Insurance Claims in a Covid-19 World: The Mandate & Technology to Streamline Claims.

By Leor Melamedov

Insurance companies are busier than ever, as call centers field inquiries surrounding policy expansion, coverage, and of course, claims. And as we emerge from the lockdown, experts predict that there will be a surge in insurance claims related to policy incidents and property issues. Determining coverage and eligibility is a sensitive issue right now, and taking up insurance providers’ time.

Requiring customers to file claims and send documents via snail mail, or get access to printers, scanners, and fax machines means imposing slow and inefficient processes on policyholders contending with issues of high urgency. In addition, these cumbersome transactions often require breaking social distancing –– which is a last resort for many customers who are still concerned about virus transmission.

We must do better at serving customers in the context of today’s remote reality. Enabling customers to file claims in a streamlined, mobile-friendly way can boost efficiency, prevent not-in-good-order (NIGO) documents, and improve claim turnaround time — at a time when customers need this most.

Claim Processes Are Critical to Insurers’ Profitability

Once an insurance company wins a new customer, retention and minimizing unnecessary expenses, while delivering a strong, and consumer-friendly claim process is key. For that reason, each claims process must be seamlessly and efficiently handled.

It’s true –– insurers are judged in their policyholders’ time of need.

On average, policyholders only make a claim every seven years, yet customers pay regularly to maintain their policies. Moreover, given customers don’t normally leave their insurance provider unless they have a negative experience during the claims process. But once they leave, the provider misses out on years of regular payments. It is imperative for insurance companies to make sure claims are dealt with efficiently and customer satisfaction/NPS is maintained. The best way of doing that is to make sure customers are fully satisfied with their claims experience.

Financially, there is even more importance to handling claims quickly and seamlessly. For example, if the claim lags, the insurer incurs additional internal handling costs of claims bureaucracy, such as filing, calls from the customer, compliance risks, not to mention endless overhead of transferring the claim between all parties. Furthermore, until the payout is made the insurance, they often incur other expenses like additional living expenses (ALE), which can certainly add up.

Consumers Demand Full, Fast Digital Claims

Currently, the insurance industry norm involves bouncing policyholders from channel to channel, and touchpoint to touchpoint as they try to get their claim approved. In between interactions, customers are left waiting and wondering what the next step in the process will be.

Time is of the essence for claimants, but insurance companies often don’t respond to their customers’ queries and requests in a way that reflects the urgency of their issue.

