7 Ways to Create an Unforgettable Onboarding Experience For New CU Members

By Leor Melamedov

While many bank customers may be happy with a simple and efficient onboarding experience, credit union members typically have higher expectations.

Not only do members want to be onboarded in a speedy manner, but they are also typically looking for an exceptionally personalized level of service. Today’s “new normal,” characterized by remote-first business transactions, can actually be an opportunity for credit unions to onboard new members with both greater efficiency and personalization.

Here, we will explore the top seven things credit unions can do right now to create delightful onboarding experiences for their new members.

First, The Good News: Credit Unions Are Already Better Than Banks At Digital Onboarding

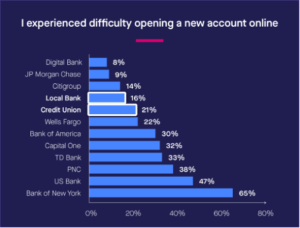

Lightico conducted a survey of 1,007 Americans representing a cross-section of the population. Consumers were asked to identify their current bank out of top ten banks in the United States, while “local bank” “credit union” and “digital-only bank” were grouped into three separate options.

The study revealed that credit unions outperform most banks when it comes to easy digital account opening. Only 21% of credit union members experienced difficulty during online onboarding.

Nonetheless, digital banks still outrank credit unions in this area, showing that credit unions can still benefit from optimizing their onboarding flows.

For credit unions to go from good to great, they should consider the following onboarding best practices:

1. Don’t Shy Away From Technology

Credit unions shouldn’t be afraid to embrace onboarding software to remove onboarding friction. Far too often, credit unions rely on their loan origination system (LOS) to do double duty, but this is a mistake. Onboarding is a unique moment in the member’s lifecycle, and the tech stack that credit unions use for it should reflect this. Investing in technology doesn’t mean investing less in human-to-human service.

2. Use Conditional Logic in eForms

Credit unions frequently have unique criteria for accepting new members. The onboarding form is the best place to uncover early on whether the prospective member shares a “field of membership,” and provide automated next steps. Below are two examples of business rules that can be applied to eForms to automatically determine membership eligibility:

If the customer is a member of First Baptist Church, then additional form fields appear.

Ifthe customer is not a member of First Baptist Church, then a field appears asking if they would like to join. If they say “yes,” then a trigger for joining the church appears.

While nonmembers can sometimes join churches, volunteer organizations, and so on in order to become eligible for the credit union, some criteria are harder, if not impossible to meet.

For instance, nonmembers are not going to change their geographic residence or place of employment to join a credit union. eForms that include this as a mandatory “field of membership” should use it to exclude eligibility. For instance:

Ifthe customer is an employee of Acme Company, then additional form fields appear.

If the customer is not an employee of Acme Company, then additional fields remain hidden and the nonmember is informed of non-eligibility.

By employing conditional logic in smart forms, credit unions can ensure potential members are aware of eligibility requirements early on in the application process.

3. Harness Automated Workflows For Document Collection

KYC requirements demand that credit unions conduct due diligence when onboarding new members. This often translates into requirements for additional documentation during the account opening process, especially for business accounts or higher-risk members. Automated workflows can be easily set up to prompt credit union staff to request relevant supporting documents based on the member’s risk profile and credit union needs.

This prevents credit union staff from having to follow up with prospective members at a later time for additional documents. It also significantly saves time on both the staff and member end, as KYC expectations are clear to everyone from the beginning.

In addition, rules can be set up to trigger requests for eSignatures on documents, if needed.

4. Digitally Verify Member ID

Every aspect of the member onboarding experience should be frictionless, including ID verification. Credit union members should be able to instantly submit their government-issued photo ID for automatic verification from their smartphone — whether they’re onboarding at a credit union branch or remote.

Here’s how the process of digital ID verification works:

A credit union associate sends the prospective member a text message containing a link that opens to a secure virtual session.

The member opens that link, snaps a picture of their photo ID using their smartphone, and uploads it to the mobile session.

The member then takes a selfie using “live” mode and uploads it to the mobile session.

An AI-powered photo ID algorithm scans the two images and determines whether there is a match.

Having such an intuitive ID verification system in place makes it easy for credit unions to protect themselves from fraud while promoting a streamlined credit union member experience.

Used in tandem with behind-the-scenes checks with agencies like ChexSystems, credit unions can quickly build a profile of a prospective member.

5. Collect The First Payment Effortlessly

Once a new credit union member’s account is created, they’ll need to submit the initial payment. It should be easy for new members to make that minimum deposit without having to visit a physical branch. Credit unions can enable members to pay securely directly from their smartphones in real-time. Digital payment systems are also highly secure and PCI-DSS compliant. Customer card details are secure without any exposure to agents or the business.

6. Automate Cross-Selling

Once members have onboarded, it’s not too early to begin cross-selling. In fact, it’s just the right time. Credit unions have just received plenty of information about their new members, which they can use to make relevant recommendations for products and services. Credit unions with an automated workflow solution can set up business rules that trigger recommendations to members based on their unique characteristics.

For example, if a new member recently purchased a home, the credit union can offer a home renovation loan. Or if a new member just retired, the credit union can recommend relevant financial services. Cross-selling at a credit union should cater to members’ life stages — and automation can make that easier.

7. Stay Human

When credit unions adopt technology, they’ll want to make sure it’s supported by friendly and caring credit union staff. Associates should always be available to guide new members through the digital onboarding process via phone conversation, helping them through their application and answering questions along the way. The best onboarding software will allow associates and members to co-view and collaborate on applications in real-time.

Once the account is open, credit union staff can offer discounts at stores, access to travel agents, special rates, and other white-glove services that make members feel cared for. And with the bureaucratic aspects of onboarding automated, staff will have more time for these “extras” that make all the difference.

The Takeaway

A combination of digital tools, automated workflows, and world-class staff can ensure an unforgettable onboarding experience for credit union members. Onboarding sets the stage for the entire relationship, and members won’t soon forget an especially seamless and delightful account opening process. When new members eventually need a loan, credit card, or service, they’ll be eager to reengage their credit union.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

For credit unions to go from good to great, they should consider the following onboarding best practices:

For credit unions to go from good to great, they should consider the following onboarding best practices: