Survey Data Shows Mobile App Strategy is Failing Insurers & Brokers

By Gaby Young

Whether you’re shopping for that perfect Halloween costume, ordering take-out from your favorite restaurant, or eyeing flight and hotel deals for a weekend getaway, chances are you’re doing this from the one device you turn to most frequently - your mobile smartphone. And today that includes how you get your insurance done too.

85% of Americans today own a smartphone, while 57% spend 5 hours or more on their cell phone daily. Insurance customers in recent years have become used to quickly and intuitively engaging their insurer or broker and transacting business on their mobile - be they applying for a new policy or looking to report and resolve a claim.

When they don’t receive that seamless yet personalized convenience? They’re not satisfied, they’re loyalty evaporates, and they abandon to a competitor instead. Gone are the days when having a website or mobile app was a ‘wow factor’ seen ahead of its time. Today the entire experience for insurance customers needs to be not just digital but comprehensive: Customers need to be able to complete every requirement asked of them to resolve their request from their smartphone.

Current Solutions Are Not In-Step with Customers’ Mobile Needs

How are insurers and brokers keeping up with the expectations of today’s mobile-first customers?

Lightico recently surveyed insurance professionals across the United States to gauge the state of digital insurance and see how many customers are actually using mobile solutions offered by their providers.

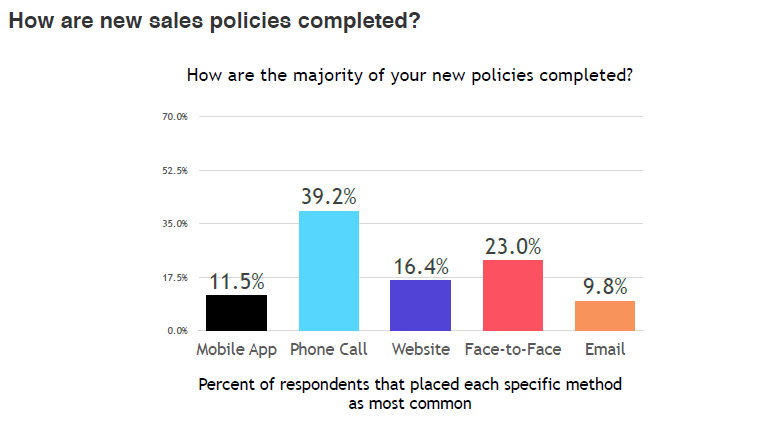

When it comes to new policy sales, merely 11% of professionals stated that new policies are completed on mobile. Just as surprisingly, only 16% indicated customers open a new insurance policy using a website. This leaves call center agents and office staff still handling the majority of new policy sales, meaning required forms and signatures, supporting documents and terms and conditions (T’s & C’s) are largely dependent on lengthy phone conversations and time-consuming paperwork for both employees and customers.

Enrolling new customers in the ways that are quickest and easiest for them is crucial to earning their loyalty. Just as critical is keeping current policyholders happy and during the times they need their provider most - when they need to file a claim for benefits.

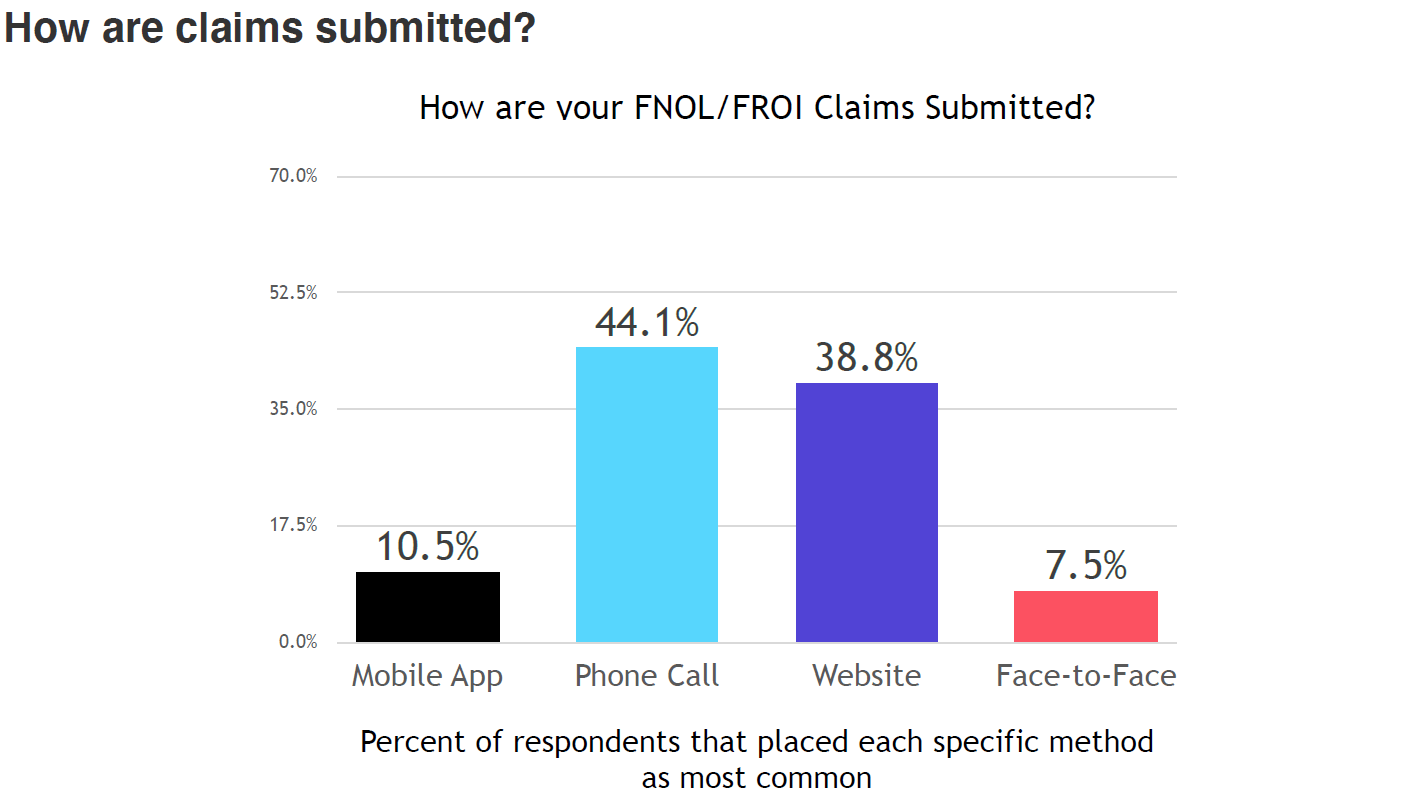

But when insurance employees were asked how First Notice of Loss (FNOL) and First Report of Injury (FROI) claims are currently being submitted at their company, only 10% responded that these claims are being submitted on mobile.

While insurance carriers and brokers have increased digital investment in recent years, these numbers expose that most insurers and brokers have yet to provide mobile solutions that are in-step with customer needs and so critical to driving adoption.

Insurance Journeys Full of Friction for Customers & Agents

With no convenient way to do business with insurers and brokers from their smartphones, customers are forced into high-effort interactions that demand time spent on the phone or visiting the office to go review a policy or claim in-person.

But doing business the old way comes at a significant cost for insurers and brokers: Completing all of the customer-facing steps needed to open a new policy or resolve claims locks both employees and the customers they serve into a broken journey full of paperwork and outdated legacy processes.

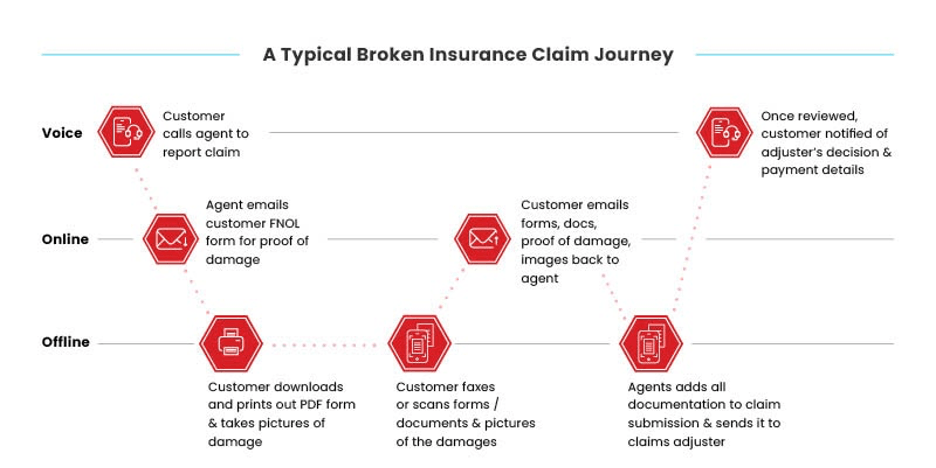

Customers are bounced across channels, from the contact center, to their email just to access the forms and agreements they need to complete or sign. They often are also required to provide supporting documents to get approved or have their request for benefits processed.

This makes it impossible to complete all of these requirements in one channel - instead customers must hunt down solutions like fax and scanning machines that remind them more of the 80s and 90s rather than today’s mobile and digital world.

What do these broken journeys look like? Here’s what insurance customers typically must go through just to file an FNOL claim:

But what about eSignature apps?

Many insurers have invested in eSignature apps the past few years. Why then does the data reveal dramatically low customer mobile app adoption rates? Here 4 main reason why:

1)eSign apps are incomplete: esignature apps cover one step of many a customer needs to complete when applying for a new insurance policy or making a claim. They still need to provide IDs for verification, a myriad of supporting documents (e.g. death certificate for life insurance claims, hospital bills for health insurance claims), and consenting to binding terms and conditions.

2) Lack integration and are neither fully digital or seamless: Esign apps are not integrated smoothly with other business workflows and require multiple steps and touchpoints, frustrating customers while prolonging turnaround times.

3) Cumbersome PDF forms defeat the purpose of mobile: Esign apps rely on legacy processes like email and PDF-based forms. Reading and understanding long and cumbersome agreements in a clunky PDF form on your 6 inch smartphone screen? That’s a customer experience no-go. Most customers will delay completing the process - eventually many choose to print off those forms which means they’ll need to find a fax or scanning machine to send them back.

4) Force customers to the app store for a one-time event: Having to toggle from your insurance policy application to the app store just to sign it is hardly seamless. And no customer enjoys having to download and store an esignature app on their personal phone for what essentially is a one-time use.

To Compete, Insurers Need A Completely New Mobile Strategy

To do away with disjointed journeys that waste valuable time for customers and employees while racking up adding overhead and management costs, insurers and brokers need to leave digital silos and legacy processes behind and leverage completely end-to-end Digital Completion technology.

Instead of driving customers on errands that encompass multiple channels, flood your contact centers, inflate your average call handle (ACH) times, and produce paperwork that delays resolution and complicates compliance, your customers can complete all steps of a policy sale or claim from the device they’re most comfortable with - their smartphone.

Agents can send customers an SMS or email link which instantly starts a digital session optimized for mobile, that guides them every step of the way. Customers can sign and complete forms within this interactive session, upload supporting documents or evidence directly, and digitally consent to new terms and conditions. ID verification is as simple as snapping a selfie and taking a picture of their government-issued identification card.

Gone is the need for customers to download eSign apps that merely fulfill one small step in the process are based on legacy PDF forms that end up being printed, allowing insurers and brokers to dramatically speed completion times by 85% and reduce touchpoints by 60%, helping them meet the mobile needs of today’s customers and win their long-term loyalty.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

When it comes to new policy sales, merely 11% of professionals stated that new policies are completed on mobile. Just as surprisingly, only 16% indicated customers open a new insurance policy using a website. This leaves call center agents and office staff still handling the majority of new policy sales, meaning required forms and signatures, supporting documents and terms and conditions (T’s & C’s) are largely dependent on lengthy phone conversations and time-consuming paperwork for both employees and customers.

When it comes to new policy sales, merely 11% of professionals stated that new policies are completed on mobile. Just as surprisingly, only 16% indicated customers open a new insurance policy using a website. This leaves call center agents and office staff still handling the majority of new policy sales, meaning required forms and signatures, supporting documents and terms and conditions (T’s & C’s) are largely dependent on lengthy phone conversations and time-consuming paperwork for both employees and customers.

Enrolling new customers in the ways that are quickest and easiest for them is crucial to earning their loyalty. Just as critical is keeping current policyholders happy and during the times they need their provider most - when they need to file a claim for benefits.

But when insurance employees were asked how First Notice of Loss (FNOL) and First Report of Injury (FROI) claims are currently being submitted at their company, only 10% responded that these claims are being submitted on mobile.

Enrolling new customers in the ways that are quickest and easiest for them is crucial to earning their loyalty. Just as critical is keeping current policyholders happy and during the times they need their provider most - when they need to file a claim for benefits.

But when insurance employees were asked how First Notice of Loss (FNOL) and First Report of Injury (FROI) claims are currently being submitted at their company, only 10% responded that these claims are being submitted on mobile.

While insurance carriers and brokers have increased digital investment in recent years, these numbers expose that most insurers and brokers have yet to provide mobile solutions that are in-step with customer needs and so critical to driving adoption.

While insurance carriers and brokers have increased digital investment in recent years, these numbers expose that most insurers and brokers have yet to provide mobile solutions that are in-step with customer needs and so critical to driving adoption.