The economic downturn and rising interest rates has a deep impact on the consumer lending space. Delinquencies are starting to rise, auto loan defaults are increasing, and concerns about rising costs are ubiquitous. To learn more about the current state of borrowing habits and experiences, Lightico commissioned a survey of 1,449 Americans. We found that a majority of consumers are concerned about their ability to repay loans, but have some doubts about their bank or auto lender’s ability to support them.

Key Findings

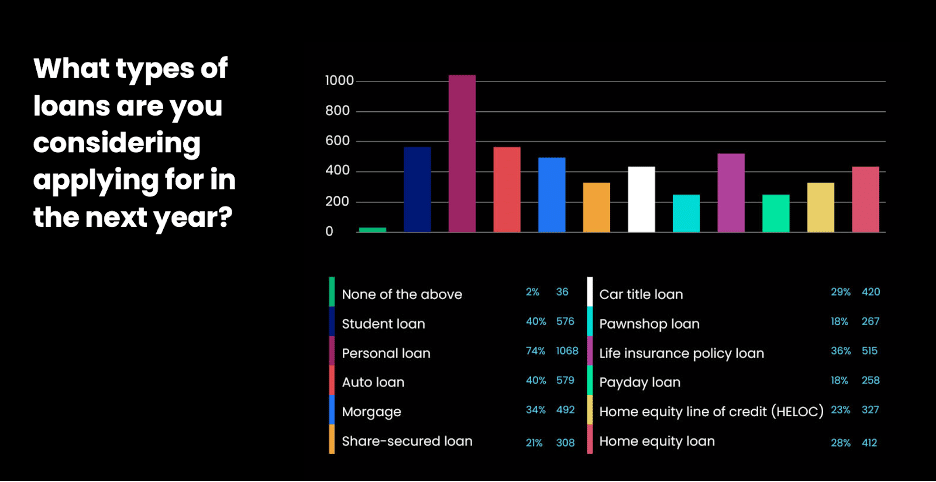

- Loan originations are still happening. Despite higher interest rates, 74% of consumers are considering applying for a personal loan in the next year. Another 40% are considering applying for an auto loan. Lenders will need to ensure these applications are processes quickly and efficiently, with an eye towards the customer experience.

- Loan extensions and modifications are on the rise. High rates and the rising price of goods are leading a majority of consumers to consider a loan extension or modification. Loan servicing will also need to be made more efficient and digital to process the demand.

- More digitization is needed. Overall, borrowers are satisfied with the level of servicing they receive from their financial institution. But there is room for improvement. A sizable minority of consumers say it is difficult for them to modify a loan. Lack of consistent digitization, insufficient self-service options, and multiple touchpoints are likely culprits.

What Consumers Told Us (And What It Means)

Loan Applications Are Unlikely to Slow Down

While many lenders might not be expecting it, they can expect to continue to receive loan applications. Personal loans make up the biggest chunk of the potential applicants, with a whopping 74% of consumers saying they are thinking of taking out a personal loan. Auto lenders can also brace for an influx of car loan applications.

Lenders are advised to take a proactive stance, and prevent many of the common problems plaguing originations. Often during the loan process, the agent chases the customer for additional documentation, with mounting frustration and time loss affecting both sides. Forms are incorrectly filled out, and require rework.

To efficiently process loan applications at scale, lenders are going to have to go all-in on their digital investments. Having a digital loan application, but then bouncing customers to a branch to sign the final agreement, is no longer going to cut it. Such scenarios result in prolonged turnaround times and slower time to funding, which is counterproductive to business goals. It’s also bad for the customer experience.

Instead, lenders will want to invest in technology such as automated digital workflows, which allow customers to submit stips, documents, forms, and terms and conditions consent from a single digital channel.

Loan Modifications Are On The Rise

Financial institutions are currently dealing with increasing borrower defaults and delinquencies due to the economic downturn. Yet many responsible consumers prefer to take a proactive approach and request a loan extension when they’ve fallen on hard times.

Our survey found that 78% of consumers are considering modifying or extending the terms of their loan. This is a significant proportion of consumers. How this process is handled can make or break a lender’s customer experience, reputation, and operational efficiency.

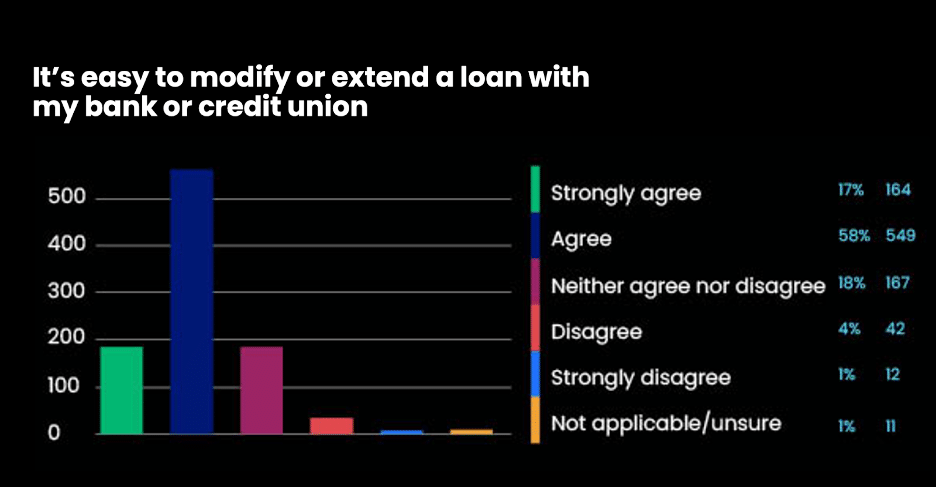

Unfortunately, too many lenders’ processes are cumbersome and inefficient. Our survey found that 25% of consumers don’t agree with the statement, “It's easy to modify or extend a loan with my bank or credit union.” And only 17% strongly agree with the statement, showing a lukewarm attitude towards loan servicing processes.

