Lost Customers, Lost Dollars: How Bad Onboarding is Bleeding Your Bank Dry

By Leor Melamedov

Ever get the feeling that these days, your bank is pouring more and more money into slick sales and marketing campaigns? If so, you’re in good company. Overall, prominent banks increased their marketing spend by 13% in 2018, equalling on average half a billion dollars. Let that sink in: a 13% increase in just one year. Half a billion dollars.

Yet while these efforts often succeed at catching prospective customers’ attention, converting them is the final battle. And disappointingly, that battle is too frequently lost once customers encounter time-consuming and confusing onboarding processes. And those processes very often send them running to the nearest competitor.

Losing customers — before they’re even won

Sound like an exaggeration? Think again. According to research by Deloitte, a whopping 40% of consumers have abandoned a bank onboarding process. When asked, the most common culprit cited was overly time-consuming paperwork and too many personal questions asked.

And who can blame them? Imagine you’re the average banking customer: You’ve signed up for quite a few services over the past few years: Uber to provide for your transport needs, Amazon Prime for your entertainment needs, Seamless for your food needs, AirBnB for your vacation needs — the list goes on.

Many of these services required little more than signing up with your Facebook credentials and adding a credit card number. A few clicks on your phone and you’re up and running. The very neurons in your brain have happily habituated to instant and automatic everything. There’s no going back.

And then one day, it’s time to join a new bank. You decide to go for whichever one your family uses, and the bank’s clever ads reassure you that you’re dealing with a modern institution that “gets” you.

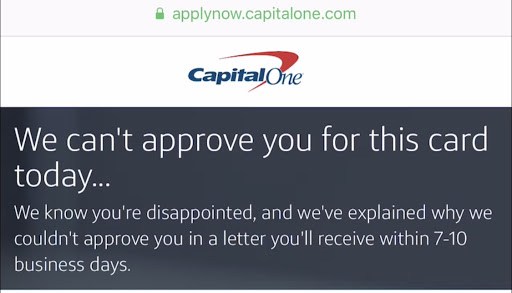

You land on the bank’s website, fill out your details to begin the process, and then bam — you’re hit with the following message:

You’re not about to wait over a week for a rejection letter. So you decide to call the bank, which takes you through an IVR system that takes you through to an agent, who transfers you to another agent, who puts you on hold…

As you wait, you’ve already opened a new tab in your browser, where you scour for another bank you’ve heard about recently. Didn’t Karen from accounting mention a digital-only bank? Sounds easy. Maybe things will go smoother with them.

(To read about real-life examples bank onboarding customer experiences, click here).

This is your first impression of the bank. Cumbersome. Time-consuming. Outdated. You start to think: if this is how I’m treated before I’ve even joined, how will things go once I’m already signed up? You conclude this isn’t the bank for you, and join the ranks of the 40% of banking customers who drop out of the onboarding process.

The real cost of bad customer onboarding

A disjointed, long, or paperwork-centric onboarding process is far from a mere annoyance: It’s a real liability for your company, draining you of precious time and money. Your customers are savvier than ever, and have more options at their fingertips than ever. Customer centricity is no longer a “nice-to-have” — it’s the battlefield you’re competing on in the fight to win new customers.

Is digitally transforming your onboarding process still low on that list of priorities? Here are a few reasons why you should reconsider:

Paperwork is expensive: A Forrester study found that an onboarding process can cost up to $25,000 per new customer, with an average cost of $6,000 per customer (this study surveyed a range of financial institutions offering consumer, commercial, and investment services).

Paperwork is time-consuming (and time=money): The same Forrester study found that the average customer is contacted ten times during the onboarding process, and must submit between five and up to a hundred documents. Imagine all the (costly) manpower hours wasted.

Lost customers are lost dollars: The average banking customer lifetime value is $45,600 (for the average customer lifespan of eight years). So every prospect that drops out of the onboarding process is $45,600 down the drain.

It’s the make-or-break for many customers: A negative onboarding experience is a big deal for all customers. But a sizeable number of customers (26%) cite easy enrollment and login as their single most important criteria for choosing a bank.

It creates a dangerous domino effect: According to research by Medallia, 35% of bank customers tell friends, family, or colleagues after a negative experience with their bank. In other words: Customers exposed to a frustrating onboarding process will be happy to help undo the reputation you’ve worked so hard to build (on the other hand, customers who have a positive experience will turn into your best advocates — 40% of those happy customers spread the word).

It’s a direct blow to your bottom line: According to Forrester, over 64% of banks report lost revenue due to problems in their onboarding processes. The flip side: McKinsey found that for every one-point increase in customer onboarding satisfaction on a ten-point Net Promoter Score (NPS) scale, there was a 3% increase in customer revenue.

Bottom line: Customer experience in bank onboarding matters

Far from fluff, the ease of your onboarding process has a direct and measurable impact on your financial institution’s revenue. But to win the battle for customers’ pockets, you must first win the battle for their hearts.

When customers decide whether they want to join you, they’re not comparing you to other banks — they’re comparing you to Amazon. To Facebook. To Netflix. To the delightful and seamless consumer services they glide through every day.

Add to that the advent of digital-first neobanks and fintech, and there’s a perfect storm threatening your seemingly-invincible bank. The last thing you want is to be the bank equivalent of Blockbuster. And customer expectations show that physical paperwork is going the way of VHS: Make sure you aren’t.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

You’re not about to wait over a week for a rejection letter. So you decide to call the bank, which takes you through an IVR system that takes you through to an agent, who transfers you to another agent, who puts you on hold…

As you wait, you’ve already opened a new tab in your browser, where you scour for another bank you’ve heard about recently. Didn’t Karen from accounting mention a digital-only bank? Sounds easy. Maybe things will go smoother with them.

(To read about real-life examples bank onboarding customer experiences, click here).

This is your first impression of the bank. Cumbersome. Time-consuming. Outdated. You start to think: if this is how I’m treated before I’ve even joined, how will things go once I’m already signed up? You conclude this isn’t the bank for you, and join the ranks of the 40% of banking customers who drop out of the onboarding process.

You’re not about to wait over a week for a rejection letter. So you decide to call the bank, which takes you through an IVR system that takes you through to an agent, who transfers you to another agent, who puts you on hold…

As you wait, you’ve already opened a new tab in your browser, where you scour for another bank you’ve heard about recently. Didn’t Karen from accounting mention a digital-only bank? Sounds easy. Maybe things will go smoother with them.

(To read about real-life examples bank onboarding customer experiences, click here).

This is your first impression of the bank. Cumbersome. Time-consuming. Outdated. You start to think: if this is how I’m treated before I’ve even joined, how will things go once I’m already signed up? You conclude this isn’t the bank for you, and join the ranks of the 40% of banking customers who drop out of the onboarding process.