Property and casualty (P&C) insurance companies have to juggle many complex processes, and it’s not easy. Between closing new policies, modifying existing policies, and processing claims, taking care of policyholders’ losses and potential losses is a heavy responsibility.

In addition, combating fraud, maintaining compliance, and boosting efficiency are constants that can’t be overlooked.

In this article, we have selected statistics that will help P&C companies assess their current priorities based on the real, quantifiable impact these issues have on their business.

Thirty percent of the people are honest, 30% are dishonest, and 40% are situationally honest or dishonest. That means that 70% of the people could commit fraud if given the opportunity (Source: PropertyCasualty360).

The takeaway: Many insurance fraudsters are situational criminals, not professionals, and can be effectively deterred by tough compliance measures.

2. The total cost of insurance fraud in the U.S. (excluding health insurance) is estimated to be more than $40 billion per year, costing the average U.S. family between $400 and $700 annually in the form of increased premiums. (Source: FBI)

The takeaway: Insurance fraud doesn’t just cost insurance companies in terms of hefty penalties. It also costs innocent policyholders and may make some policies prohibitively expensive.

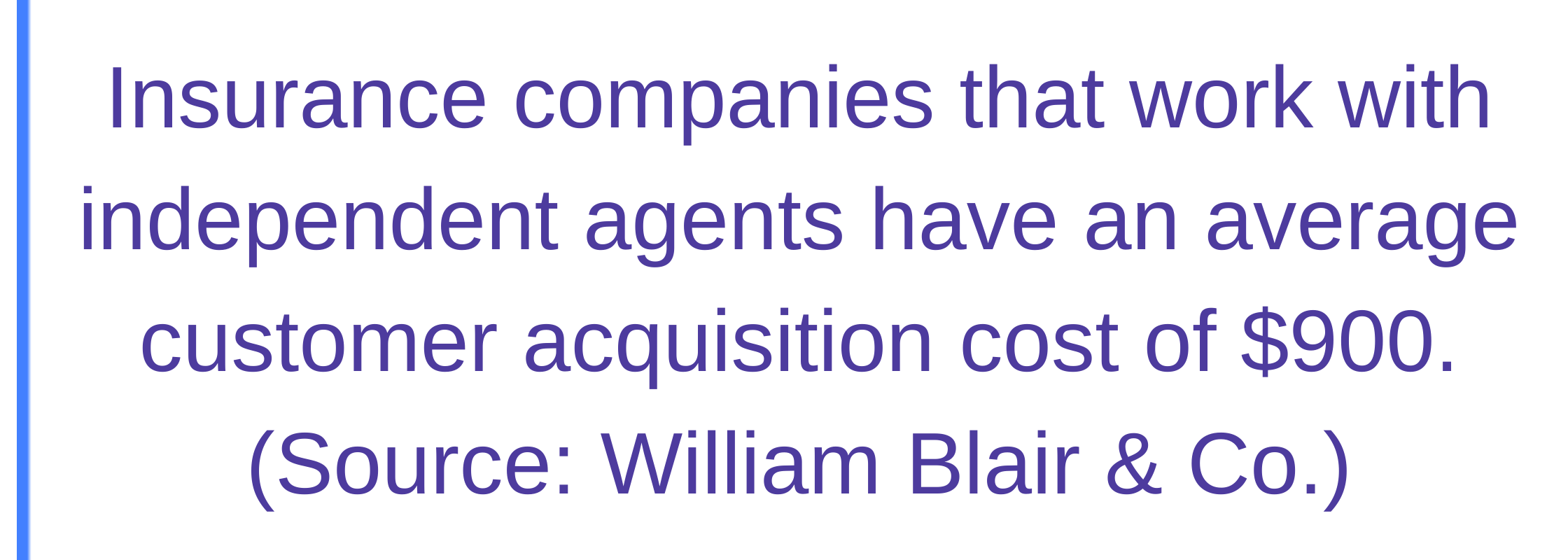

3.The takeaway: Acquiring new prospective customers is expensive — prevent them from dropping out before they’ve even converted by facilitating an intuitive and digital onboarding process.

4. The average homeowner files a property insurance claim every nine or ten years. (Source: Zacks).

The takeaway: Homeowners rarely file claims, so when they do, be sure their experience is a great one.

5. The average motorist files an auto insurance claim every 17.9 years. (Source: Coverhound)

The takeaway: Car owners file claims even less frequently than homeowners, so when they do, be sure their experience is a great one.

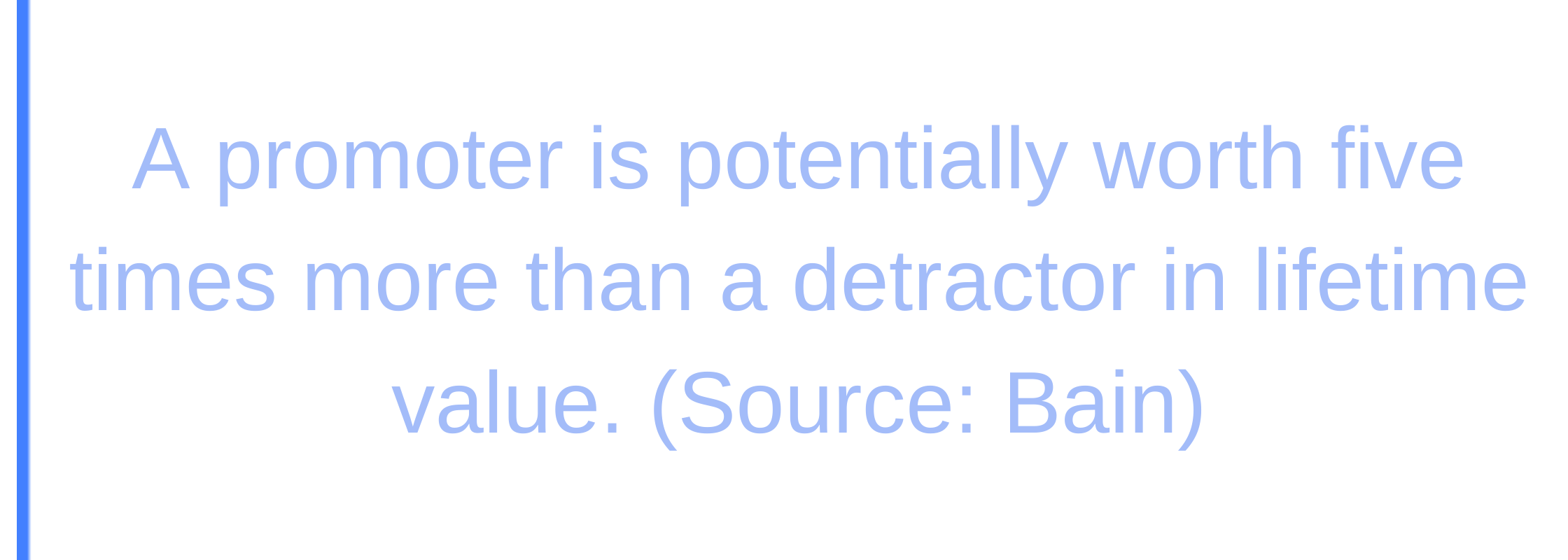

6. The takeaway: A quality customer experience, as measured by the net promoter score (NPS), is intrinsically tied with more revenue for insurers.

7. 41% of P&C policyholders who submit a claim are likely to switch insurers within 12 months. (Source: Accenture)

The takeaway: Policyholders generally stick with their insurance provider — unless a bad claim filing experience gives them a reason not to.

8. 83% of P&C policyholders who report dissatisfaction with the way their claim is handled said they had switched or planned to switch to another insurer. (Source: Accenture)

The takeaway: A bad claim filing experience is the fastest way to get a customer to churn.

9. The largest organizations plan to invest $10 million to $20 million annually in robotic process automation, or RPA systems alone (Source: protiviti)

The takeaway: RPA systems can help insurance companies automate routine back-office processes, but they are expensive. Smaller insurers may want to consider more cost-effective ways of boosting their efficiencies.

10. The national average cost for home insurance is $2,305 annually. (Source: Insurance.com)

The takeaway: P&C insurers enjoy regular income from policyholders who rarely submit claims. Take care of customers during that rare claim process, and insurance companies can enjoy predictable revenue from loyal customers.

11. It costs seven to nine times more for an insurance company to attract a new customer than to retain an existing one. (Source: ITL)

The takeaway: Efficient service, digitized processes, and fast time to settlement all prevent policyholders from churning. These efforts are financially worthwhile.

12. Nearly 60% of customers expect real-time interactions with their insurance providers. (Source: Medallia)

The takeaway: Today’s mobile customers want to buy insurance and submit claims as soon as they’re ready. They don’t want to wait to deal with cumbersome paperwork or get in front of a computer.

13. Word-of-mouth referrals account for 20% to 50% of all purchasing decisions. (Source: McKinsey)

The takeaway: Happy existing customers = more new customers without the expense of marketing.

14. During the coronavirus lockdown, just 34% of insurance customers could easily communicate with their insurers with questions or changes to their policies. (Source: Lightico)

The takeaway: Policyholders will remember which providers made it easy for them to do business safely during their time of need.

15. 50% of insurance companies are failing to meet consumer demand for online chat servicing and 25% are behind on consumer demand for website servicing. (Source: Lightico)

The takeaway: Insurance customers expect fast and reliable digital communication with their providers.

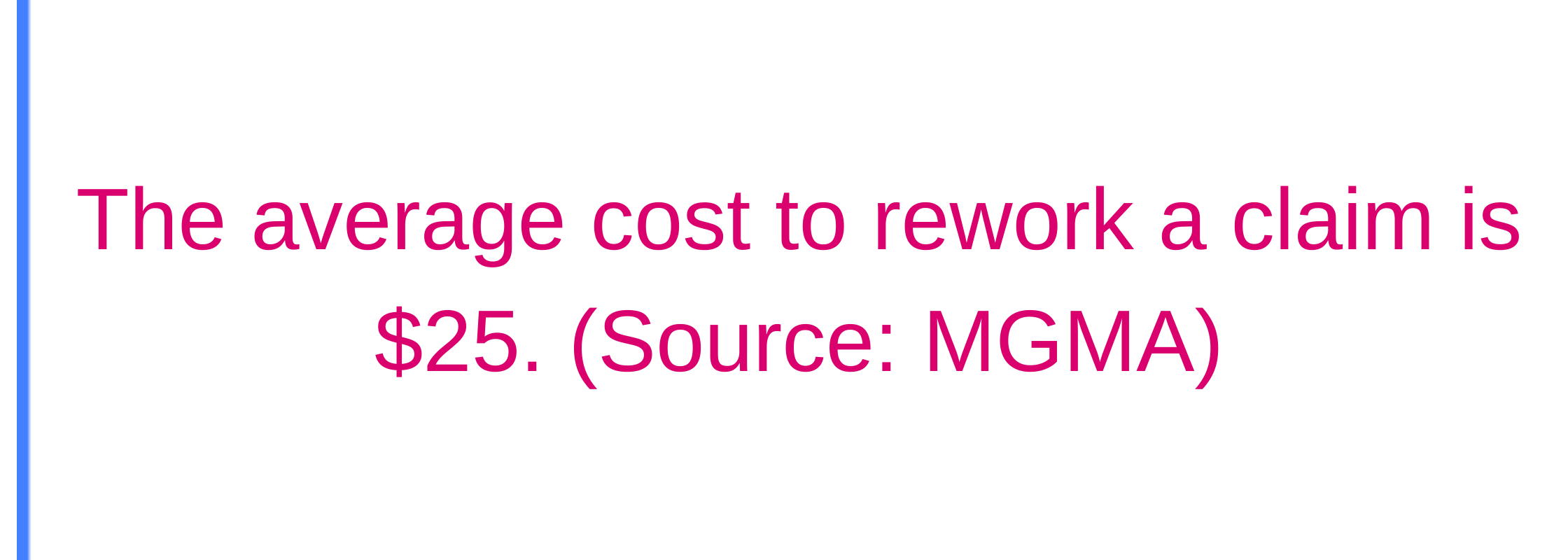

16. The takeaway: Prevent costly and time-consuming not-in-good-order (NIGO) reports by enabling mobile-optimized forms that are easy to understand and correct.

The importance of making data-based decisions

Insurance companies can lower costs, improve efficiencies, and create delightful customer journeys by paying attention to objective indicators of what works and what doesn’t. Concepts like customer experience and digital transformation encompass so much that they are often overwhelming. But looking at the numbers can allow insurance companies to focus on what really matters when making business improvements.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

The takeaway: Acquiring new prospective customers is expensive — prevent them from dropping out before they’ve even converted by facilitating an intuitive and digital onboarding process.

4. The average homeowner files a property insurance claim every nine or ten years. (Source: Zacks).

The takeaway: Homeowners rarely file claims, so when they do, be sure their experience is a great one.

5. The average motorist files an auto insurance claim every 17.9 years. (Source: Coverhound)

The takeaway: Car owners file claims even less frequently than homeowners, so when they do, be sure their experience is a great one.

6.

The takeaway: Acquiring new prospective customers is expensive — prevent them from dropping out before they’ve even converted by facilitating an intuitive and digital onboarding process.

4. The average homeowner files a property insurance claim every nine or ten years. (Source: Zacks).

The takeaway: Homeowners rarely file claims, so when they do, be sure their experience is a great one.

5. The average motorist files an auto insurance claim every 17.9 years. (Source: Coverhound)

The takeaway: Car owners file claims even less frequently than homeowners, so when they do, be sure their experience is a great one.

6.  The takeaway: A quality customer experience, as measured by the net promoter score (NPS), is intrinsically tied with more revenue for insurers.

