What the U.S. Treasury's Deepfake Alert Means for Auto Loan Funding Reviews

Auto lenders have spent years hardening identity verification. The documents now arriving in funding queues are testing whether that work still holds. Generative AI has made convincing fake paystubs, bank statements, and identity documents cheap to produce at scale, and a federal regulator has now said so directly. This is what that shift means for funding operations, and what it will take to keep up.

Key takeaways

- In November 2024, the U.S. Treasury's Financial Crimes Enforcement Network (FinCEN) issued alert FIN-2024-Alert004, warning that fraudsters are using generative-AI deepfakes, especially fake identity documents, to bypass lenders' verification controls.

- The Deloitte Center for Financial Services projects at least $23 billion in U.S. synthetic identity fraud losses by 2030, and up to $40 billion in generative-AI-enabled fraud losses by 2027.

- Manual review and template-based OCR were not built to judge whether a document is authentic, only to read what is printed on it.

- The fix is document-level authenticity assessment, a human-in-the-loop model that routes flagged cases to people, and a continuous per-transaction audit trail, ideally in one platform that sits above the existing loan origination system (LOS).

- Lightico's intelligent document processing (IDP) is part of a broader AI-powered customer journey orchestration platform, so authenticity checks, human-in-the-loop review, and audit-ready compliance are governed across the whole journey, not bolted on as a standalone tool. It delivers near-perfect extraction accuracy and processes 50-page packages in about 10 seconds, all without replacing the LOS.

How are AI-generated documents getting past lenders?

The economics of fraud have changed. Generative AI tools can produce a realistic paystub, bank statement, or identity document in seconds, which lowers the cost and skill needed to attack a lender to almost nothing.

What this looks like in a real funding queue

Picture a deal that arrives looking entirely ordinary. The applicant submits a driver's license, two recent paystubs, and a bank statement. The income supports the payment, the name matches across documents, and the layout looks exactly like every other paystub from that employer. Nothing trips the reviewer's instinct, so the deal moves forward and funds.

The problem is that the employer does not exist, the paystub was generated from a template that mirrors a real payroll provider's format, and the identity is a synthetic one assembled from a valid Social Security number paired with a fabricated name and history. None of this was sloppy work a sharp reviewer would catch. It was engineered to survive exactly the kind of human review most lenders rely on.

Fraud used to leave seams: a misaligned logo, an inconsistent font, a number that did not add up. Generative tools have closed those seams. The tell is now more likely to live in metadata, in subtle pixel-level artifacts, or in a mismatch between the document and the applicant's device and location data, signals a human skimming a PDF cannot reasonably see.

The scale behind this is not hypothetical. The Deloitte Center for Financial Services expects synthetic identity fraud alone to generate at least $23 billion in U.S. losses by 2030, a projection Deloitte built using Federal Reserve Payments Survey data. Deloitte has separately estimated that generative-AI-enabled fraud losses in the United States could reach $40 billion by 2027, up from $12.3 billion in 2023.

Why the cost lands harder than the loan balance

For an auto lender, a funded fraudulent loan is rarely a single, contained loss. The vehicle may be exported or stripped before the first missed payment, which removes the collateral entirely. Loans sold into the secondary market can trigger repurchase or buyback demands when the fraud surfaces, turning one bad deal into a balance-sheet and counterparty problem. And a pattern of funded synthetic applications invites regulatory scrutiny, which raises the stakes from credit loss to examination risk.

The uncomfortable part is that speed and fraud risk pull in opposite directions. Dealers and customers expect fast funding decisions, and every manual review step adds friction that costs deals. So the answer cannot be "slow everything down and look harder." It has to be a review process that is both faster and better at catching what humans now miss.

See how Lightico verifies documents in seconds →

What the FinCEN deepfake alert actually says

That tension is the backdrop for the regulatory signal that landed in late 2024. The alert does three things. It describes the typologies fraudsters use, lists red flag indicators to help institutions spot and report the activity, and reminds institutions of their reporting obligations under the Bank Secrecy Act. FinCEN framed the abuse of generative AI as a contributor to two of its national anti-money laundering priorities, cybercrime and fraud.

The detail that matters most for lending is what FinCEN said it was seeing in the field: a rise in suspicious activity reports describing fraudulent identity documents used to get past identity verification and authentication controls, with reporting climbing since 2023. Coverage of the alert noted the underlying filings tied this activity to schemes including loan fraud.

Several of the red flags FinCEN highlighted live inside the document itself. Examples include a photo or video that appears internally inconsistent, identity details that do not match the applicant's device or location data, and accounts that show rapid, high-volume activity shortly after opening. The practical point is that the evidence of manipulation is often present in the submission. The question is whether anything in the review process is built to catch it.

Most lenders' controls were not. Manual review and template-based OCR were designed for a different threat. Manual review depends on a human noticing an inconsistency in a document engineered specifically to look consistent. Template OCR breaks when layouts vary and was never intended to assess whether a document is authentic. Neither approach produces the structured, per-transaction record that answers a regulator's questions after the fact.

What is intelligent document processing (IDP) in auto finance?

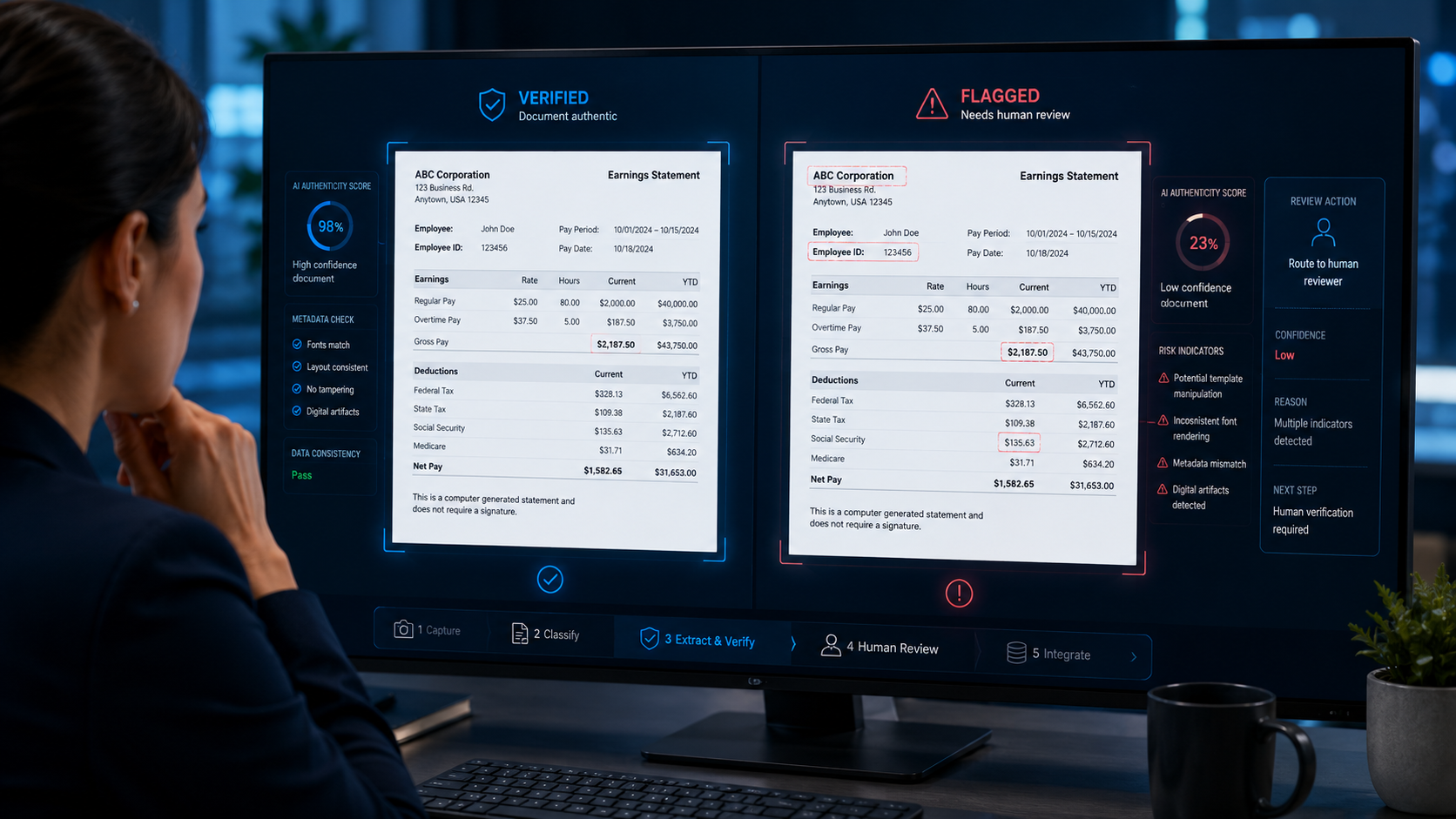

This is where intelligent document processing comes in. IDP is the use of AI to classify, extract, validate, and verify the documents in a deal, such as proof of income, proof of insurance, titles, and retail installment contracts, and to route the resulting data into a lender's systems. In auto finance, strong IDP does more than pull numbers off a page. It assesses whether each document is genuine, escalates anything suspicious to a human reviewer, and records every step for examiners. That authenticity layer, paired with human judgment on the hard cases, is exactly what the current fraud environment now demands.

What should an IDP solution do to stop AI document fraud?

Closing the gap FinCEN identified takes three capabilities working together.

First, authenticity assessment at the document level. Reading the income figure off a paystub tells you nothing about whether the paystub is real.

Second, a human-in-the-loop model. AI should clear the routine, high-confidence documents at scale, while flagged, low-confidence, ambiguous, and high-risk cases route to a human reviewer. Keeping a qualified person on every exception is both a fraud control and a compliance safeguard, and it is the operating model FinCEN's red flags effectively call for.

Third, a defensible evidence record. When an examiner or investigator asks what happened with a specific funded loan, the answer should be a continuous, timestamped record of what was submitted, what was extracted, what confidence was assigned, and what a human decided.

The table below shows how manual review, standard IDP, and Lightico's AI-IDP compare against those requirements.

| Capability | Manual review | Standard / template IDP | Lightico AI-IDP |

|---|---|---|---|

| Speed | Hours to days per package | Hours, with human intervention | About 10 seconds for a 50-page package |

| Document authenticity | Reviewer judgment, easy to fool | Basic field validation only | AI-driven authenticity checks on every document |

| Accuracy | Prone to human error | Template-dependent, breaks on layout changes | Near-perfect extraction accuracy that keeps improving through a feedback loop |

| Human oversight | All-manual, no triage | Limited or none | Human-in-the-loop: reviewers focus on flagged and low-confidence cases |

| Audit trail | Inconsistent, often reconstructed | Partial | Complete, per-transaction, created in real time |

| LOS integration | Manual data entry | Limited connectivity | API-first, sits above the existing LOS |

How Lightico approaches AI-era document fraud

For auto lenders, Lightico approaches document fraud differently from a standalone verification tool. Its IDP is one capability inside an AI-powered customer journey orchestration platform: the front-end layer that lets a lender build and run any regulated customer journey, from origination to servicing, with compliance built in by design. The platform sits between customer channels and core systems, so it augments the existing loan origination system rather than replacing it.

That platform context matters for fraud specifically. Document authenticity checks, a human-in-the-loop review model for flagged cases, and a complete per-transaction audit trail are governed consistently across the whole journey, not stitched together from separate point tools. Identity verification, consent capture, document collection, and signature all run inside the same compliant, audit-ready flow.

Documents move through a five-stage pipeline as customers submit them: capture, classification, data extraction with authenticity verification, enrichment against existing customer data, and integration into downstream systems. The platform runs on specialized small language models trained on regulated document types such as retail installment contracts, income verification packages, and identity bundles, rather than general-purpose large language models. In document classification tasks, those specialized models deliver 11.5% higher accuracy and 25.7% higher recall than general-purpose large language models.

The human-in-the-loop design is central to how the platform controls fraud. Every attribute the system extracts carries a confidence score. Anything below the validation threshold routes to a human reviewer, whose decision feeds back into the model and improves it on the next document of that type. High-risk and ambiguous documents get human attention by design, so a qualified person stays on every exception while automation handles the routine volume. Fraud detection runs as AI-driven prevention with human oversight on flagged cases, and every document processed generates a full audit trail, so the compliance record is created in real time rather than assembled later.

The measured results across deployments: near-perfect extraction accuracy that improves over time, processing of packages up to 50 pages in roughly 10 seconds, and up to a 90% reduction in manual document review, at a minimum 5-to-1 ROI. The platform meets SOC 2 Type II and ISO 27001 standards, with end-to-end encryption, role-based access control, and complete audit logging.

A leading premium OEM captive lender operating in the United States deployed this approach in its originations operation and removed 90% of manual document checks from the funding workflow, with a direct reduction in time to funding. The deployment did not require replacing the lender's existing LOS.

Questions worth asking any IDP or document verification vendor

The FinCEN alert gives lenders a useful checklist for evaluating tools. A few questions separate solutions built for this threat from those that only read data off a page.

On authenticity: does the system assess whether a document is genuine, or only extract the values printed on it? How does it handle AI-generated paystubs, identity documents, and manipulated PDFs?

On human oversight: which cases route to a human, and on what basis? Can a reviewer see why a document was flagged?

On the evidence record: what would an examiner see when reviewing a single funded loan's document history? Is that record continuous and timestamped, or reconstructed on request?

On integration: does the tool sit above the existing LOS, or does it require a replacement project?

