How Credit Unions Can Deliver a Better Member Experience From Their Legacy Banking Core

By Leor Melamedov

Credit unions are typically loath to change their core processing systems. Doing so requires a huge investment of time and money, as well as support from stakeholders on the business, IT, and back-office side. The good news is that credit unions don’t need to change their core in order to upgrade the member experience. All they need are the right technological tools that can be synced with the core via open APIs, and provide immediate ROI.

Here, we’ll explain why it’s so important for credit unions to harness digitization to improve their member experience, and the top capabilities that will help them do so.

A Digital Member Experience Is A Positive Member Experience

With coronavirus cases skyrocketing across the U.S., credit union members are eager for digital and remote banking options. In today’s world, credit unions that want to improve the member experience (and let’s face it, what credit union doesn’t?) will want to look no further than banking technology.

A recent survey of over 1,000 Americans found that credit union members overwhelmingly prefer digital and remote banking — and many will simply skip banking activities that require in-person interaction. According to the survey, almost 50% of members would avoid taking a loan out if it required a physical visit to a credit union.

While fear of coronavirus transmission is certainly driving some of this eagerness for digital banking, it’s unlikely to be the only reason. The safety imperative has turned into a convenience imperative; digital banking is no longer seen as a stopgap but as the default way of doing things. Even demographic groups that weren’t normally associated with digital banking before the coronavirus struck, such as senior citizens, are now all-in.

The following survey results reveal just how integral remote banking is to the member experience:

55% of consumers say they plan to visit credit union branches less often in the future.

26% say they will avoid face-to-face banking altogether.

Just 10% say they would be more likely to visit a branch if it offered safety measures (like mandatory mask-wearing and hand sanitizer).

For credit unions that want to maximize their member experience, they need not look further than plugging in valuable, visible frontend technology to existing systems. An older core doesn’t have to hold them back. Digital tools can be plugged in to provide immediate member and associate value. During today’s remote reality, fast innovation is needed to keep up with rapidly changing member expectations. Associates who are armed with the right tools can focus on creating more meaningful and personal experiences, rather than scrambling to hold together bureaucratic pieces. Here are the capabilities need to do it.

5 Essential Member-Centric Technologies CUs Need Now

To meet the growing member demand for digital banking, credit unions need to ensure seamless journeys, whether at the physical branch or on digital channels. This can be accomplished by retaining the credit union’s existing core while adding digital tools that help and delight members.

But the member-centric platforms aren't composed of mere features. The best platforms enable admins to automate entire end-to-end processes with a simple drag-and-drop interface. Intuitive conditional rules can be set to ensure business logic between steps, within steps, and within form fields.

This ensures that at every stage, members are requested to take action based on their particular characteristics and needs. Credit union members are all unique, with unique circumstances; automated digital workflows should reflect that.

The following tools are integral parts of such workflows, and will have an immediate positive impact on the member experience without requiring coding or IT involvement. Admins can simply plug and play — and see results right away.

Capability 1: Mobile-First eSignatures

Allow members to sign contracts, forms, and agreements from their cell phones. Credit unions can use mobile eSignatures to send documents directly to the member’s cell phone via text message for immediate attention and easy completion. Unlike wet signatures and email eSignature solutions, text-message-centric mobile eSignature solutions do not require a physical branch, snail mail, email, or phone apps.

Mobile eSignatures can be deployed from any member touchpoint including website, chat, or IVR. They can even be used during a call with a credit union agent who can guide members through the signing process. Members either finger sign, type sign, or use auto-generated signatures which are validated and stored on the CRM with a full audit trail. Mobile-first eSignatures are proven to generate over 50% more completed signatures than legacy systems, the vast majority in the moment.

