COVID-19 Consumer Study Shows Banks are Still Fumbling Digital Onboarding

By Leor Melamedov

The coronavirus and widespread fear of infection made it imperative for banks to fully digitize many banking transitions — and new customer onboarding was no exception.

With this in mind, we conducted a survey of 1,007 American banking customers to determine the strength of their banks’ onboarding processes. We found that of the customers who tried to open a new bank account between February and June 2020, a large minority faced difficulties during the process.

This suggests that while banks overall rose to the occasion to promote digital services during this period, those digital services aren’t as smooth as they could be.

The state of digital onboarding in the wake of COVID-19

Banks are spending record amounts on marketing. In 2018, banks cumulatively increased their marketing spend by 13% to $13.0 billion, with JP Morgan Chase, Capital One, Bank of America, and Citibank each spending over $1.0 billion on marketing.

They have good reason to fight for every customer’s attention. The rewards for every new customer are great, with the lifetime average value of a banking customer now standing at $45,600 (for the average customer lifespan of eight years).

Yet attracting customers’ attention is only half the battle. The other half is actually getting them to convert once they show intent.

At the height of the Great Lockdown, it was ultra-important for banks to offer customers digital onboarding. Fears of catching the pathogen in packed in-person banks led customers from a wide variety of demographic groups to prefer digital onboarding. Even groups that would have previously shied away from signing up to a bank online, such as older Americans, are now far more open to digital banking.

Banks made sure to promote their digital onboarding offerings during the coronavirus, but simply offering digital onboarding isn’t enough. It’s crucial that customers that try to open an account from their mobile phones or computer are able to complete the process effortlessly.

Failure to offer smooth onboarding comes at a heavy price. According to Forrester, over 64% of banks report lost revenue due to problems in their onboarding processes. The good news is, these issues are relatively easy to fix once they’re identified.

Digital onboarding across banks was inconsistent during the coronavirus

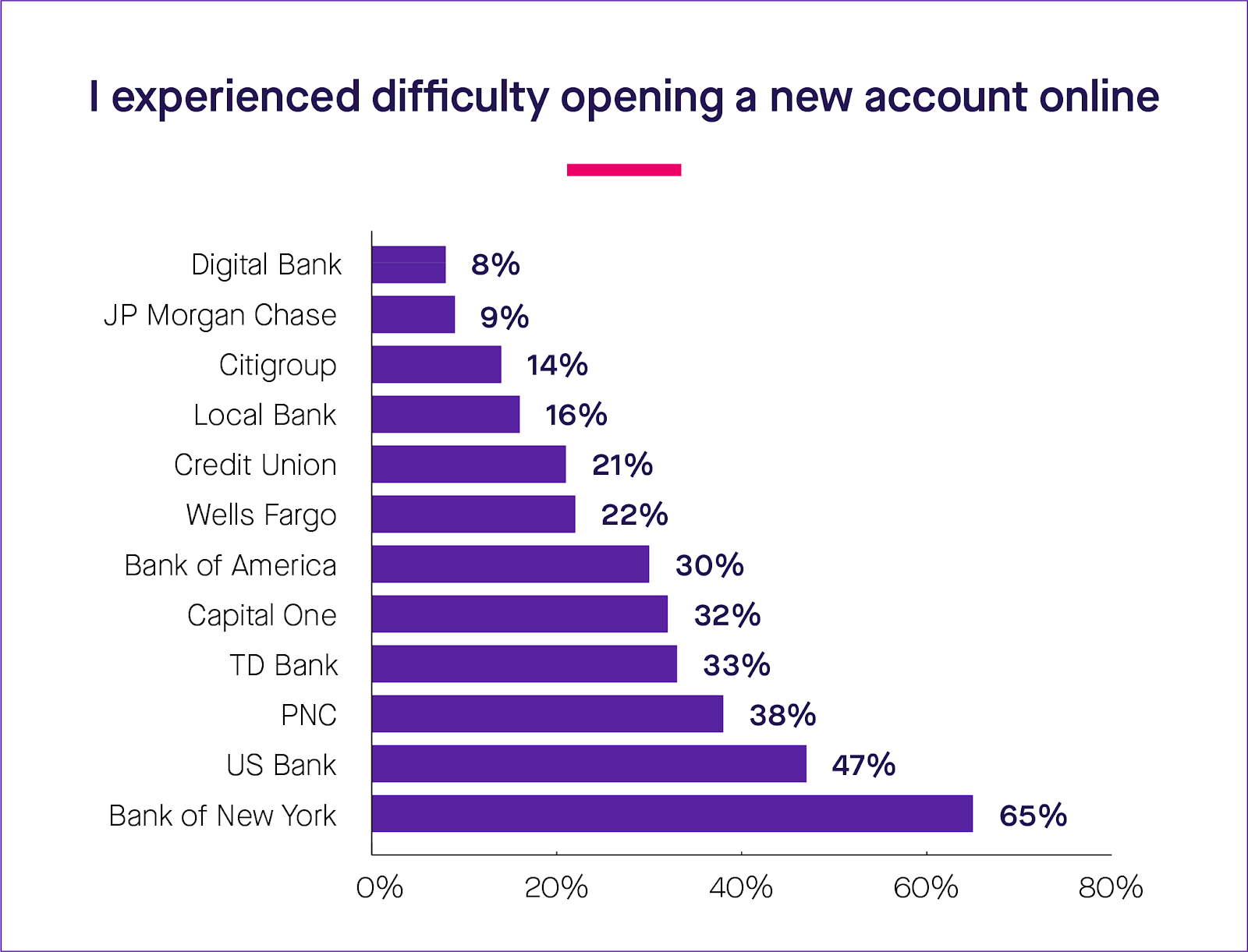

According to the Lightico survey, 18% of customers tried to open a new bank account between February and June 2020. That’s a significant proportion of customers who were making a big move during the lockdown and needed to do so remotely and efficiently.

The survey results reveal large variability in the smoothness of the onboarding journey across banks.

Unsurprisingly, customers at digital-only banks showed the greatest satisfaction in their online account opening experience. A mere 8% of this group reported difficulty opening a new account online.

Yet JP Morgan Chase, Citibank, and local bank customers also reported relatively low levels of onboarding frustration, and high satisfaction with their account opening process. In stark contrast, 47% and 65% of customers of the worst-ranking banks for digital onboarding, reported digital onboarding difficulties. The average ratio of customers who reported difficulty across all banks and bank types was 27%.

This variability shows that while digital-only banks certainly have the upper hand when it comes to creating an effortless account opening experience, their advantage is hardly set in stone. Traditional banks that replace legacy systems and commit to streamlining the digital onboarding process can easily catch up to digital-only banks’ success. In fact, a few of them already are.

What went wrong during the onboarding process?

Most major banks allow customers to open an account online, a capability that was heavily promoted during the coronavirus era. But once customers begin that process, the purported digitality of the transaction is often compromised.

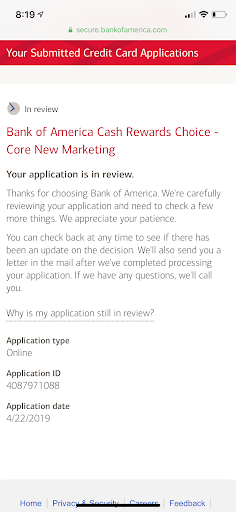

For example, Bank of America customers are able to complete the entire account application process online. However, they are required to remember to regularly return to the bank’s website to check on their application status — or await a letter in the mail. Below is a screenshot from an actual interaction:

Imagine if this were a digital-only or digital-first bank: The customer would receive a text message or email updating them as soon as their application was approved or rejected.

Banks that eliminate paperwork or snail mail, and remove other annoying obstacles such as bouncing between channels, can find themselves well-positioned to compete even with digital-only banks on this front.

Conclusion: Online onboarding still has room for improvement

Offering online bank account opening is a must, both in light of coronavirus-related safety concerns about in-branch banking, and customers’ surging interest in convenient bank transactions. Yet many banks need to ensure their digital onboarding process is so smooth, customers won’t even think about dropping out of the process due to preventable operational glitches and legacy systems.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

According to the Lightico survey, 18% of customers tried to open a new bank account between February and June 2020. That’s a significant proportion of customers who were making a big move during the lockdown and needed to do so remotely and efficiently.

The survey results reveal large variability in the smoothness of the onboarding journey across banks.

Unsurprisingly, customers at digital-only banks showed the greatest satisfaction in their online account opening experience. A mere 8% of this group reported difficulty opening a new account online.

Yet JP Morgan Chase, Citibank, and local bank customers also reported relatively low levels of onboarding frustration, and high satisfaction with their account opening process. In stark contrast, 47% and 65% of customers of the worst-ranking banks for digital onboarding, reported digital onboarding difficulties. The average ratio of customers who reported difficulty across all banks and bank types was 27%.

This variability shows that while digital-only banks certainly have the upper hand when it comes to creating an effortless account opening experience, their advantage is hardly set in stone. Traditional banks that replace legacy systems and commit to streamlining the digital onboarding process can easily catch up to digital-only banks’ success. In fact, a few of them already are.

According to the Lightico survey, 18% of customers tried to open a new bank account between February and June 2020. That’s a significant proportion of customers who were making a big move during the lockdown and needed to do so remotely and efficiently.

The survey results reveal large variability in the smoothness of the onboarding journey across banks.

Unsurprisingly, customers at digital-only banks showed the greatest satisfaction in their online account opening experience. A mere 8% of this group reported difficulty opening a new account online.

Yet JP Morgan Chase, Citibank, and local bank customers also reported relatively low levels of onboarding frustration, and high satisfaction with their account opening process. In stark contrast, 47% and 65% of customers of the worst-ranking banks for digital onboarding, reported digital onboarding difficulties. The average ratio of customers who reported difficulty across all banks and bank types was 27%.

This variability shows that while digital-only banks certainly have the upper hand when it comes to creating an effortless account opening experience, their advantage is hardly set in stone. Traditional banks that replace legacy systems and commit to streamlining the digital onboarding process can easily catch up to digital-only banks’ success. In fact, a few of them already are.

Imagine if this were a digital-only or digital-first bank: The customer would receive a text message or email updating them as soon as their application was approved or rejected.

Banks that eliminate paperwork or snail mail, and remove other annoying obstacles such as bouncing between channels, can find themselves well-positioned to compete even with digital-only banks on this front.

Imagine if this were a digital-only or digital-first bank: The customer would receive a text message or email updating them as soon as their application was approved or rejected.

Banks that eliminate paperwork or snail mail, and remove other annoying obstacles such as bouncing between channels, can find themselves well-positioned to compete even with digital-only banks on this front.