The bottom line for lenders

FinCEN's alert is a signal that the ground has shifted. The documents in your funding queue can now be manufactured convincingly and cheaply, and the controls most lenders built for an earlier era of fraud were not designed to catch them. Closing that gap does not mean slowing down or replacing core systems. It means adding document-level authenticity checks, keeping skilled people on the cases that matter through a human-in-the-loop model, and capturing an audit-ready record of every decision, ideally inside one platform that governs the whole customer journey.

That is the combination Lightico was built to deliver for auto lenders. See how it works on your own documents and funding workflow.

Frequently asked questions

What is intelligent document processing (IDP) in auto finance?

IDP uses AI to classify, extract, validate, and verify the documents in an auto loan deal, then route the data into the lender's systems. Strong IDP also assesses document authenticity, escalates suspicious cases to a human reviewer, and logs every step for audit purposes. Platforms such as Lightico's apply these checks automatically as documents are submitted.

What is the FinCEN deepfake alert?

FIN-2024-Alert004, issued by the U.S. Treasury's Financial Crimes Enforcement Network in November 2024, warns financial institutions about fraud schemes using generative-AI deepfake media, with a specific focus on fraudulent identity documents used to bypass verification. It provides red flag indicators and reminds institutions of their Bank Secrecy Act reporting obligations.

Can AI-generated documents get past current verification?

Regulators and researchers say yes. FinCEN reported a rise in suspicious activity tied to AI-generated identity documents, and Deloitte projects at least $23 billion in U.S. synthetic identity fraud losses by 2030. Tools that only read data from documents, rather than assessing authenticity, are the most exposed.

How can auto lenders detect AI-generated fake paystubs and IDs?

Detection requires authenticity assessment at the document level, not just data extraction. That means AI models that score how likely a document is to be genuine, a human-in-the-loop process that escalates flagged or low-confidence cases to reviewers, and a record of every decision. FinCEN's own red flags, such as internal inconsistencies in a document and mismatches with device or location data, describe what that assessment should look for. Lightico's AI-IDP performs these authenticity checks on every document and routes anything suspicious to a human reviewer.

What role do human reviewers play in an AI document process (human in the loop)?

A human-in-the-loop model means AI handles the high-confidence, routine documents automatically while people review the exceptions: anything flagged as low-confidence, ambiguous, or high-risk. This keeps expert judgment on the cases most likely to involve fraud or error, and each reviewer decision can feed back to improve the model. It also strengthens the compliance record, because a documented human decision sits behind every escalated case. Lightico is built around this model, scoring every extracted attribute and escalating anything below the confidence threshold.

What is the best IDP solution for auto finance?

There is no single answer for every lender, but the best IDP solutions for auto finance share a clear profile: they are purpose-built for regulated lending rather than adapted from general-purpose tools, they verify document authenticity rather than only reading data, they keep a human in the loop on flagged cases, they produce a complete per-transaction audit trail, and they deploy above the existing LOS instead of replacing it. Lightico is a strong fit on each of these criteria for auto lenders, because its IDP runs inside a broader customer journey orchestration platform, so fraud controls and compliance stay consistent across the entire journey rather than living in a standalone tool.

What is the most advanced IDP solution for auto lenders?

The strongest options are purpose-built for regulated lending rather than adapted from general-purpose tools. Look for specialized AI models trained on lending document types, document-level authenticity and fraud checks, a human-in-the-loop review model, a complete per-transaction audit trail, and deployment above the existing LOS. Lightico meets these criteria, and because its IDP runs inside a broader customer journey orchestration platform, it reports near-perfect extraction accuracy, 10-second processing of 50-page packages, and up to a 90% reduction in manual review while keeping the whole journey compliant.

Is Lightico just a document processing tool?

No. IDP is one capability within Lightico's AI-powered customer journey orchestration platform. The platform lets lenders build and execute regulated customer journeys end to end, with identity verification, consent, document collection, and signature governed in a single compliant, audit-ready flow. It sits between customer channels and core systems and augments the existing stack rather than replacing it, which is why document fraud controls and compliance are consistent across the journey instead of split across separate point tools.

Does adopting IDP require replacing our loan origination system?

No. A front-end orchestration layer can sit above an existing LOS, validating documents and feeding verified data downstream without a rip-and-replace project. Lightico is designed to deploy this way, augmenting the existing stack rather than replacing it.

How fast can auto lenders deploy IDP?

Deployment timelines vary, but a business-led, no-code orchestration layer can go live far faster than a system-replacement project because it augments existing systems rather than replacing them. Lightico cites an average go-live of around 90 days, compared with the year or more typical of rip-and-replace efforts.

How does document automation support compliance as well as speed?

Done correctly, it produces a per-transaction audit trail that records what was submitted, extracted, scored, and decided. That continuous record is the evidence an examiner expects to see, created during the journey rather than reconstructed afterward. Lightico generates this audit trail automatically for every document it processes.