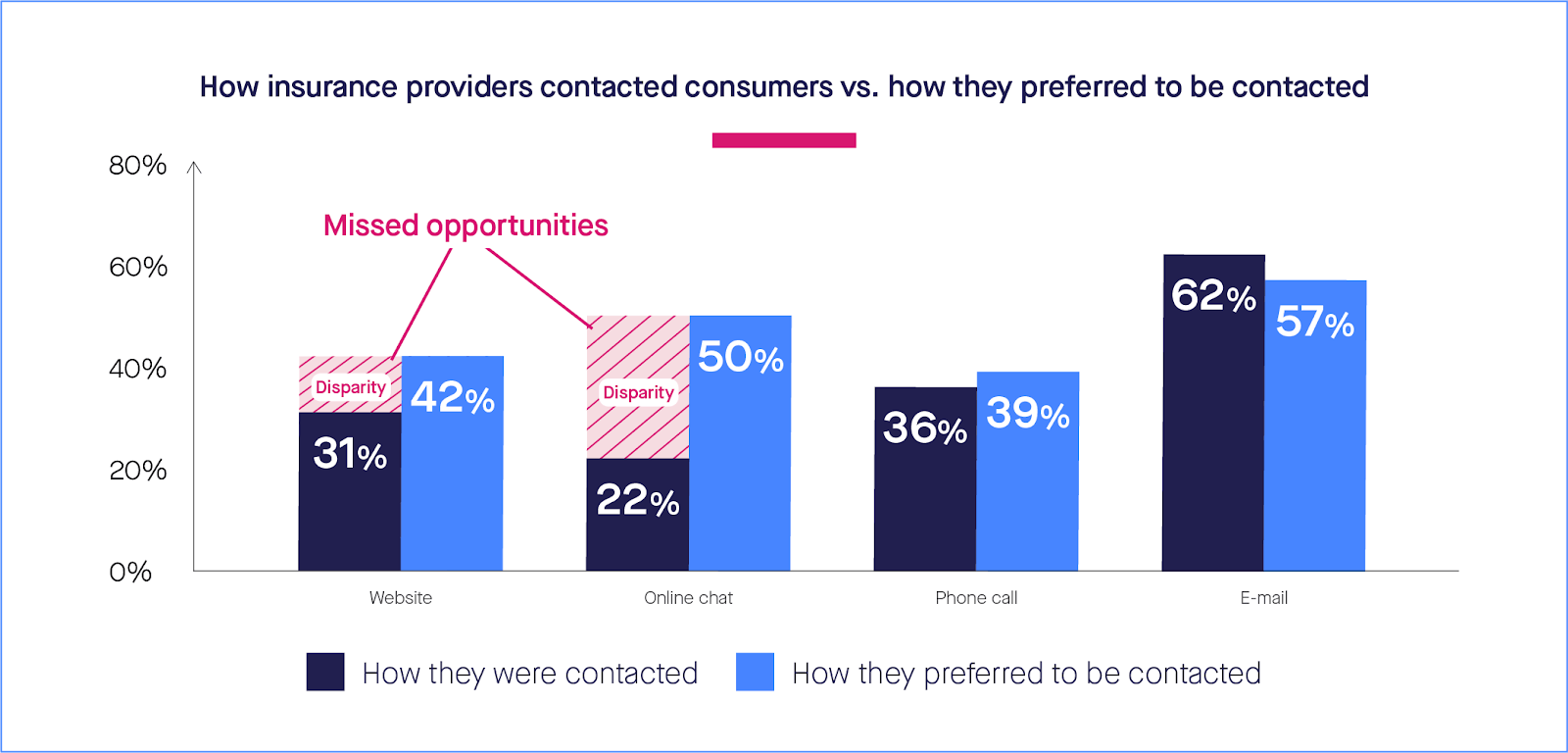

A recent Lightico survey found that during the coronavirus, U.S. consumers struggled to communicate with their insurance providers. Only 34% of policyholders said they were able to easily communicate with their insurance companies to ask questions or make modifications.

We also uncovered a significant gap between the channels insurance companies use to communicate with their customers, and the channels customers wish they would use. Many policyholders expressed the desire to communicate with their insurers online but weren’t offered the option. For example, 50% of policyholders said they wanted to communicate through online chat, but a mere 22% had access to this communication channel.

These communication issues show up again when customers try to file and complete a claim in a digital, efficient, and customer-centric way — and face obstacles to do so.

While many large insurance companies offer at least partially digital claims filing options, they still often involve bouncing customers between channels (e.g., phone, fax, scanning, email), adding needless friction, prolonging turnaround times, and ultimately hurting providers’ bottom line.

Insurers Can Easily Create A Best-In-Class Digital Claims Process

It’s time for a true digital transformation to make all of this needless difficulty history, once and for all. Digital transformation has been spoken about in the insurance industry for a while now, but now it’s imperative to act quickly to bring about the changes customers desperately need.

Insurance companies that make the switch to completely digital claims journeys will see a fast ROI. SaaS services bring the best of customer-facing technology to the forefront, allowing agents to easily manage claims remotely.

Specifically, adopting real-time mobile-optimized customer interactions enables insurance companies to collect and process all claims-related evidence and documentation instantly and from any location.

Streamlining the entire end-to-end claims process — from FNOL to processing and payment — has never been so easy to implement.

Here are some of the core capabilities insurance providers can easily integrate to leverage best-in-class digital claims processes on top of their current systems:

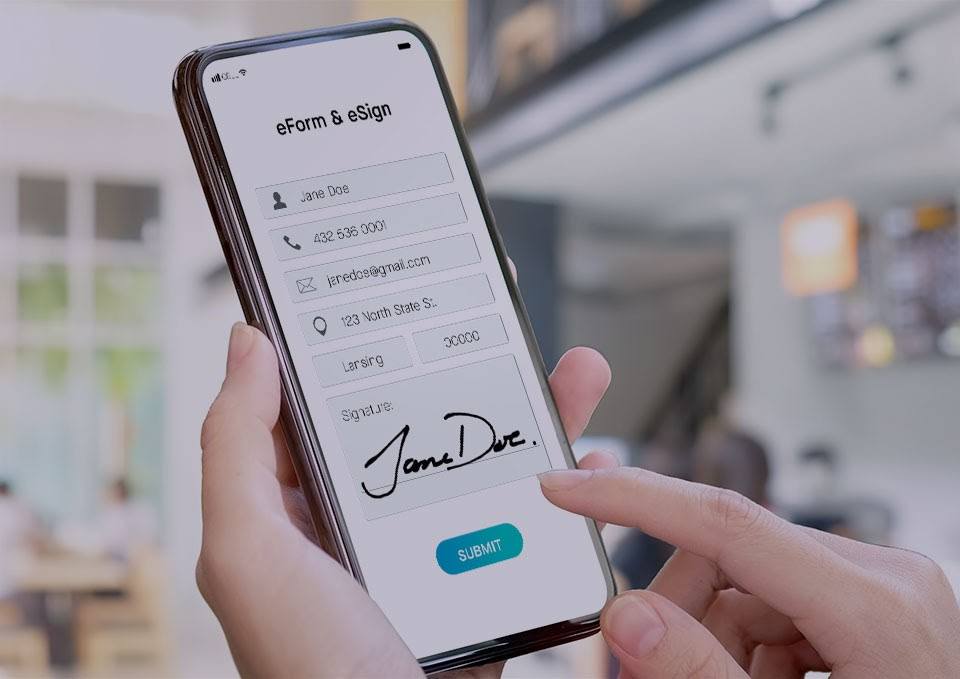

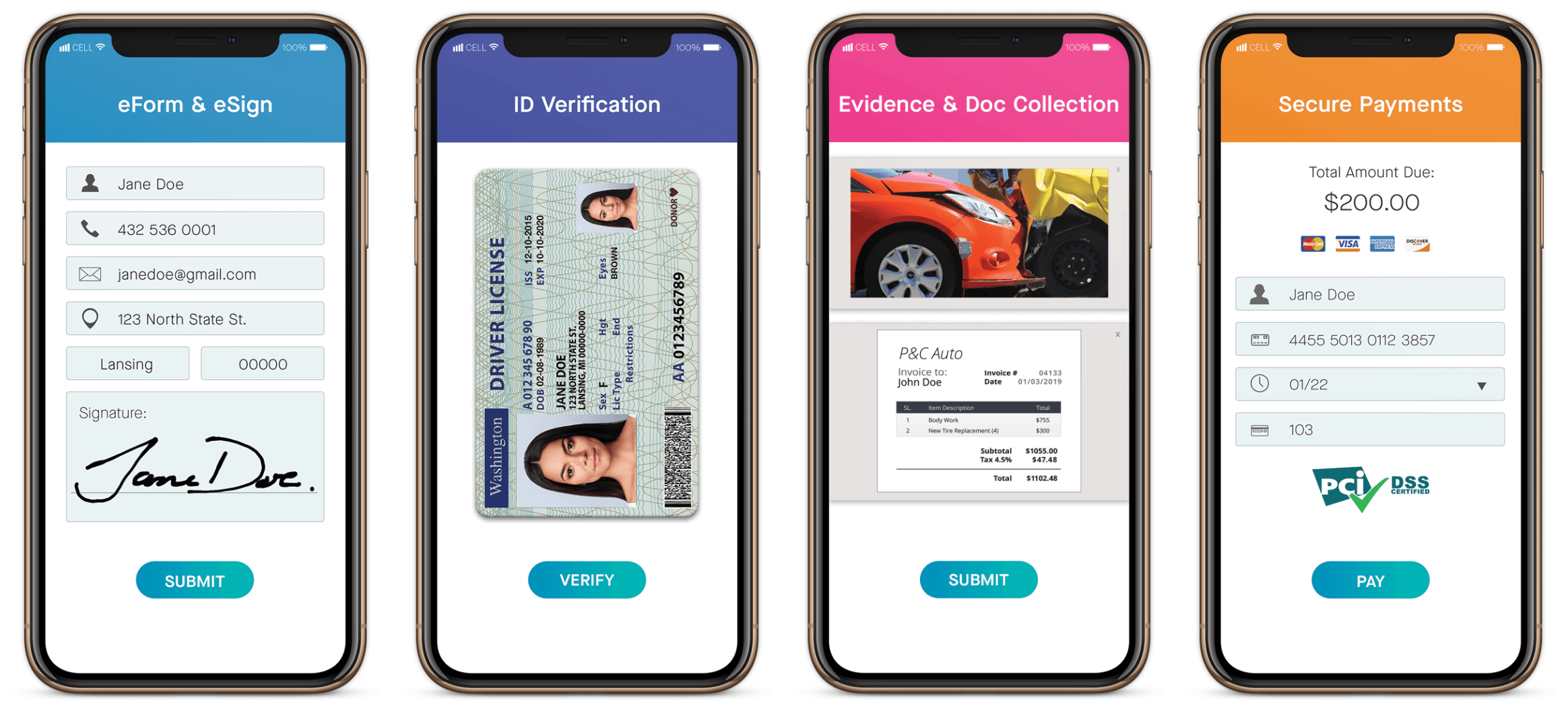

eForms and eSignatures

Customers shouldn’t need to print out forms, fill them out, scan, and email them to an agent in order to file a claim. This time-consuming process results in customers putting off filing claims and making mistakes in their applications. Documents that are NIGO are also a major burden on agents, who have to chase customers to complete and sign forms only to deal with the whole process from scratch when forms come back riddled with errors.