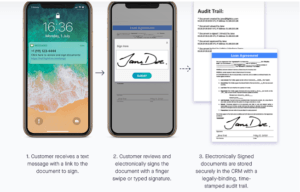

How Mobile-First eSignatures Work

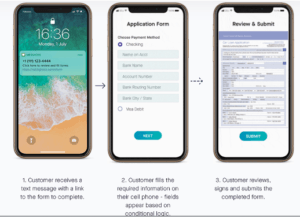

Capability 2: Smart eForms

Agents should not be burdened with chasing members to complete forms or fix error-filled fields. User-friendly eForms provide members with an intuitive interface so they can complete all the required information correctly the first time, eliminating rework and chasing.

Smart eForms simplify the paperwork that often slows processes and frustrates members and agents. With smart eForms, cumbersome paper forms and PDFs are converted into easily fillable mobile eForms. They leverage techniques like conditional logic, smart fields, auto-fill, and predictive typing to boost first-time completion rates to 95%, slashing NIGO forms.

eForms are sent directly to the member’s mobile device via a text message from which the member can effortlessly complete and submit any missing information in real-time. This information is then seamlessly synced with the credit unions’ CRM to ensure data hygiene.

How Smart eForms Work

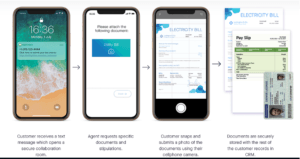

Capability 3: Mobile-First Document Collection

Collecting documents such as photo ID, proof of income, invoices, and utility bills are often a KYC requirement for credit union onboarding and servicing. However, current processes damage the member experience as members are required to scan, email, fax, and even visit the branch to submit these documents.

Credit unions can promote remote document collection by enabling members to use their cellphone cameras to easily snap and instantly submit pictures of these documents. Those collected documents are then associated with the member’s file and securely stored with the rest of their records in the CRM. Mobile-first document collection minimizes the back and forth between agents and members, speeding up cycle times by 80%. For today’s busy credit union members, this comes as a huge relief.

How Mobile-First Document Collection Works

Capability 4: Effortless ID Verification

Automatic ID verification allows credit unions to verify member identity completely remotely.

Credit unions can use digital ID verification tools to determine whether a member or nonmember’s ID is authentic by allowing users to submit their passport, driver’s license, or another government-issued photo directly from their cell phone — for quick and convenient ID verification. AI algorithms analyze the authenticity and validity of the photo ID to determine whether the document is genuine or fraudulent.

Agents can also confirm that the member they are speaking to is genuine by having the member send a selfie that is scanned and automatically compared to the photo ID.

In this way, credit unions can protect themselves and their members from fraud without slowing sales and service experiences.

How Effortless ID Verification Works

Capability 5: Digital Storage & Security

Credit unions can secure digital document storage to simplify adherence to NCUA regulations. By capturing all member interactions digitally, it is easier to audit and track those interactions. All documents can be digitally stored and stamped with seals to ensure safe and secure storage and quality control. With digitized contracts, supporting documents, and consent forms, credit unions can simplify audit and quality checks of their member interactions.

The Takeaway

By integrating agile and scalable customer-facing technologies into their existing core, credit unions can enhance their overall member experience. There is no need to revamp the entire backend system to enjoy an immediate and tangible ROI. All that’s needed are the right tools to boost the speed and quality of customer interactions.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Allow members to sign contracts, forms, and agreements from their cell phones. Credit unions can use mobile eSignatures to send documents directly to the member’s cell phone via text message for immediate attention and easy completion. Unlike wet signatures and email eSignature solutions, text-message-centric mobile eSignature solutions do not require a physical branch, snail mail, email, or phone apps.

Mobile eSignatures can be deployed from any member touchpoint including website, chat, or IVR. They can even be used during a call with a credit union agent who can guide members through the signing process. Members either finger sign, type sign, or use auto-generated signatures which are validated and stored on the CRM with a full audit trail. Mobile-first eSignatures are proven to generate over 50% more completed signatures than legacy systems, the vast majority in the moment.