7. 41% of P&C policyholders who submit a claim are likely to switch insurers within 12 months. (Source: Accenture)

The takeaway: Policyholders generally stick with their insurance provider — unless a bad claim filing experience gives them a reason not to.

8. 83% of P&C policyholders who report dissatisfaction with the way their claim is handled said they had switched or planned to switch to another insurer. (Source: Accenture)

The takeaway: A bad claim filing experience is the fastest way to get a customer to churn.

The takeaway: A quality customer experience, as measured by the net promoter score (NPS), is intrinsically tied with more revenue for insurers.

7. 41% of P&C policyholders who submit a claim are likely to switch insurers within 12 months. (Source: Accenture)

The takeaway: Policyholders generally stick with their insurance provider — unless a bad claim filing experience gives them a reason not to.

8. 83% of P&C policyholders who report dissatisfaction with the way their claim is handled said they had switched or planned to switch to another insurer. (Source: Accenture)

The takeaway: A bad claim filing experience is the fastest way to get a customer to churn.

9. The largest organizations plan to invest $10 million to $20 million annually in robotic process automation, or RPA systems alone (Source: protiviti)

The takeaway: RPA systems can help insurance companies automate routine back-office processes, but they are expensive. Smaller insurers may want to consider more cost-effective ways of boosting their efficiencies.

10. The national average cost for home insurance is $2,305 annually. (Source: Insurance.com)

The takeaway: P&C insurers enjoy regular income from policyholders who rarely submit claims. Take care of customers during that rare claim process, and insurance companies can enjoy predictable revenue from loyal customers.

11. It costs seven to nine times more for an insurance company to attract a new customer than to retain an existing one. (Source: ITL)

The takeaway: Efficient service, digitized processes, and fast time to settlement all prevent policyholders from churning. These efforts are financially worthwhile.

12. Nearly 60% of customers expect real-time interactions with their insurance providers. (Source: Medallia)

The takeaway: Today’s mobile customers want to buy insurance and submit claims as soon as they’re ready. They don’t want to wait to deal with cumbersome paperwork or get in front of a computer.

13. Word-of-mouth referrals account for 20% to 50% of all purchasing decisions. (Source: McKinsey)

The takeaway: Happy existing customers = more new customers without the expense of marketing.

14. During the coronavirus lockdown, just 34% of insurance customers could easily communicate with their insurers with questions or changes to their policies. (Source: Lightico)

The takeaway: Policyholders will remember which providers made it easy for them to do business safely during their time of need.

15. 50% of insurance companies are failing to meet consumer demand for online chat servicing and 25% are behind on consumer demand for website servicing. (Source: Lightico)

The takeaway: Insurance customers expect fast and reliable digital communication with their providers.

16.

9. The largest organizations plan to invest $10 million to $20 million annually in robotic process automation, or RPA systems alone (Source: protiviti)

The takeaway: RPA systems can help insurance companies automate routine back-office processes, but they are expensive. Smaller insurers may want to consider more cost-effective ways of boosting their efficiencies.

10. The national average cost for home insurance is $2,305 annually. (Source: Insurance.com)

The takeaway: P&C insurers enjoy regular income from policyholders who rarely submit claims. Take care of customers during that rare claim process, and insurance companies can enjoy predictable revenue from loyal customers.

11. It costs seven to nine times more for an insurance company to attract a new customer than to retain an existing one. (Source: ITL)

The takeaway: Efficient service, digitized processes, and fast time to settlement all prevent policyholders from churning. These efforts are financially worthwhile.

12. Nearly 60% of customers expect real-time interactions with their insurance providers. (Source: Medallia)

The takeaway: Today’s mobile customers want to buy insurance and submit claims as soon as they’re ready. They don’t want to wait to deal with cumbersome paperwork or get in front of a computer.

13. Word-of-mouth referrals account for 20% to 50% of all purchasing decisions. (Source: McKinsey)

The takeaway: Happy existing customers = more new customers without the expense of marketing.

14. During the coronavirus lockdown, just 34% of insurance customers could easily communicate with their insurers with questions or changes to their policies. (Source: Lightico)

The takeaway: Policyholders will remember which providers made it easy for them to do business safely during their time of need.

15. 50% of insurance companies are failing to meet consumer demand for online chat servicing and 25% are behind on consumer demand for website servicing. (Source: Lightico)

The takeaway: Insurance customers expect fast and reliable digital communication with their providers.

16.  The takeaway: Prevent costly and time-consuming not-in-good-order (NIGO) reports by enabling mobile-optimized forms that are easy to understand and correct.

The takeaway: Prevent costly and time-consuming not-in-good-order (NIGO) reports by enabling mobile-optimized forms that are easy to understand and correct.