It’s likely that current loan servicing processes are siloed, leading to frustration and misunderstandings. A customer that is struggling financially and is about to miss a payment may put in a request for a loan extension. Yet if this request isn’t immediately captured, someone from the collections department who is unaware of the loan extension request may take heavyhanded measures. Such missteps due to siloed communication and broken workflows carry a heavy price. They can be uncovered — and penalized — during audits, or result in customer complaints to the Consumer Financial Protection Bureau (CFPB).

Just as with originations, automated digital workflows can alleviate many of the difficulties seen in loan extension processes. They ensure that loan extension requests are captured and processed quickly in a single automated flow from one channel.

With automated digital workflows, borrowers can submit all the forms and documents required (e.g., proof of hardship, payslips) in real time.

Insufficient Digitization

While the coronvirus pandemic and changing customer expectations has led lenders to digitize more processes, they still aren’t fully digital. Customers still find themselves bouncing between touchpoints, channels, and agents during the originations and servicing process. This is particularly problematic for servicing, given the surge we are seeing in this area.

The survey found that 23% of consumers are unable to modify their loan via self-service. This is a lost opportunity for lenders, as many borrowers prefer the relative anonymity of requesting a loan modification on their own. Adding self-service options would also save agent time and potentially reduce call center overhead costs.

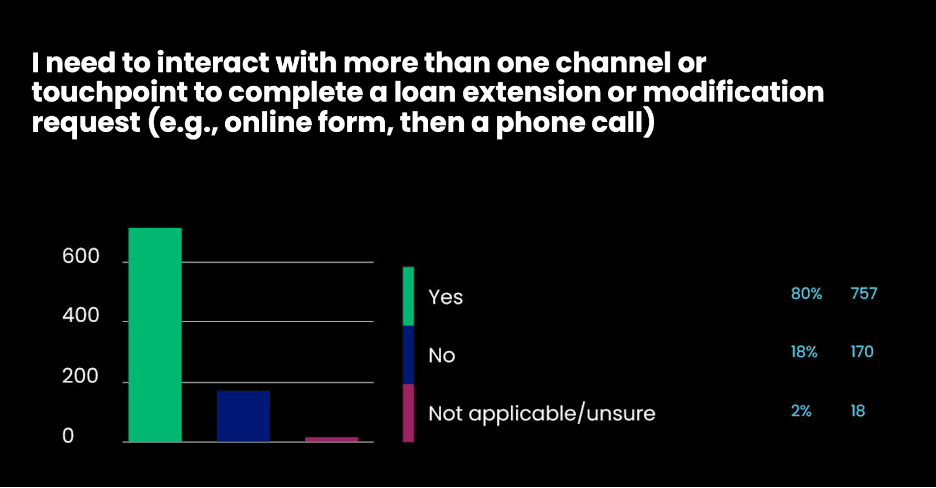

Even more troubling are the high rates of choppy customer journeys. 80% of consumers say that they “need to interact with more than one channel or touchpoint to complete a loan extension or modification request.” Customers may begin their loan modification process online, but they are inevitably bounced to a phone call or mandatory branch visit. Here is another lost opportunity for lenders to go digital, and allow consumers to fill out forms, submit documents, and consent to terms and conditions online.

Digitization reflects the will of consumers. We found that 54% of consumers would prefer to modify or extend their loan through an online channel (i.e., desktop computer, mobile phone, or email). In other words, failing to offer a fully digital loan servicing option alienates more than half of consumers.

Lightico’s Digital Lending Solution

Lightico allows lenders, banks and credit unions to digitize their consumer facing originations and servicing processes. With Lightico’s Digital Completion Platform, lenders can quickly and easily collect signed documents or missing documents straight from the customer's chosen device, in order to complete the loan package or servicing application. All capabilities fit into a single automated workflow. During a live and encrypted digital session (either self-service or with a remote agent), customers can:

- Upload supporting documents in seconds using their cellphone camera

- Submit their details via smart forms based on conditional logic

- Verify their identity

- Submit missing eSignatures, including from co-signers

With this platform, lenders slash time to loan funding or modifying, while improving the customer and dealer experience and keeping fraud out. On average, lenders reduce their “time to collect” by an average of 90%. This allows the business to scale without needing to grow the team size.

Fewer touchpoints are needed, there is no need to chase customers, and customers are happier.

Westlake Financial Services Achieves 94% eSignature Conversion Rate

Westlake Financial implemented Lightico’s mobile-first platform to accelerate and improve service processes. The Lightico Digital Completion platform allows Westlake’s service representatives to instantly collect signatures on extensions and fully complete ACH forms via a simple text message sent to the customer’s mobile phone by the agent during a call.

Using Lightico’s intuitive interface, customers can now complete and sign forms in seconds without waiting for emails or using a printer, scanner or fax - with full compliance.

Since adopting the technology, Westlake’s representatives no longer have to spend their valuable time chasing missing signatures and reworking incorrectly completed forms. As a result, servicing has become much more efficient and Westlake has strengthened its reputation as a leader in the automotive industry.

Read the full Westlake case study here.

The Bottom Line

Today’s consumers are strapped for cash and overwhelmed. By making it easier for them to apply for loans and modify existing loans, financial institutions can cement customer loyalty, reduce inefficiencies, and become leaders in the worldwide digital transformation.