Top 5 Reasons Investing in Frontend Tech is the Fastest Path to ROI for P&C

By Leor Melamedov

When insurance companies think about digital transformation, they often think about digitizing core systems.

While IT changes such as implementing robotic process automation (RPA) can help automate time-consuming back office tasks, a complete digital overhaul of the backend can be incredibly expensive, with the largest insurance companies spending on average between $10 million to $20 million on RPA systems annually.

The good news is that insurers can reduce friction, boost sales, shrink time to settlement, and improve the agent and customer experience by focusing on the frontend. Many frontend technologies seamlessly sync with existing core systems. Best of all, it’s far more cost- and time-efficient than trying to overhaul legacy IT systems. Here’s why:

Customer-centricity

Source: Bain.

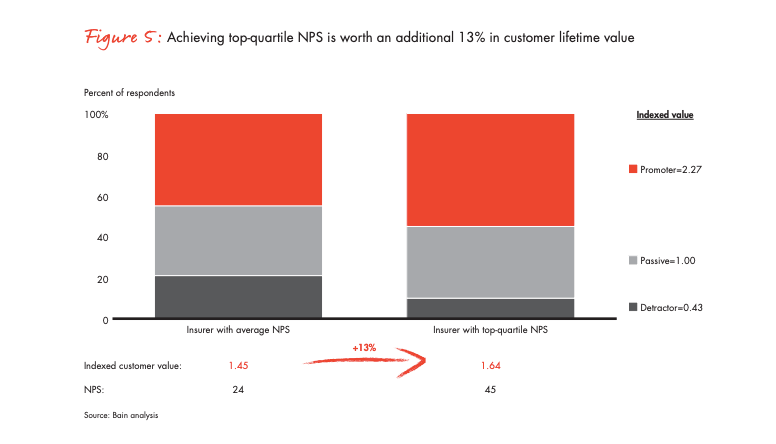

Net promoter score (NPS) measures customers’ satisfaction with the brands they interact with and is an easy way of quantifying the customer-centricity of a company. Customers don’t know what’s going on in their insurer’s backend, but the quality of their frontend experience determines the NPS they’ll give.

Customers’ expectations for an easy, enjoyable, and digital insurance experience are at an all-time high. This is likely due to a combination of the ascent of digitization in all areas of customers’ lives, as well as the coronavirus that drove demand for streamlined remote transactions across all demographic groups.

Yet a Lightico survey conducted in Spring 2020 found that a mere 34% of insurance customers could easily communicate with their insurers with questions or changes to their policies.

Insurers aren’t consistently using the digital channels their customers want, with 50% of insurance companies failing to meet consumer demand for online chat servicing and 25% behind on consumer demand for website servicing.

Insurers can do better. And those that do will be handsomely rewarded.

Bain research found that a promoter is potentially worth five times more than a detractor in lifetime value. This is mostly thanks to better retention, which means premiums are paid for more years. For example, in car insurance, 44% of all promoters stay with their insurer for longer than 6 years, compared with a mere 27% of detractors.

2. Higher conversion rates

Customer acquisition costs are sky-high. Depending on the business model of the particular insurer, average costs can vary between $487 and $900 per customer. This might be justifiable if most prospective customers end up converting and becoming long-term customers. But the reality is that they don’t.

A whopping 45% of potential customers who show initial interest in an insurance plan ultimately fail to convert. In some cases, of course, this can be chalked up to finding better rates elsewhere. But oftentimes poor application completion rates are a direct result of cumbersome and time-consuming paperwork processes.

And don’t forget: it’s not just marketing dollars that are wasted when prospects don’t convert. It’s the entire potential customer lifetime value (CLV) that evaporates due to needless friction.

Insurance agents can increase their rate of closed sales by moving to streamlined, digital processes that can be completed from any location. A customer that has to wait for computer, scanner, or fax access is a customer that’s more likely to get away. That means insurers need to offer mobile-optimized forms, documents, and signatures that the customer can fill out while on the sales call, when interest and intent to buy is highest.

3. Easy compliance

Insurance is a heavily regulated industry. The General Data Protection Regulation (GDPR) went into effect on May 25. 2018, and the California Consumer Privacy Act (CCPA) on January 1, 2020. To add to the complication, states across the country often have their own variations of privacy laws. Staying compliant is key to avoiding hefty fines and reputational damage, but it always seems like a moving target.

Frontend technology can ensure insurance companies stay compliant without adding additional time-draining requirements to the onboarding or first notice of loss (FNOL) process.

First, digital forms and documents sync with insurance companies’ CRMs, making it easy to securely store and retrieve sensitive customer data.

Second, electronic documents come with a timestamped, tamper-proof paper trail that holds up in a court of law and prevents disputes.

Third, electronic ID verification can now be easily completed by enabling the policyholder to text their insurance agent a picture of a photo ID and selfie taken in “live” mode for instant verification. This makes it possible for insurers to follow AML and KYC procedures remotely and digitally.

4. Faster time to settlement

The faster insurance companies settle a claim, the faster they can move on to new claimants and the fewer overhead costs they accrue. An insufficiently digital claims process is notoriously slow. Chasing customers to complete paper forms or PDFs and dealing with the back-and-forth of error-laden forms prolongs the final settlement. It’s also costly — studies show that reworking a claim costs $25, in addition to all the manpower hours needed. This can add up to thousands of dollars a month.

On the other hand, customers who are able to instantly complete the entire FNOL process from their mobile with an agent guiding them on the phone are far less likely to make errors, forget a piece of documentation, or require later follow up and chasing. Time is money, and digital frontend technology saves both.

5. More referrals

Medallia research found that nearly 60% of customers expect real-time interactions with their insurance providers. There is a close link between instant digitized processes and satisfaction — and there’s a close link between satisfaction and referrals. Among consumers who reported a positive experience with an insurer in the last year, 44% say they told friends and family about it.

Word-of-mouth referrals account for 20% to 50% of all purchasing decisions, according to Jacques Bughin, Jonathan Doogan and Ole Jørgen Vetvik at McKinsey. Referrals are both an extremely effective and cost-effective way of generating new business. But it doesn’t happen unless existing customers are happy.

Imagine a customer is involved in a car accident that results in major damage to all cars involved. This is a stressful situation to be in. Here are two scenarios:

The insurance company is the “necessary evil”: adding stress by bouncing the policyholder through different touchpoints and requiring documents to be printed or scanned.

The insurance company is the unexpected hero: removing stress by allowing the customer to use their smartphone at the site of the incident to instantly send photos, videos, and FNOL forms to their insurer — no printers, scanners, or physical forms required.

When all is said and done, which scenario would turn the policyholder into a vocal advocate for the insurance company? The answer is clear.

The immediate impact of a digital frontend

Digital frontend technologies help expedite the insurance sales and claims filing process, improve customer satisfaction, reduce costs, and maximize profits.

Madanes is an insurance company that switched to digital signatures and forms and quickly started closing 50% more policies on the first call, and reducing customer processing time by 80%. Sure enough, their referral rates shot through the roof, growing by 300%.

That’s the kind of immediate ROI insurers get when they move to digital processes.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.