Why Does Digital Completion Matter For the Customer Experience In Banking?

By Leor Melamedov

Banking products and services tend to be extremely similar from bank to bank. Applying for a loan, getting a credit card, and taking out a mortgage — these things don’t vary much. That’s why in recent years, institutions have prioritized the customer experience in banking.

A positive customer experience can be characterized by many things, but one of the main ones is the ability to digitally complete customer-facing transactions faster. Ultimately, bank customers simply want to finish their banking task as quickly, efficiently, and painlessly as possible.

This is where the concept of digital completion comes in. Digital completion refers to streamlining and automating customer-facing tasks, and minimizing human manual involvement. Here, we’ll discuss more of what digital completion refers to, and how digital completion can help improve banks’ NPS and loyalty.

What is Digital Completion in Banking?

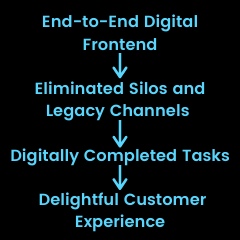

Digital Completion refers to the intelligent automation and delivery of customer-relevant tasks into simplified, accelerated completed customer journeys. The goal is to deliver step-changed business efficiency, error-free compliance, and customer delight.

Until now, too many CIOs and CTOs have been nearly unitarily focused on ensuring operational continuity and stability, and customer-facing interactions have been afterthoughts. As a result, we have seen incredible progress in internal digitization but have neglected front-facing systems. For customer-facing processes, banks have typically cobbled together a combination of digital point solutions, mixed with legacy interactions. But these are disjointed and far from complete.

To leverage the investments already made, banks need to add a business-centric digital front. This is everything that is visible to customers and directly impacts the quality and speed of their experience. The approach should be focused on streamlining the entire road to completion, not on piecemeal solutions that end up in silos. Ultimately, half-measures only add greater confusion and choppiness to the customer journey.

Banks that have achieved digital completion are:

Truly real-time: The bank shares and collects all tasks requiring completion in real-time with customers.

All in one place: The bank can consolidate all customer-facing tasks into a single interactive experience.

No-code automation: Any business user is able to design workflows that automate the full journey and tailor it to each customer.

Fully integrated: Banks are able to get more out of their existing systems via APIs.

What’s Standing in the Way of Digitally Complete Banking Journeys?

On the one hand, customers like to be able to complete banking tasks independently. On the other hand, they still prefer to receive agent-assisted guidance — as long as it doesn’t involve mandatory branch visits or waiting for extended periods on the phone. An approach of digital completion means blending complementary elements — employee guidance and automation — for the purpose of removing obstacles that stand in the way of completing bank tasks.

An approach that emphasizes the digital completion of processes aims to tackle two culprits that have long thwarted customers from getting stuff done: The prevalence of silos and legacy channels. Banks that have the right tools in place can eliminate silos and legacy channels, which in turn makes completion possible. And more tasks completed faster means a better customer experience.

Silos

Banks today usually employ technology to enable digital interaction. Yet many of these technological tools end up creating more silos because they fail to connect the dots of the customer journey. For example, a bank may allow customers to begin the account opening process online, but redirect them to a physical branch when it comes time to sign.

In such cases, digital processes are not integrated and lack cohesiveness. Customers are bounced from one channel to another, leading to frustration. It’s also common to see things like customers being able to fill out some forms electronically, but the forms don’t remember information that was supplied at another stage of the process.

These choppy digital journeys have too many touchpoints and lack a sense of continuity. And this is often due to the fact that companies tend to adopt digital tools as point solutions.

Many customers who encounter siloed processes or too many touchpoints during their journey will simply give up. In other cases, customers do complete the journey but their customer experience has been badly tarnished, putting the bank at risk of reputational damage and churn.

Legacy Channels

Banks may think that eSignatures connected to PDFs and websites are customer-centic and digitally advanced. But in today’s world, mobile is king.

Customers love their smartphones, which allow them to get things done from any location. From ordering goods to trading stocks, consumers today are accustomed to taking care of practically any matter from their miniature handheld computer.

These habits would seem to naturally carry over to how consumers prefer to fill out forms and sign: through their phones. Yet when consumers attempt to fill out banking information and sign via PDF on their mobile phone, they encounter friction. Many existing software solutions on the market require mobile users to open their email, download the pdf, and complete and sign their documents in A4 or Letter size on small screens. The forms aren’t optimized for mobile. And some formats require users to download a particular app in order to digitally fill out the form.