Allow members to sign contracts, forms, and agreements from their cell phones. Credit unions can use mobile eSignatures to send documents directly to the member’s cell phone via text message for immediate attention and easy completion. Unlike wet signatures and email eSignature solutions, text-message-centric mobile eSignature solutions do not require a physical branch, snail mail, email, or phone apps.

Mobile eSignatures can be deployed from any member touchpoint including website, chat, or IVR. They can even be used during a call with a credit union agent who can guide members through the signing process. Members either finger sign, type sign, or use auto-generated signatures which are validated and stored on the CRM with a full audit trail. Mobile-first eSignatures are proven to generate over 50% more completed signatures than legacy systems, the vast majority in the moment.

Agents should not be burdened with chasing members to complete forms or fix error-filled fields. User-friendly eForms provide members with an intuitive interface so they can complete all the required information correctly the first time, eliminating rework and chasing.

Smart eForms simplify the paperwork that often slows processes and frustrates members and agents. With smart eForms, cumbersome paper forms and PDFs are converted into easily fillable mobile eForms. They leverage techniques like conditional logic, smart fields, auto-fill, and predictive typing to boost first-time completion rates to 95%, slashing NIGO forms.

eForms are sent directly to the member’s mobile device via a text message from which the member can effortlessly complete and submit any missing information in real-time. This information is then seamlessly synced with the credit unions’ CRM to ensure data hygiene.

Agents should not be burdened with chasing members to complete forms or fix error-filled fields. User-friendly eForms provide members with an intuitive interface so they can complete all the required information correctly the first time, eliminating rework and chasing.

Smart eForms simplify the paperwork that often slows processes and frustrates members and agents. With smart eForms, cumbersome paper forms and PDFs are converted into easily fillable mobile eForms. They leverage techniques like conditional logic, smart fields, auto-fill, and predictive typing to boost first-time completion rates to 95%, slashing NIGO forms.

eForms are sent directly to the member’s mobile device via a text message from which the member can effortlessly complete and submit any missing information in real-time. This information is then seamlessly synced with the credit unions’ CRM to ensure data hygiene.

Collecting documents such as photo ID, proof of income, invoices, and utility bills are often a KYC requirement for credit union onboarding and servicing. However, current processes damage the member experience as members are required to scan, email, fax, and even visit the branch to submit these documents.

Credit unions can promote remote document collection by enabling members to use their cellphone cameras to easily snap and instantly submit pictures of these documents. Those collected documents are then associated with the member’s file and securely stored with the rest of their records in the CRM. Mobile-first document collection minimizes the back and forth between agents and members, speeding up cycle times by 80%. For today’s busy credit union members, this comes as a huge relief.

Collecting documents such as photo ID, proof of income, invoices, and utility bills are often a KYC requirement for credit union onboarding and servicing. However, current processes damage the member experience as members are required to scan, email, fax, and even visit the branch to submit these documents.

Credit unions can promote remote document collection by enabling members to use their cellphone cameras to easily snap and instantly submit pictures of these documents. Those collected documents are then associated with the member’s file and securely stored with the rest of their records in the CRM. Mobile-first document collection minimizes the back and forth between agents and members, speeding up cycle times by 80%. For today’s busy credit union members, this comes as a huge relief.

Credit unions can secure digital document storage to simplify adherence to NCUA regulations. By capturing all member interactions digitally, it is easier to audit and track those interactions. All documents can be digitally stored and stamped with seals to ensure safe and secure storage and quality control. With digitized contracts, supporting documents, and consent forms, credit unions can simplify audit and quality checks of their member interactions.

Credit unions can secure digital document storage to simplify adherence to NCUA regulations. By capturing all member interactions digitally, it is easier to audit and track those interactions. All documents can be digitally stored and stamped with seals to ensure safe and secure storage and quality control. With digitized contracts, supporting documents, and consent forms, credit unions can simplify audit and quality checks of their member interactions.