What’s The True Cost of Delaying A Digital Transformation in P&C Insurance?

By Leor Melamedov

Property and casualty insurance companies that contemplate a digital transformation are often lured by the prospect of better customer experience and efficiency — or the vague sense that it’s something they should be doing. Yet these somewhat nebulous-sounding goals make it easy to think digital transformation is something insurers can get around to at some point, or dabble in.

For that reason, it may be more useful for insurance companies to consider what they stand to lose by postponing a full digital transformation. There is a very real financial impact of failing to sufficiently digitize. Here are some of the biggest cost-drainers to watch out for.

Diminished customer lifetime value (CLV)

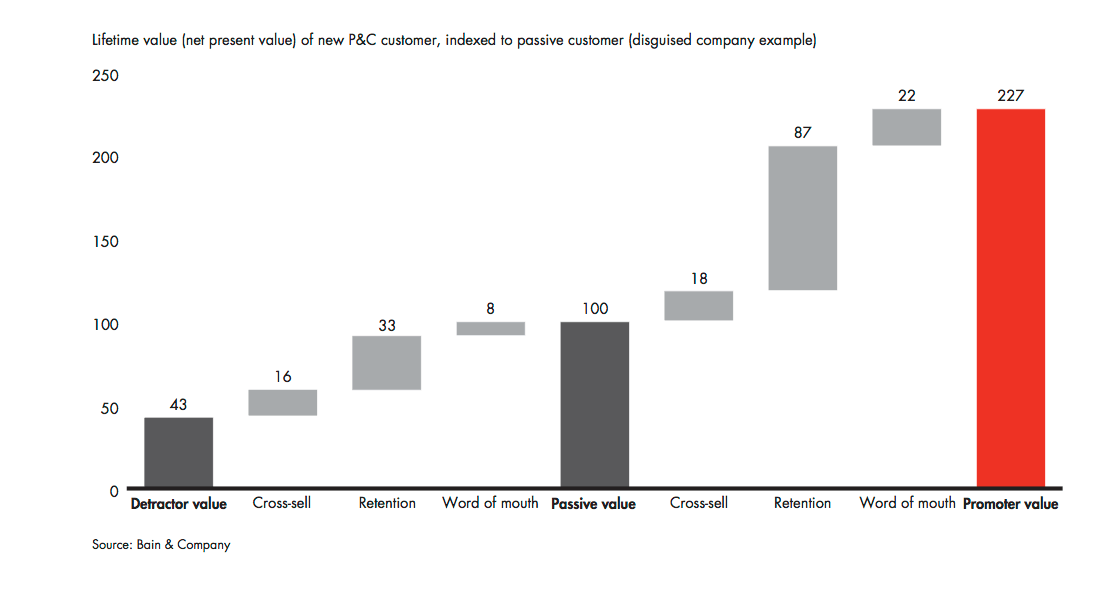

Customer lifetime value (CLV) is the sum of the insurance premium a customer pays plus the value of upsell opportunities (i.e., new or expanded policies). According to Bain research, a promoter is potentially worth five times more than a detractor in lifetime value. This means the insurance customer experience is now a financial imperative.

There are two main times when an insurance company risks losing or diminishing the CLV: during the customer onboarding process and after a negative claim filing process.

At the point of onboarding

The average insurer’s customer acquisition cost when an independent agent is involved is $900. That’s a lot of marketing and sales dollars that go into attracting prospective customers.

Yet 45% of prospective customers who shop for insurance fail to convert. This is at least partially due to onboarding processes that are too cumbersome, paperwork-heavy, or involve jumping from channel to channel, leading to low completion rates. Not only does the marketing budget go down the drain: customers that fail to convert take all that unfulfilled CLV with them and bring it to the competition.

At the point of claims

Customers go years dutifully paying for insurance without ever filing a claim. The average homeowner files a claim every nine or 10 years; for car owners, it’s a mere every 17.9 years.

Unlike other service providers that have more regular interactions with customers, insurance companies have limited opportunities to make or break their customers’ opinion of them.

A First Notice of Loss (FNOL) process that requires customers to go through multiple channels (e.g., email, scanner, phone, fax), fails to update customers as to the status of their claim, or makes it difficult to send supporting information at a later time will tarnish the customer’s perception of their insurer.

After they reach a settlement, these customers who are left with a bad taste in their mouth will be more likely to actively search for a new provider or be receptive to other providers’ marketing efforts. Prominent digital-first insurance companies such as Lemonade that boast a minutes-long, paperwork-free claims process are just waiting in the wings for these disgruntled customers to show up at their doorstep.

Unfortunately, customer churn is a significant expense that can’t simply be recouped via new customers.

As Lynn Thomas, president at 21st Century Management Consulting observes, “The insurance industry has the highest customer acquisition costs of any industry. It costs seven to nine times more for an insurance agency to attract a new customer than to retain one.”

2. Additional Living Expenses (ALE)

Many insurance policies require the insurer to cover temporary costs, such as a rental car or housing in the event of an incident or disaster. If insurers settle the claim quickly and efficiently, the ALE can be minimized. However, if the time to settlement is prolonged, insurance companies will have to foot the bill for a more extended period of time.

3. Processing costs

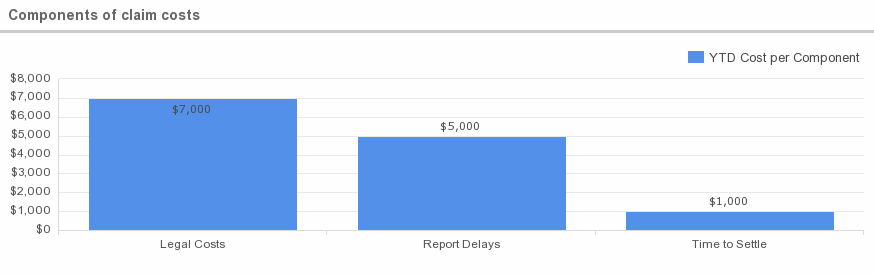

"Time to settle and report delays cost insurers $6,000 each year."

Source: Guiding Metrics

The operational and processing costs of traditional insurance processes can really add up. Here are just some of the costs incurred with clunky, nondigital claims processes:

Manual data entry takes up time for agents, underwriters, and other parties in the insurance cycle. This manpower cost cannot be overstated.

High error rates: According to some estimates, 60% of physical forms and documents contain errors or omissions. When these inevitably appear during the onboarding or claims processing cycle, agents must chase customers, wait for the corrected paperwork to be resubmitted, and process it over again.

Lack of integration: Legacy systems that drive core processes and frontend solutions should sync together seamlessly. Far too often they don’t, prolonging and complicating processes.

Difficulty in updating changing compliance regulations: Changing compliance regulations may necessitate insurance companies to update their forms, documents, disclosures, and procedures. Outdated manual processes make it a challenge to quickly adapt to changes in compliance requirements.

Costly Robotic Process Automation (RPA): When insurance companies think of going digital, they often think of RPA, which integrates the backend with the frontend. However, it can be incredibly expensive, with the largest insurance companies planning to invest $10 to $20 million annually in RPA alone. A digital frontend that integrates seamlessly with existing core systems can provide a similar function to RPA at a fraction of the cost.

Tackling these areas can dramatically shrink bloated processing costs. In fact, McKinsey research has found that increasing automation and digitizing processes can result in savings of up to 80% -- a significant ROI.

Nondigital is expensive

Insurance companies that put off enacting a full digital transformation aren’t just missing out on the benefits of digitization, such as better NPS, faster time to settlement, and fewer touchpoints. Failing to digitize is financially costly, and insurance companies foot the bill in terms of lost premiums, difficulty with conversions, prolonged periods of paying AML, and needless processing costs. Going digital isn’t a mere trend — it’s a critical component of reducing bloated costs.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Customer lifetime value (CLV) is the sum of the insurance premium a customer pays plus the value of upsell opportunities (i.e., new or expanded policies). According to Bain research, a promoter is potentially worth five times more than a detractor in lifetime value. This means the insurance customer experience is now a financial imperative.

There are two main times when an insurance company risks losing or diminishing the CLV: during the customer onboarding process and after a negative claim filing process.

Customer lifetime value (CLV) is the sum of the insurance premium a customer pays plus the value of upsell opportunities (i.e., new or expanded policies). According to Bain research, a promoter is potentially worth five times more than a detractor in lifetime value. This means the insurance customer experience is now a financial imperative.

There are two main times when an insurance company risks losing or diminishing the CLV: during the customer onboarding process and after a negative claim filing process.

Source: Guiding Metrics

The operational and processing costs of traditional insurance processes can really add up. Here are just some of the costs incurred with clunky, nondigital claims processes:

Source: Guiding Metrics

The operational and processing costs of traditional insurance processes can really add up. Here are just some of the costs incurred with clunky, nondigital claims processes: