Even As Lockdowns Are Lifted, Consumers Want Remote Banking More Than Ever

By Leor Melamedov

Slowly but surely, lockdowns and mandated social distancing policies are being lifted around the US. As a result, many banks are gearing up for a return to pre-pandemic banking habits, such as an abundance of full-service bank branches and physical paperwork.

However, a Lightico survey of 1,024 Americans in mid-September 2020 found that consumers were even more eager to try new digital tools and open financial accounts online than they were in our May survey. Consumer resistance to in-branch banking is independent of fluctuations in official mandates. In other words, the belief that “If you open it, they will come,” couldn’t be further from the truth.

Mandatory Branch Visit? Consumers Would Rather Stay Home.

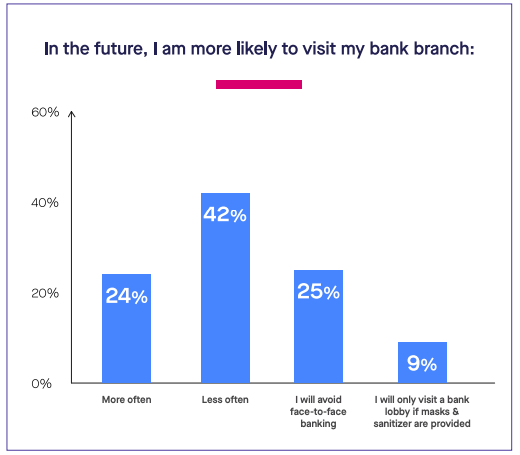

Branch banking continues to be impacted by consumers’ reluctance to leave the house. 76% of consumers plan to avoid or reduce visiting a bank branch in the future (to break it down, 42% will go less often, and 25% will avoid face-to-face banking altogether). Interestingly, safety measures seem to make little difference, with only 9% of consumers saying they will visit the branch if masks and hand sanitizers are available.

Unfortunately, it gets worse. Not only do consumers prefer to bypass the branch visit––47% of consumers would be less likely to attend to a non-loan banking or financial task if it forced them to visit a branch.

Furthermore, 33% of consumers would not take a loan if it required a branch visit. This should come as a shock given the desperation we see among consumers for new lines of credit, and the importance of lending in the banking industry. Yet, if we do not make lending seamless and if we require our customers to come into our branch, we will lose these opportunities.

Interest in Digital Banking Even Higher Today Than in May

As of September 2020, more states were loosening coronavirus-related restrictions than tightening them. The coronavirus is no longer the mystery it was at the beginning of the outbreak, and we understand more about how to take precautions. And while a vaccine is still not available, we are likely closer to having one than we were months ago.

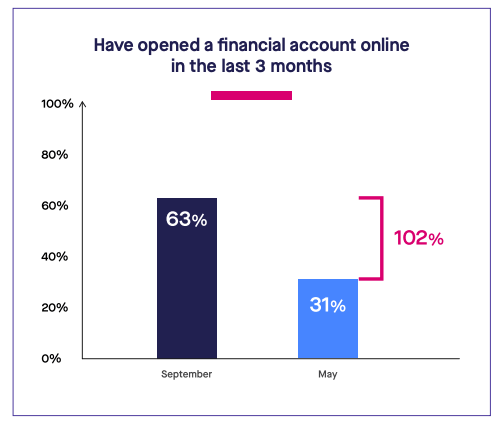

Despite all this, consumers are significantly more likely to prefer digital, remote transactions now than they were when the outbreak was still fresh. 91% of consumers are willing to try a new digital app or website––an increase from 63% in May. And of customers who opened a financial account in the last three months, 63% of them completed the process online (compared to just 31% who did so in May).

We can surmise that two things are at play here: First, banks have gotten better at serving customers digitally throughout the pandemic; there are more opportunities now for financial institutions to serve their customers digitally.

Second, consumers have had more time to get comfortable with digital interactions throughout the pandemic. This may be especially true of nontypical digital users, such as senior citizens, who started to rely on digital channels to safeguard their health during the past half-year. Online and mobile banking no longer seem so intimidating; many now come to see digital channels as an essential convenience.

But Banks Are Still Not Delivering Sufficiently Digital Journeys

To be sure, most banks have significantly improved and expanded their digital offerings during the pandemic. As we’ve seen, this partly explains the increased consumer usage of online banking. At the same time, banks still have room for improvement if they want to cater to consumers’ growing digital demands.

Our survey found that more than half of consumers have recently experienced being bounced to physical channels during a purportedly all-digital interaction. 57% of consumers were directed to a branch during an online interaction between July and September, and a similar percentage were asked to print, scan, or fax during an online interaction.

In many ways, these broken digital journeys are even more disruptive to the customer experience because they set customer expectations for digital high––only to disappoint them at the last minute (usually to sign KYC paperwork at a branch). Such broken journeys are also directly harmful to the bank’s bottom line: banks need to invest in both ample digital and branch infrastructure, with no clear delineation between what services are online, and which are branch-based.

The Takeaway

Banks that want to serve customers well both during the pandemic and after need to ensure all interactions that begin online, stay online. Consumers’ expectations for streamlined journeys have increased exponentially over the past several months, and banks will need to make continuous additions and modifications to their online offerings to meet unprecedented demand.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Unfortunately, it gets worse. Not only do consumers prefer to bypass the branch visit––47% of consumers would be less likely to attend to a non-loan banking or financial task if it forced them to visit a branch.

Furthermore, 33% of consumers would not take a loan if it required a branch visit. This should come as a shock given the desperation we see among consumers for new lines of credit, and the importance of lending in the banking industry. Yet, if we do not make lending seamless and if we require our customers to come into our branch, we will lose these opportunities.

Unfortunately, it gets worse. Not only do consumers prefer to bypass the branch visit––47% of consumers would be less likely to attend to a non-loan banking or financial task if it forced them to visit a branch.

Furthermore, 33% of consumers would not take a loan if it required a branch visit. This should come as a shock given the desperation we see among consumers for new lines of credit, and the importance of lending in the banking industry. Yet, if we do not make lending seamless and if we require our customers to come into our branch, we will lose these opportunities.

We can surmise that two things are at play here: First, banks have gotten better at serving customers digitally throughout the pandemic; there are more opportunities now for financial institutions to serve their customers digitally.

Second, consumers have had more time to get comfortable with digital interactions throughout the pandemic. This may be especially true of nontypical digital users, such as senior citizens, who started to rely on digital channels to safeguard their health during the past half-year. Online and mobile banking no longer seem so intimidating; many now come to see digital channels as an essential convenience.

We can surmise that two things are at play here: First, banks have gotten better at serving customers digitally throughout the pandemic; there are more opportunities now for financial institutions to serve their customers digitally.

Second, consumers have had more time to get comfortable with digital interactions throughout the pandemic. This may be especially true of nontypical digital users, such as senior citizens, who started to rely on digital channels to safeguard their health during the past half-year. Online and mobile banking no longer seem so intimidating; many now come to see digital channels as an essential convenience.