Legacy channels and formats such as email and PDF contribute to excess time to completion, or failure to complete the transaction at all. A study of over 1,000 Americans surveyed respondents who didn’t complete a contract that required an eSignature. The results show that 27% lost or forgot about it, and 35% said it wasn’t mobile- or user-friendly enough. The digital and non-digital channels of decades past aren’t equipped to promote completion for today’s on-the-go, mobile-first customers.

Notably, some of the legacy eSignature solutions have tried to integrate PDF with additional customer-facing capabilities, but this hasn’t yielded the desired results. The experience is still centered around the PDF and therefore difficult to streamline, automate, and make intuitive.

Why Does Digital Completion Matter For Banking CX?

Banks are starting to understand that no amount of exciting marketing, friendly service, or attractive rates can compensate for long and tedious banking processes.

Here is why digital completion can help improve metrics that gauge the customer experience, such as like NPS and CSAT:

1. It’s Mobile-First

Digitally complete banks are mobile-first. Customers are able to complete any task, from applying for a loan to changing their address, from the comfort of their mobile phone. Customers should be able to send stips, forms, and signatures to the bank agent via text message — just as they would interact with a friend. No apps or PDFs are required, relieving the burden of having to download special software.

2. Proving Identity Is Easy

Digitally complete banks make it easy for customers to get their ID verified. Instead of having to show up in person, customers simply take a selfie with their official photo ID. The selfie and the image in the ID are instantly scanned and a match is confirmed. By making KYC instant and digital, the customer is able to complete the task quickly and painlessly.

3. Forms Are Smart

Digitally complete banks allow customers to fill out responsive electronic forms from any channel, including their mobile phone. Fields are revealed or hidden based on conditional logic, saving the customer precious time and minimizing the likelihood of error (and having to redo the form).

4. Signatures Are Instant

Digitally complete banks don’t force customers to repeatedly sign their name, whether electronically or on paper. Customers digitally sign once, tap the signature, and place it on all documents where it’s required. In addition, multiple signatories can affix their signature remotely. This saves customers the headache of having to coordinate a branch visit among multiple account holders.

5. The Human Touch Remains

Digitally complete banks strategically use human input They know how to harness human talent to expedite rather than prolong customer journeys. For example, having employees manually input customer data prolongs time to completion and frustrates everyone. Yet having employees remotely guide customers through a banking task or provide guidance can speed things up — and improve the customer experience.

6. Security Is Frictionless

Digitally complete banks always prioritize security. If they didn’t, customer trust would go out the window. Yet digitally complete banks also understand that issues like security and compliance should coexist with an efficient customer experience. A secure banking frontend can rely on measures such as one-time passwords, single sign-on, and audit trails that don’t unduly burden customers.

CX In Banking Means Digital Completion

In today’s fast-paced, instant gratification world, creating a winning customer experience means allowing customers to complete tasks quickly and easily. By eliminating siloes and replacing legacy channels with end-to-end digital journeys, the customer experience in banking is positively transformed.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Digital Completion refers to the intelligent automation and delivery of customer-relevant tasks into simplified, accelerated completed customer journeys. The goal is to deliver step-changed business efficiency, error-free compliance, and customer delight.

Until now, too many CIOs and CTOs have been nearly unitarily focused on ensuring operational continuity and stability, and customer-facing interactions have been afterthoughts. As a result, we have seen incredible progress in internal digitization but have neglected front-facing systems. For customer-facing processes, banks have typically cobbled together a combination of digital point solutions, mixed with legacy interactions. But these are disjointed and far from complete.

To leverage the investments already made, banks need to add a business-centric digital front. This is everything that is visible to customers and directly impacts the quality and speed of their experience. The approach should be focused on streamlining the entire road to completion, not on piecemeal solutions that end up in silos. Ultimately, half-measures only add greater confusion and choppiness to the customer journey.

Banks that have achieved digital completion are:

Digital Completion refers to the intelligent automation and delivery of customer-relevant tasks into simplified, accelerated completed customer journeys. The goal is to deliver step-changed business efficiency, error-free compliance, and customer delight.

Until now, too many CIOs and CTOs have been nearly unitarily focused on ensuring operational continuity and stability, and customer-facing interactions have been afterthoughts. As a result, we have seen incredible progress in internal digitization but have neglected front-facing systems. For customer-facing processes, banks have typically cobbled together a combination of digital point solutions, mixed with legacy interactions. But these are disjointed and far from complete.

To leverage the investments already made, banks need to add a business-centric digital front. This is everything that is visible to customers and directly impacts the quality and speed of their experience. The approach should be focused on streamlining the entire road to completion, not on piecemeal solutions that end up in silos. Ultimately, half-measures only add greater confusion and choppiness to the customer journey.

Banks that have achieved digital completion are: