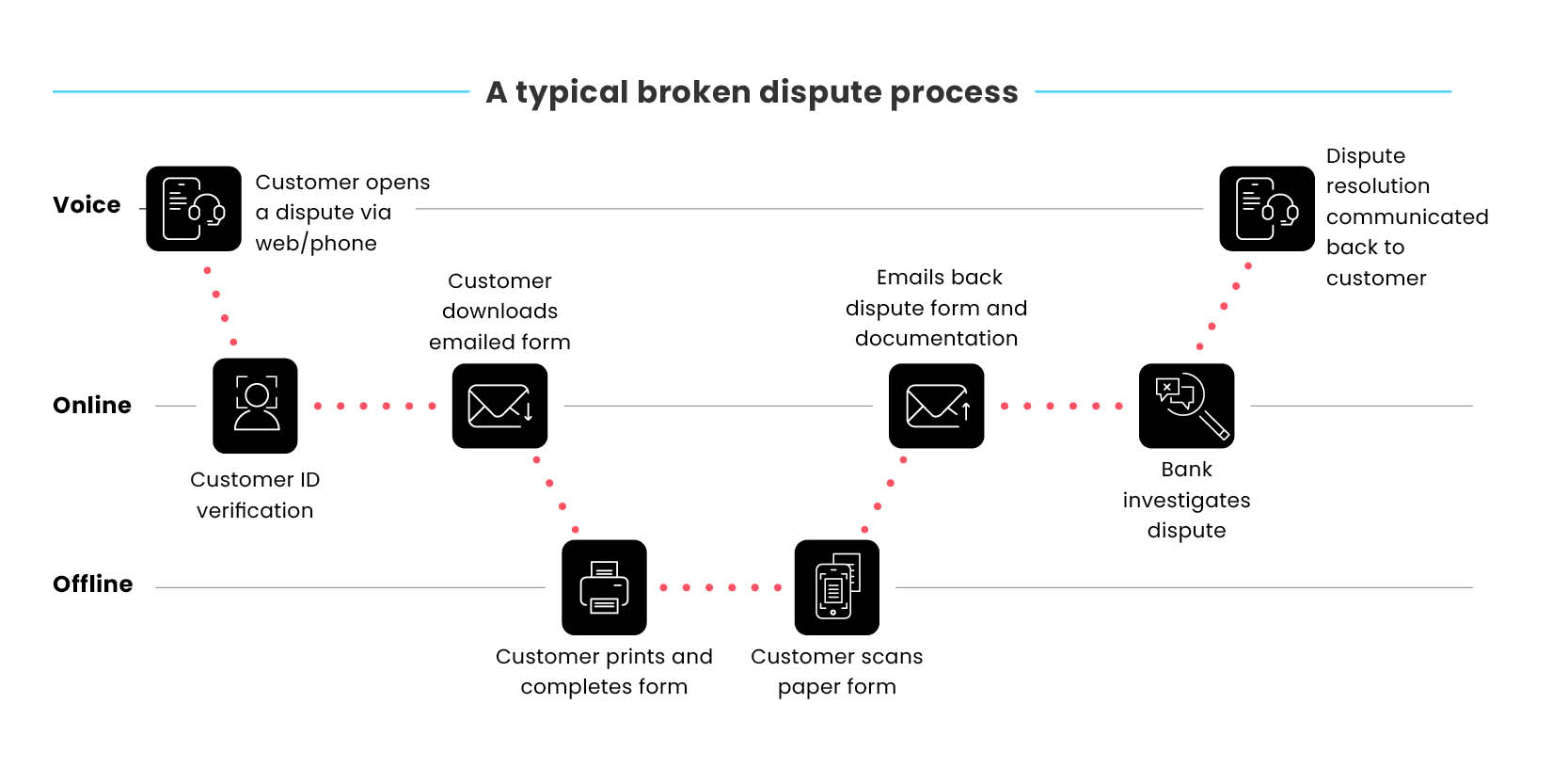

For example, take a customer who realizes they’ve been wrongly charged for a purchase. They’ll first connect with the bank either on the phone or via their website if they find the right page and form to fill out to report their dispute. Typically, this customer may speak to an agent at first to explain why they were overcharged and by what store.

The agent will then email the customer a form to capture all of the relevant details regarding the dispute. On-the-go and constantly multitasking, today’s customer would prefer to fill out and sign a banking dispute form directly from their mobile phone. But with most banks reliant on legacy-based forms instead, they’re usually asked to download a PDF-based form that’s clunky and difficult to follow. As a result the customer will usually need to print out the form before filling it out and signing it. Then, to get it back to the bank, they’ll usually need to scan the completed form and send it back to the contact center.

Before their dispute even gets reviewed, this customer has had to spend time speaking to an agent on the phone, opening and downloading a PDF form, printing it, and often have to trek out to a store to scan it. That’s a make-work process if there ever was one. And it’s because digital silos and legacy processes force customers into a lengthy and broken banking dispute process.

The Undisputed Truth: Broken Journeys Leak Customers

Precisely at the time where their loyalty is already at risk, digitally incomplete journeys prolong dispute resolution. Due to frustrating experiences just like this, banks risk false starts and service-level issues such as escalation, customer churn, and lowered NPS, and regulatory compliance.

Streamlining the Entire Banking Dispute Process with Digital Completion

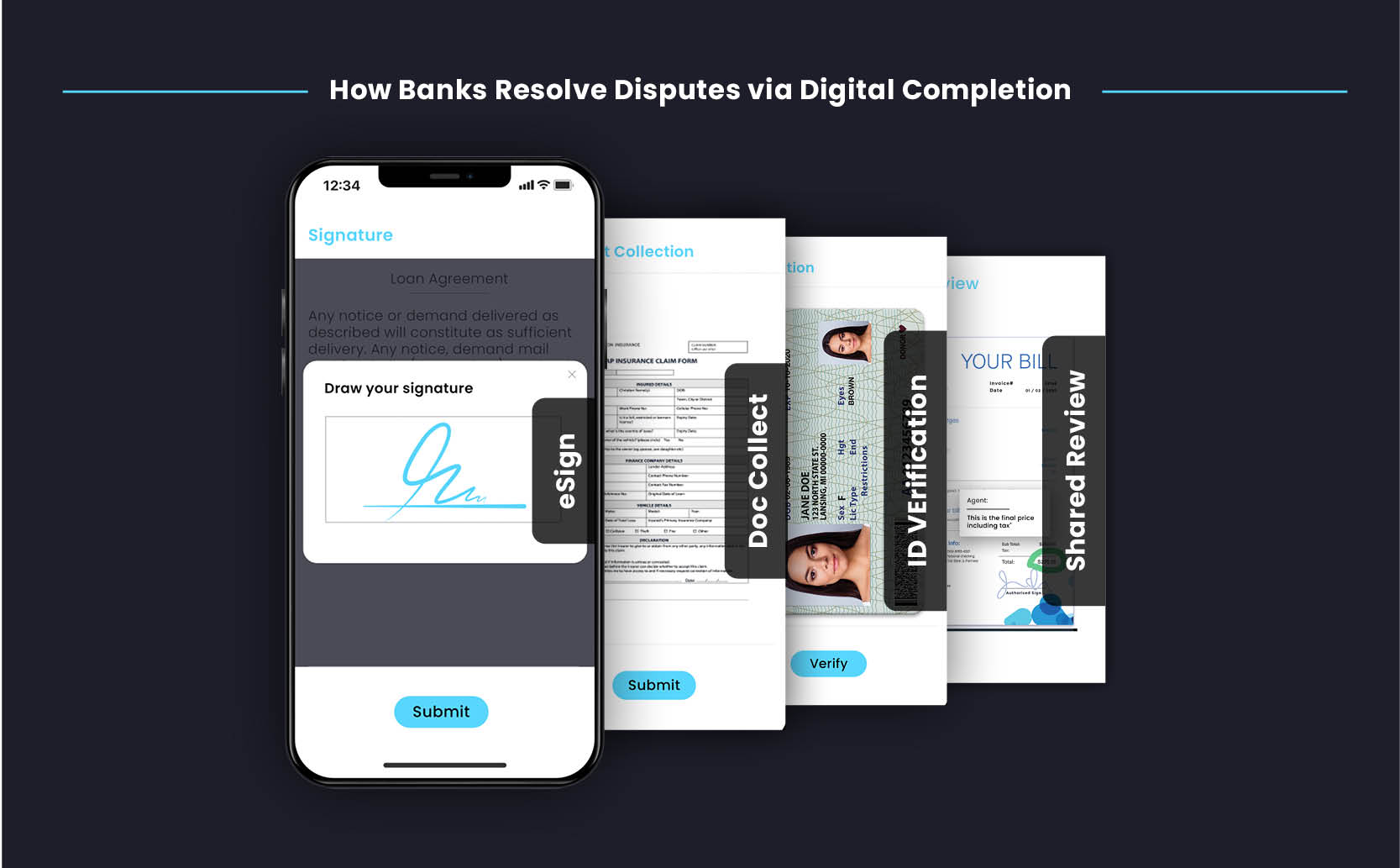

From e-signatures, ID verification, document collection, and terms and conditions, technological innovations now enable banks to give customers one seamless digital experience that quickly and transparently guides them through the entire banking dispute resolution process, right on to completion.

This is possible through an end-to-end Digital Completion solution. This one interactive digital experience lets banks share documents with their customers and guide them in real time, every step of the way, until the dispute is resolved.

Being able to complete all of these steps digitally not only saves time and effort for the customer, integrating this with agent assistance gives customers the comfort and peace of mind needed to know their dispute is being handled with care, boosting their trust and loyalty in your brand.For banks, digital completion allows them to cut significant time and resources spent on fielding customer complaints and guiding them through the dispute process. An average dispute call fielded at the branch or contact center can take between 5-10 minutes to complete. Having an entirely automated self-service workflow helps to complete these tasks faster while minimizing time expended on agent calls and administrative tasks that follow this and many other banking processes.

Financial institutions currently delivering that experience to their customers are seeing immediate improvements to major KPIs, including:

First-call Resolution(FCR)

Turn-around times (TAT)

Overall time to resolution

NPS / CSAT

Resolving disputes is already an anxious experience for banking customers, and a true customer experience test that can make or break their relationship with your bank. Simplifying that process with Digital Completion can help banks pass this test with flying colors en route to strengthening customer loyalty.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Financial institutions currently delivering that experience to their customers are seeing immediate improvements to major KPIs, including:

Financial institutions currently delivering that experience to their customers are seeing immediate improvements to major KPIs, including: