New Survey Shows Seniors Are Eager For Digital Banking––But Worried About Security

By Leor Melamedov

There’s a common stereotype of older people as technophobes––eschewing the conveniences of technology in favor of pen-and-paper or face-to-face interactions. Yet the latest research shows that this is no longer the case. The coronavirus pandemic has only accelerated growing digital and remote trends, forcing unlikely groups, including older people, to interact with technology like never before.

Lightico commissioned a study of 1,329 Americans in July 2020 that found that older customers are just as likely to complete online financial transactions as younger people. Yet compared to their younger cohorts, these consumers voice more concerns about security. This suggests that if banks want older people to have peace of mind, they will need to ensure seamless and effective security measures for online banking transactions.

A Digital Divide Over 65? Don’t Be So Fast to Assume.

The coronavirus has led customers to depend on remote, digital services like never before. 55% of consumers we surveyed say they intend to visit their branch less often, even as restrictions are lifted. Another 26% say they will avoid in-person banking altogether going forward, regardless of safety measures (like mandating mask-wearing and offering hand sanitizer) the bank takes.

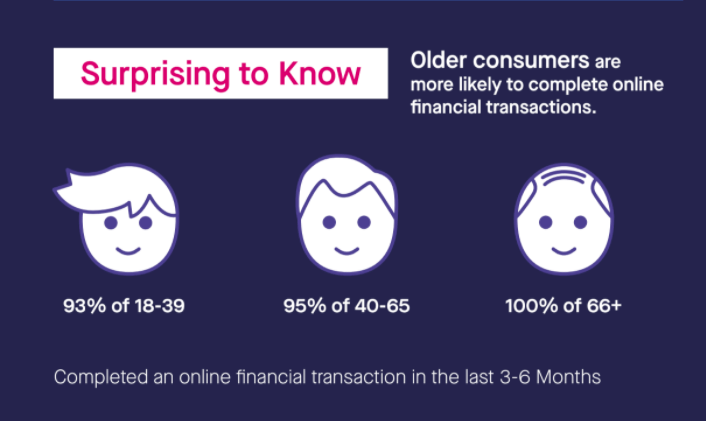

Older people are even warier of in-branch banking due to the increased health risk posed by the coronavirus. The results were dramatic: 100% of the older consumers (aged 66-75) we surveyed say they have completed an online financial interaction in the last three to six months. In contrast, a smaller but still very large proportion (93%) of 18 to 39-year-olds have done so.

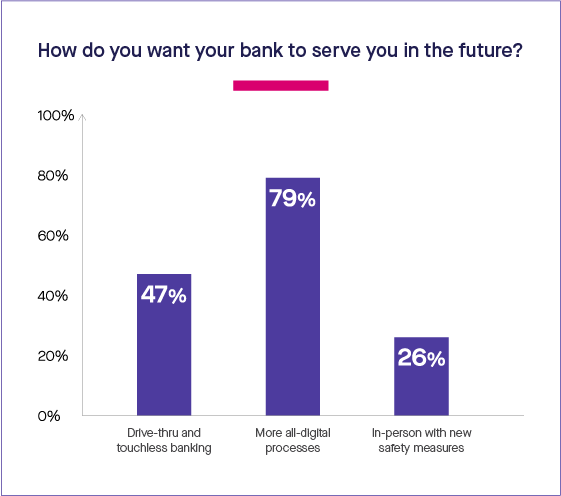

Given that 79% of all consumers want their bank to offer more all-digital processes in the future, it’s very likely that senior citizens have also gained unprecedented comfort with digital banking due to necessity. Whether in a few months or a year or more, the coronavirus will no longer be a reason to turn to digital. But by then, seniors will have become so accustomed to taking care of their finances online that the thought of going to a physical branch will be an unnecessary hassle.

Banking Security Remains a Concern For Seniors

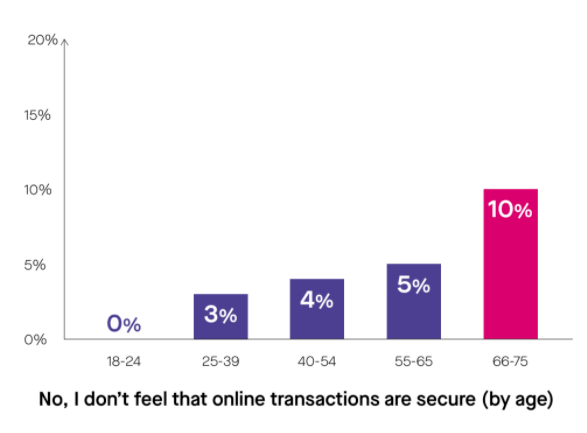

Despite record-high use of digital banking among senior citizens, lingering fears about online security lurk under the surface acceptance of digital tools. 10% of senior citizen bankers don’t feel online transactions are secure (even larger proportions see them as merely “somewhat secure” — also not a raging endorsement).

When asked to rank their top concerns regarding online security, the majority fear financial loss first (52%), and loss of privacy second (42%). Seniors, who are often on fixed incomes and may already feel financially vulnerable, may be especially worried about the potential monetary loss from online identity theft and the like.

To be sure, the majority of people do trust the security of online banking, including older adults. And it would be natural to ask the question, “If seniors continue to be concerned about the security of online banking, then why do they still engage in it?” It may be that seniors are happy to use digital bank tools for the most rudimentary tasks, such as checking their bank balance. But if seniors are avoiding opening a new account, transferring money, or other more “active” tasks due to security concerns, this represents lost opportunities for the bank.

Transparent Security For Peace of Mind

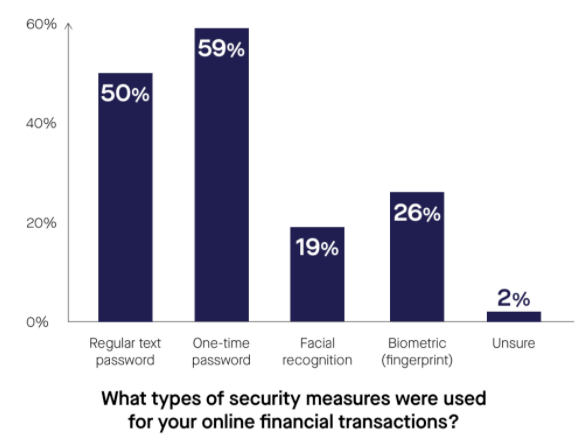

Banks that want to ensure high digital usage from their senior citizen customers would do well to implement visible security measures. Text passwords, one-time passwords, and biometric fingerprints are commonly used by financial institutions and can provide peace of mind. However, their ease of use varies, which we will speak about soon.

Also, senior citizens (like all customers) should be taught to identify phishing attempts and copycat websites. For example, sending an email with clear explanations and examples of hacking attempts will empower senior citizens to avoid falling prey to schemes. These informational emails should also explain using simple language what steps the bank takes to ensure financial and data security.

Even better, security notices should be provided at the moment of the transaction so the reassurance is instant and contextual. No customer should have to begin a digital process without receiving explicit reassurance of how their data is being protected.

Not Just Any Security––Seamless Security

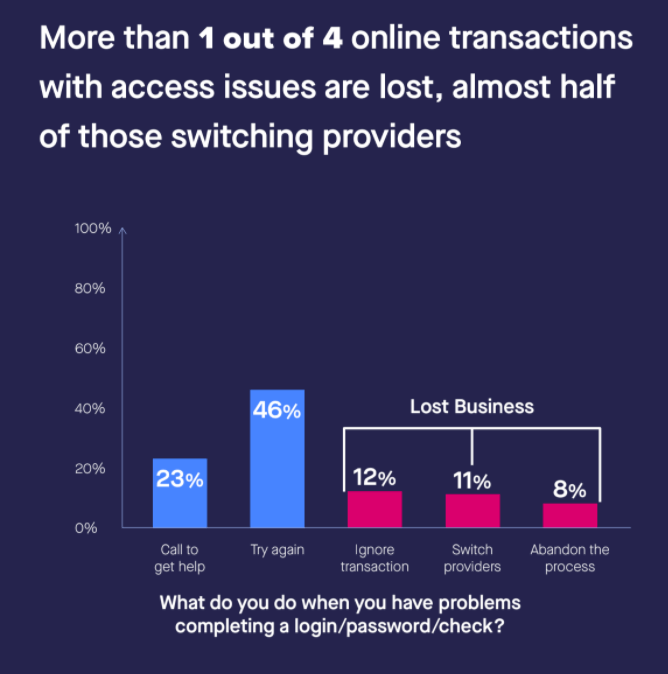

The best kind of secure online financial transaction is one that doesn’t get in customers’ way. Unfortunately, seniors are especially likely to suffer from access issues involving login, password, or security check difficulties, preventing them from even beginning the online banking task.

Seniors who are frequently asked to change their passwords, complete complicated security checks, or otherwise face security-driven obstacles are at risk of giving up on digital interactions. We found that 12% will ignore the transaction, 8% will abandon the process, and 11% will switch providers.

That’s why banks must add security features that don’t interfere with customers’ ease of use. For example, biometric security and facial recognition are all intuitive processes that can be completed from a single channel and don’t require seniors to remember complicated passwords or complete visually challenging security checks. Yet they remain woefully underused compared to more cumbersome password-based security.

Seniors are best served by seamless digital processes that are predictable and intuitive to use. Photo ID verification and digital signatures are based on sophisticated technology that remains nonintrusive to the end-user. They are part of a larger end-to-end process that keeps seniors within a single seamless digital channel, such as a mobile phone or website.

Happy and Secure Seniors

When Texas-based Happy State Bank first implemented Lightico’s secure digital transaction platform, which includes secure digital signatures, ID verification, and time-stamped forms, they were initially concerned about how their many senior citizen customers would take to the new technology.

When we checked in with Mark Murray, Happy State Bank’s VP Business Systems Liaison, he said, “We were relieved and delighted when seniors actually expressed their preference for the simplicity of Lightico’s technology, which doesn’t require any particular technical know-how on the part of the end-user.”

The presence of visible yet intuitive security features that fit into a wider digital process is just what it will take for banks to gain the trust and continued business of senior citizen customers.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

The coronavirus has led customers to depend on remote, digital services like never before. 55% of consumers we surveyed say they intend to visit their branch less often, even as restrictions are lifted. Another 26% say they will avoid in-person banking altogether going forward, regardless of safety measures (like mandating mask-wearing and offering hand sanitizer) the bank takes.

Older people are even warier of in-branch banking due to the increased health risk posed by the coronavirus. The results were dramatic: 100% of the older consumers (aged 66-75) we surveyed say they have completed an online financial interaction in the last three to six months. In contrast, a smaller but still very large proportion (93%) of 18 to 39-year-olds have done so.

The coronavirus has led customers to depend on remote, digital services like never before. 55% of consumers we surveyed say they intend to visit their branch less often, even as restrictions are lifted. Another 26% say they will avoid in-person banking altogether going forward, regardless of safety measures (like mandating mask-wearing and offering hand sanitizer) the bank takes.

Older people are even warier of in-branch banking due to the increased health risk posed by the coronavirus. The results were dramatic: 100% of the older consumers (aged 66-75) we surveyed say they have completed an online financial interaction in the last three to six months. In contrast, a smaller but still very large proportion (93%) of 18 to 39-year-olds have done so.

Given that 79% of all consumers want their bank to offer more all-digital processes in the future, it’s very likely that senior citizens have also gained unprecedented comfort with digital banking due to necessity. Whether in a few months or a year or more, the coronavirus will no longer be a reason to turn to digital. But by then, seniors will have become so accustomed to taking care of their finances online that the thought of going to a physical branch will be an unnecessary hassle.

Given that 79% of all consumers want their bank to offer more all-digital processes in the future, it’s very likely that senior citizens have also gained unprecedented comfort with digital banking due to necessity. Whether in a few months or a year or more, the coronavirus will no longer be a reason to turn to digital. But by then, seniors will have become so accustomed to taking care of their finances online that the thought of going to a physical branch will be an unnecessary hassle.

Despite record-high use of digital banking among senior citizens, lingering fears about online security lurk under the surface acceptance of digital tools. 10% of senior citizen bankers don’t feel online transactions are secure (even larger proportions see them as merely “somewhat secure” — also not a raging endorsement).

When asked to rank their top concerns regarding online security, the majority fear financial loss first (52%), and loss of privacy second (42%). Seniors, who are often on fixed incomes and may already feel financially vulnerable, may be especially worried about the potential monetary loss from online identity theft and the like.

To be sure, the majority of people do trust the security of online banking, including older adults. And it would be natural to ask the question, “If seniors continue to be concerned about the security of online banking, then why do they still engage in it?” It may be that seniors are happy to use digital bank tools for the most rudimentary tasks, such as checking their bank balance. But if seniors are avoiding opening a new account, transferring money, or other more “active” tasks due to security concerns, this represents lost opportunities for the bank.

Despite record-high use of digital banking among senior citizens, lingering fears about online security lurk under the surface acceptance of digital tools. 10% of senior citizen bankers don’t feel online transactions are secure (even larger proportions see them as merely “somewhat secure” — also not a raging endorsement).

When asked to rank their top concerns regarding online security, the majority fear financial loss first (52%), and loss of privacy second (42%). Seniors, who are often on fixed incomes and may already feel financially vulnerable, may be especially worried about the potential monetary loss from online identity theft and the like.

To be sure, the majority of people do trust the security of online banking, including older adults. And it would be natural to ask the question, “If seniors continue to be concerned about the security of online banking, then why do they still engage in it?” It may be that seniors are happy to use digital bank tools for the most rudimentary tasks, such as checking their bank balance. But if seniors are avoiding opening a new account, transferring money, or other more “active” tasks due to security concerns, this represents lost opportunities for the bank.

The best kind of secure online financial transaction is one that doesn’t get in customers’ way. Unfortunately, seniors are especially likely to suffer from access issues involving login, password, or security check difficulties, preventing them from even beginning the online banking task.

Seniors who are frequently asked to change their passwords, complete complicated security checks, or otherwise face security-driven obstacles are at risk of giving up on digital interactions. We found that 12% will ignore the transaction, 8% will abandon the process, and 11% will switch providers.

That’s why banks must add security features that don’t interfere with customers’ ease of use. For example, biometric security and facial recognition are all intuitive processes that can be completed from a single channel and don’t require seniors to remember complicated passwords or complete visually challenging security checks. Yet they remain woefully underused compared to more cumbersome password-based security.

The best kind of secure online financial transaction is one that doesn’t get in customers’ way. Unfortunately, seniors are especially likely to suffer from access issues involving login, password, or security check difficulties, preventing them from even beginning the online banking task.

Seniors who are frequently asked to change their passwords, complete complicated security checks, or otherwise face security-driven obstacles are at risk of giving up on digital interactions. We found that 12% will ignore the transaction, 8% will abandon the process, and 11% will switch providers.

That’s why banks must add security features that don’t interfere with customers’ ease of use. For example, biometric security and facial recognition are all intuitive processes that can be completed from a single channel and don’t require seniors to remember complicated passwords or complete visually challenging security checks. Yet they remain woefully underused compared to more cumbersome password-based security.

Seniors are best served by seamless digital processes that are predictable and intuitive to use. Photo ID verification and digital signatures are based on sophisticated technology that remains nonintrusive to the end-user. They are part of a larger end-to-end process that keeps seniors within a single seamless digital channel, such as a mobile phone or website.

Seniors are best served by seamless digital processes that are predictable and intuitive to use. Photo ID verification and digital signatures are based on sophisticated technology that remains nonintrusive to the end-user. They are part of a larger end-to-end process that keeps seniors within a single seamless digital channel, such as a mobile phone or website.