eSignatures play a pivotal role across the banking lifecycle. From onboarding new customers, to ongoing servicing, to taking out loans, there are many opportunities for banks to collect customer consent easily and digitally. Here, we’ll look into some of the top ways banks can use eSignatures to improve efficiencies across the customer lifecycle.

Why eSignatures Matter For Banks

Both retail and commercial banks spend a disproportionate amount of time processing paperwork, including chasing after customers to provide consent. This is a major area of concern for banks, as many processes require signatures, including account opening (onboarding), loan applications, and disputes. Even modifications of existing agreements, such as loan deferrals and forbearance requests require documents and forms to be signed and submitted.

But when banks depend on traditional wet signatures, things go awry. Customers are forced to show up to bank branches, and agents are forced to waste time printing and scanning.

Both retail and commercial banks spend a disproportionate amount of time processing paperwork, including chasing after customers to provide consent. This is a major area of concern for banks, as many processes require signatures, including account opening (onboarding), mortgage applications, personal loans such as signature loans, and wealth management. Even modifications of existing agreements, such as loan deferrals and forbearance requests require documents and forms to be signed and submitted.

eSignature Use Case #1: New Account Opening

When customers want to open a new bank account, they are typically required to sift through piles of forms and documents, signing their initials by hand on each page. This is an exhausting process that wastes both agent and customer time, lowering satisfaction rates at a time that should be marked by delight and excitement. With eSignatures, new customers can consent that the information they’re providing is accurate -- without the burden of adding a wet signature.

eSignature Use Case #2: Customer Dispute Resolution

Disagreements between customers and banks require clarification, but the process of getting that clarification is difficult. Customers are often forced to work outside their channel of choice when trying to file a dispute with their bank. As a result of these service-level issues, customers are at risk of escalating their cases, getting entangled in legal disputes, and even churning.

The right eSignature software can speed up this process of resolving customer disputes. The digital dispute form is collected, if necessary. Supporting documentation/proof related to the dispute is also collected. An eSignature field can be added to these forms, which are time-stamped and come with an audit trail.

eSignature Use Case #3: Fraud Investigation

Customer fraud complaints are serious and require investigation, but the process of investigation can be fraught with inconvenience. Fraud journeys may require additional information or supporting documentation and notarization of specific forms –– which tends to involve non-digital or partially digital work. As a result, banks must deal with extra steps, insufficient response rates, and chasing customers for documents.

With eSignatures affixed to fraud complaint forms, banks can expedite the time it takes to resolve fraud complaints. Customer response rates are better due to the ease of mobile eSignatures. And turnaround time shrinks.

eSignature Use Case #4: Reports of Lost/Stolen Credit Cards

While many banks already have a system in place that allows customers to digitally report lost or stolen credit cards, eSignatures can assist in cases where any supporting documentation or follow-up is required.

eSignature Use Case #5: Issue New Credit Cards

Banks sometimes struggle to engage customers outside of staffed hours when credit cards need to be issued or replaced. eSignatures added to online authorization forms allow customers to provide consent and complete their credit card application anytime, anywhere.

eSignature Use Case #6: Manage Account Transfers and Assumptions

The transfer of bank accounts and assumption of accounts/debts/loans (generally in the case of death or divorce of the primary account owner(s) is stressful as these transfers are

typically for loved ones — and carries risk for the bank. Adding eSignatures to authorization forms can ease the bureaucracy surrounding it.

eSignature Use Case #7: Loan Applications

Customers are still often required to sign off on documents at a physical bank branch when they want to apply for a loan. This prolongs the time to lending, burdening both bank agents and borrowers. With eSignatures, borrowers can simply provide consent to online loan application forms from their cell phones or desktop computers.

How eSignatures Work in an Automated Digital Workflow

eSignatures are generally the last, or one of the last, elements of an automated workflow. But they are so important to get right. Once the end-customer has got their ID verified, shows intent to purchase a product, and has digitally sent their forms and documents, they need to provide that final, all-important consent. Make it too cumbersome for them to sign, and a company risks losing a customer that was so close to the finish line.

Adding eSignature software to an automated digital workflow should be relatively easy, provided the workflow is dynamic and configurable.

But depending on the eSignature provider, industry, company size, how many agents will be using the platform, and existing workflow, the implementation may take more or less time.

To ensure implementation goes smoothly, it’s critical that the company works very closely with the vendor, who should provide hands-on or remote training to optimize usage.

Stakeholders should make sure the users (advisors or agents) of the eSignature, as well as relevant executive management, see the value in the solution. Be sure to speak to employees about the goals the company hopes to meet through adopting the eSignature, and emphasize ease of use and productivity benefits. Employees who understand the “why” will be more receptive to training, and more eager to use the solution in their job.

The Banking eSignature Process

Once agents and executives are aligned on the new eSignature solution, and once agents have been trained to use them, the next part is to set them up in the greater digital workflow.

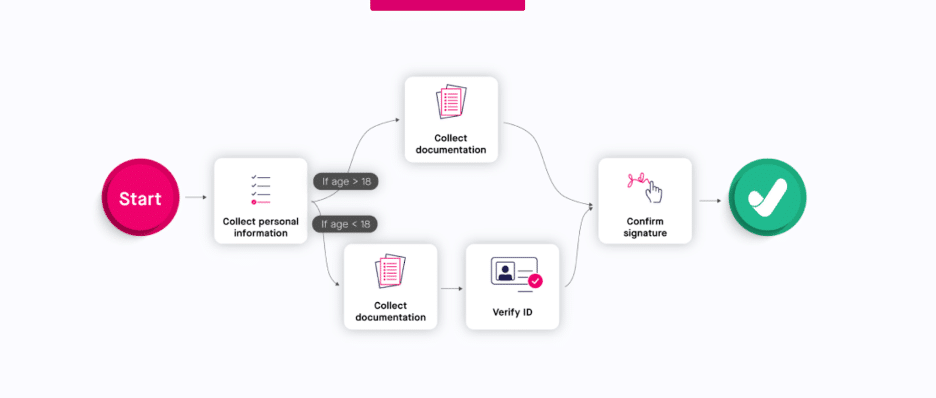

It’s easier than it sounds. An admin simply enters into a console with a drag-and-drop interface, configuring business rules to trigger requests for eSignatures. For example, customers may be required to add their eSignature to some digital documents, but not others. Admins can set up relevant rules based on conditional logic (“if”/”then”).

Here is what the eSignature flow looks like once configured:

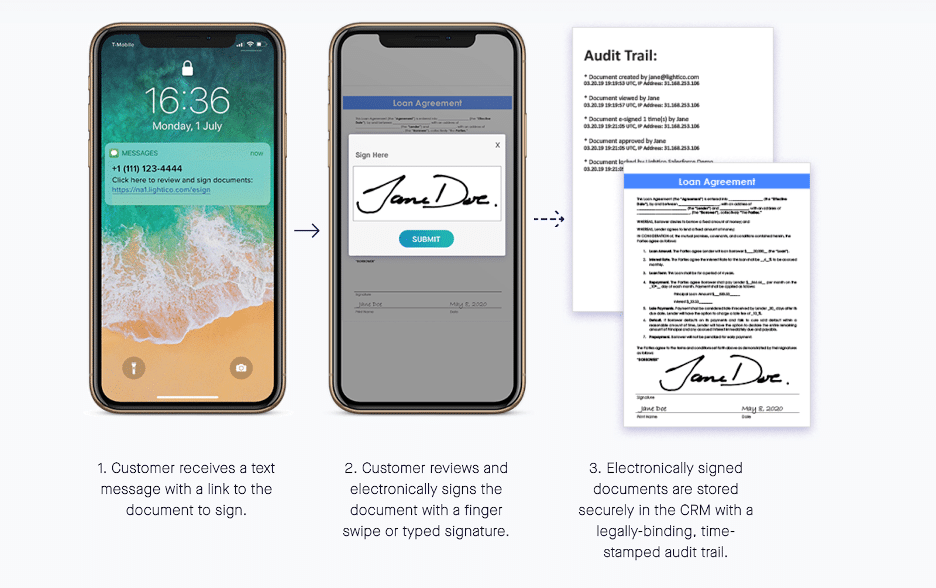

Not only is it very easy for customers to sign from any digital channel, from any location, it’s easy for agents to receive them in the moment, when they are instantly stored for future reference. There is zero lag time between any of these steps, allowing eSignatures to be a seamless part of the customer-facing workflow.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

eSignatures are generally the last, or one of the last, elements of an automated workflow. But they are so important to get right. Once the end-customer has got their ID verified, shows intent to purchase a product, and has digitally sent their forms and documents, they need to provide that final, all-important consent. Make it too cumbersome for them to sign, and a company risks losing a customer that was so close to the finish line.

Adding eSignature software to an automated digital workflow should be relatively easy, provided the workflow is dynamic and configurable.

But depending on the eSignature provider, industry, company size, how many agents will be using the platform, and existing workflow, the implementation may take more or less time.

To ensure implementation goes smoothly, it’s critical that the company works very closely with the vendor, who should provide hands-on or remote training to optimize usage.

Stakeholders should make sure the users (advisors or agents) of the eSignature, as well as relevant executive management, see the value in the solution. Be sure to speak to employees about the goals the company hopes to meet through adopting the eSignature, and emphasize ease of use and productivity benefits. Employees who understand the “why” will be more receptive to training, and more eager to use the solution in their job.

eSignatures are generally the last, or one of the last, elements of an automated workflow. But they are so important to get right. Once the end-customer has got their ID verified, shows intent to purchase a product, and has digitally sent their forms and documents, they need to provide that final, all-important consent. Make it too cumbersome for them to sign, and a company risks losing a customer that was so close to the finish line.

Adding eSignature software to an automated digital workflow should be relatively easy, provided the workflow is dynamic and configurable.

But depending on the eSignature provider, industry, company size, how many agents will be using the platform, and existing workflow, the implementation may take more or less time.

To ensure implementation goes smoothly, it’s critical that the company works very closely with the vendor, who should provide hands-on or remote training to optimize usage.

Stakeholders should make sure the users (advisors or agents) of the eSignature, as well as relevant executive management, see the value in the solution. Be sure to speak to employees about the goals the company hopes to meet through adopting the eSignature, and emphasize ease of use and productivity benefits. Employees who understand the “why” will be more receptive to training, and more eager to use the solution in their job.

Not only is it very easy for customers to sign from any digital channel, from any location, it’s easy for agents to receive them in the moment, when they are instantly stored for future reference. There is zero lag time between any of these steps, allowing eSignatures to be a seamless part of the customer-facing workflow.

Not only is it very easy for customers to sign from any digital channel, from any location, it’s easy for agents to receive them in the moment, when they are instantly stored for future reference. There is zero lag time between any of these steps, allowing eSignatures to be a seamless part of the customer-facing workflow.