By digitizing forms and signatures and optimizing the interface for both mobile and desktop, customers can breeze through the claims application quickly and easily. It’s even better if they receive real-time agent guidance during the form-filling, which prevents mistakes and costly-rework and satisfies customers’ desire for both digital and human processes.

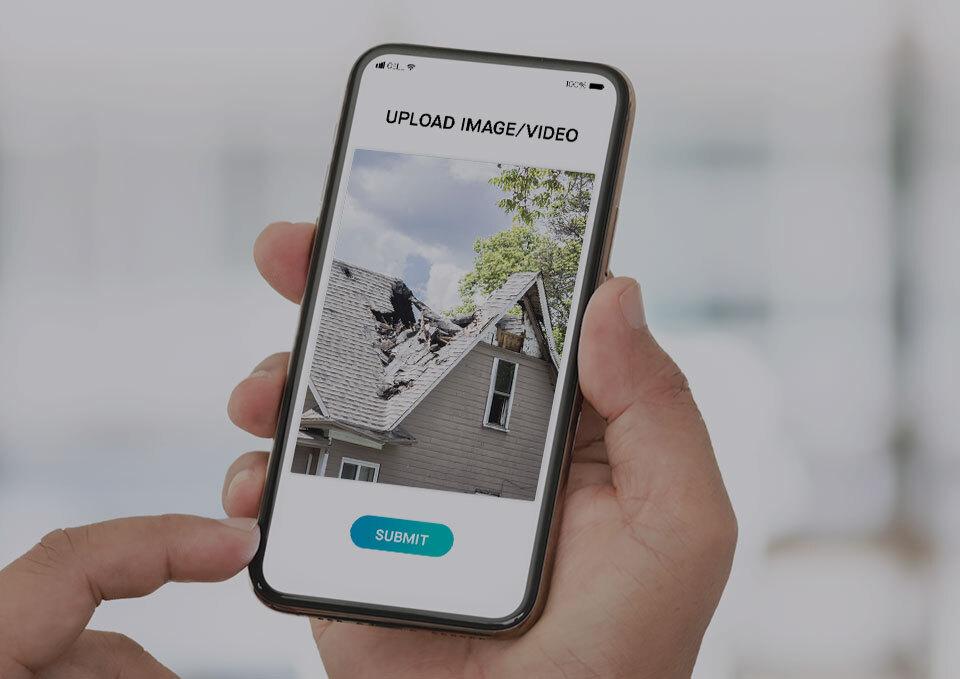

2. Digital evidence collection

Too often, the First Notice of Loss (FNOL) process is too complicated and paperwork-heavy for customers to complete at the site of an incident. This is a missed opportunity, as customers at the scene of an incident frequently only have their mobile phone readily available, and should be able to quickly begin the FNOL process as soon as they decide a claim must be filed.

To that end, customers dealing with property damage, car accidents, and related incidents should be able to easily document and send their video or photo evidence directly from their cell phones to their insurance agent. This allows the insurance company to instantly provide feedback and direction as to the next steps, get the claim into the system quickly, and minimize back and forth between policyholders and agents.

3. Instant ID verification

Insurance fraud can greatly damage insurance companies’ reputations and financial standing. Relying on post-mortem investigations to identify and analyze incidents of fraud is insufficient because it fails to prevent false claims from being paid out in the first place.

Yet traditional methods of proving identity, such as in-person meetings or scanned-and-sent documents and ID prolong the claims process and are frustrating for the majority of claimants who are legitimate.

With instant ID verification, policyholders can simply snap a picture of their photo ID, take a selfie in live mode, and upload both into the mobile session where their identity is automatically verified by AI technology. Spoofs and even “deep fakes” are instantly caught, while legitimate customers can easily move onto the next stage of the process.

4. Transparent journeys

Once customers submit an FNOL, their case often seems to fall into a black hole. They struggle to discern the status of their claim as insurance companies don’t typically provide regular updates. Customers should be able to see where they are in the claims process, from receipt of FNOL to determination of coverage to payout.

Ideally, insurance companies would also data about how their customers prefer to be interacted with –– text message, email, or phone call — and provide these regular status updates from the customers’ channel of choice.

5. Instant Payments

Similarly, notifications of instant payments such as deductibles and payouts should take place through customers’ preferred channels. Whether the payment is made through credit or bank form, customers should be immediately notified when a payment is deployed. This provides valuable peace of mind to customers, who don’t have to regularly check their bank accounts to see if the payment was received.

Digitize the entire claims process now: Try an “out of the box” digital claims solution

A fully digital filing process allows insurance companies to rapidly and easily process claims while staying compliant. On average, insurance companies that rely on digital customer interactions see 85% lower time to settle a claim, a 60% reduction in touchpoints per policy, and 15% increased customer satisfaction. This makes remote insurance claims processes not a mere stop-gap during the coronavirus, but a key way of efficiently managing claims at any time.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

These communication issues show up again when customers try to file and complete a claim in a digital, efficient, and customer-centric way — and face obstacles to do so.

While many large insurance companies offer at least partially digital claims filing options, they still often involve bouncing customers between channels (e.g., phone, fax, scanning, email), adding needless friction, prolonging turnaround times, and ultimately hurting providers’ bottom line.

These communication issues show up again when customers try to file and complete a claim in a digital, efficient, and customer-centric way — and face obstacles to do so.

While many large insurance companies offer at least partially digital claims filing options, they still often involve bouncing customers between channels (e.g., phone, fax, scanning, email), adding needless friction, prolonging turnaround times, and ultimately hurting providers’ bottom line.

Here are some of the core capabilities insurance providers can easily integrate to leverage best-in-class digital claims processes on top of their current systems:

Here are some of the core capabilities insurance providers can easily integrate to leverage best-in-class digital claims processes on top of their current systems:

Customers shouldn’t need to print out forms, fill them out, scan, and email them to an agent in order to file a claim. This time-consuming process results in customers putting off filing claims and making mistakes in their applications. Documents that are NIGO are also a major burden on agents, who have to chase customers to complete and sign forms only to deal with the whole process from scratch when forms come back riddled with errors.

By digitizing forms and signatures and optimizing the interface for both mobile and desktop, customers can breeze through the claims application quickly and easily. It’s even better if they receive real-time agent guidance during the form-filling, which prevents mistakes and costly-rework and satisfies customers’ desire for both digital and human processes.

Customers shouldn’t need to print out forms, fill them out, scan, and email them to an agent in order to file a claim. This time-consuming process results in customers putting off filing claims and making mistakes in their applications. Documents that are NIGO are also a major burden on agents, who have to chase customers to complete and sign forms only to deal with the whole process from scratch when forms come back riddled with errors.

By digitizing forms and signatures and optimizing the interface for both mobile and desktop, customers can breeze through the claims application quickly and easily. It’s even better if they receive real-time agent guidance during the form-filling, which prevents mistakes and costly-rework and satisfies customers’ desire for both digital and human processes.

Too often, the First Notice of Loss (FNOL) process is too complicated and paperwork-heavy for customers to complete at the site of an incident. This is a missed opportunity, as customers at the scene of an incident frequently only have their mobile phone readily available, and should be able to quickly begin the FNOL process as soon as they decide a claim must be filed.

To that end, customers dealing with property damage, car accidents, and related incidents should be able to easily document and send their video or photo evidence directly from their cell phones to their insurance agent. This allows the insurance company to instantly provide feedback and direction as to the next steps, get the claim into the system quickly, and minimize back and forth between policyholders and agents.

Too often, the First Notice of Loss (FNOL) process is too complicated and paperwork-heavy for customers to complete at the site of an incident. This is a missed opportunity, as customers at the scene of an incident frequently only have their mobile phone readily available, and should be able to quickly begin the FNOL process as soon as they decide a claim must be filed.

To that end, customers dealing with property damage, car accidents, and related incidents should be able to easily document and send their video or photo evidence directly from their cell phones to their insurance agent. This allows the insurance company to instantly provide feedback and direction as to the next steps, get the claim into the system quickly, and minimize back and forth between policyholders and agents.

A fully digital filing process allows insurance companies to rapidly and easily process claims while staying compliant. On average, insurance companies that rely on digital customer interactions see 85% lower time to settle a claim, a 60% reduction in touchpoints per policy, and 15% increased customer satisfaction. This makes remote insurance claims processes not a mere stop-gap during the coronavirus, but a key way of efficiently managing claims at any time.

A fully digital filing process allows insurance companies to rapidly and easily process claims while staying compliant. On average, insurance companies that rely on digital customer interactions see 85% lower time to settle a claim, a 60% reduction in touchpoints per policy, and 15% increased customer satisfaction. This makes remote insurance claims processes not a mere stop-gap during the coronavirus, but a key way of efficiently managing claims at any time.