New Survey: For High-Income Banking Customers, Seamless, Digital Security is Paramount

By Leor Melamedov

For higher-income earners, trusting their banks is a matter of course. These are individuals who have likely had positive or at least neutral experiences with their banks over the years, and may even have an ongoing relationship with a personal bank or financial advisor.

At the same time, a recent Lightico survey of 1,329 Americans conducted in July 2020 found that higher-income earners are significantly more likely to say that financial transactions are a matter of great sensitivity. Therefore, banks looking to increase uptake of digital channels among this important demographic must ensure that online banking incorporates security measures that are both seamless and robust.

The Surge of Interest in Online Banking

Lightico surveyed over a thousand banking customers to better gauge customer confidence, experiences, and expectations in online interactions. These issues have become especially relevant in recent months due to the continued influence of the coronavirus on consumer banking preferences. In just a short time, online banking went from being an emerging channel to the dominant one across all age groups and socioeconomic levels.

Even as restrictions on social distancing are lifted in many parts of the country, consumers continue to be wary of face-to-face interactions for fear of virus transmission. But it’s unlikely that consumers will flock back to branches, even once the coronavirus threat passes. During the period of lockdown, customers had time to grow accustomed to digital services, including online banking. And now that they’ve tasted the convenience of digital, they don’t want to go back.

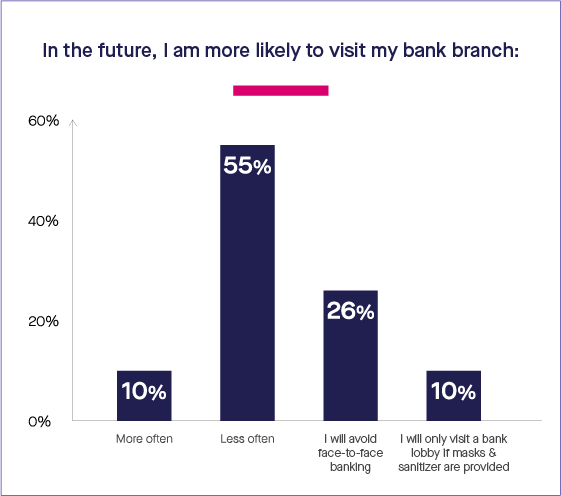

In fact, 55% of banking customers say they are likely to visit their bank branch “less often” in the future. Another 26% plan to avoid face-to-face banking altogether. And a mere 10% intend to visit their bank branch more frequently than they do today.

Of course, banks themselves have plenty of incentives to encourage customers to use a wider array of digital offerings. Digital banking is more cost-efficient; McKinsey estimates that banks can save between 20 to 25% by switching to digital processes. It’s more time-efficient; agents can focus their time on better serving customers instead of processing physical paperwork. And of course, an improved customer experience does great things for customer retention and referrals.

Online Banking Sensitive for Higher-Income Earners

But it’s not just enough to offer online banking. It needs to be perceived as a viable and secure alternative to in-person banking; otherwise, usage won’t be widespread and consistent enough to really transform the bank. In other words, consumers need to really trust online banking if they’ll be using it for more than just rudimentary tasks, like checking their bank balance.

This is particularly the case for higher-income banking customers, who are more likely than lower-income earners to depend on their banks to grow and safeguard their wealth.

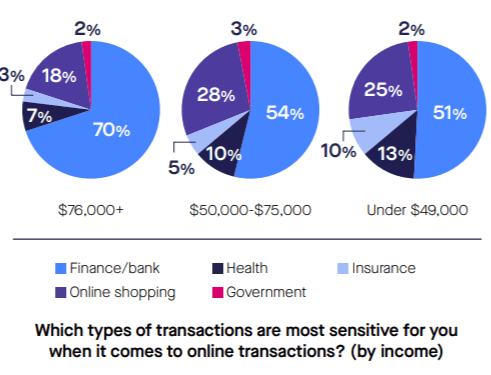

The higher-income earners in our survey (those that earn more than $76,000 a year) were significantly more likely to say that financial transactions are more sensitive to them than other types of online transactions. 70% rated financial transactions as the most sensitive, compared to just 51% of the lowest-income earners who said the same. When you have a lot, you have a lot more to lose and that translates into greater levels of sensitivity.

A Matter of Trust

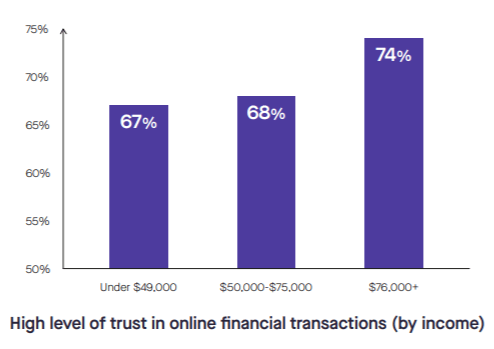

Here’s the good news: The higher the customer’s income, the more likely they are to trust online banking. 74% of higher-income earners say they have a “high level of trust in online financial transactions,” while just 67% of lower-income customers say the same.

But this trust cannot be taken for granted. Higher-income earners’ sensitivity to financial matters means that even the appearance of lax security may cause them to shy away from online banking when it comes to important matters like opening an account or transferring large sums of money. Banks that invest significant time, effort, and funds in setting up digital infrastructure will not see the expected ROI if their most desirable customers hesitate to fully embrace online banking due to security concerns.

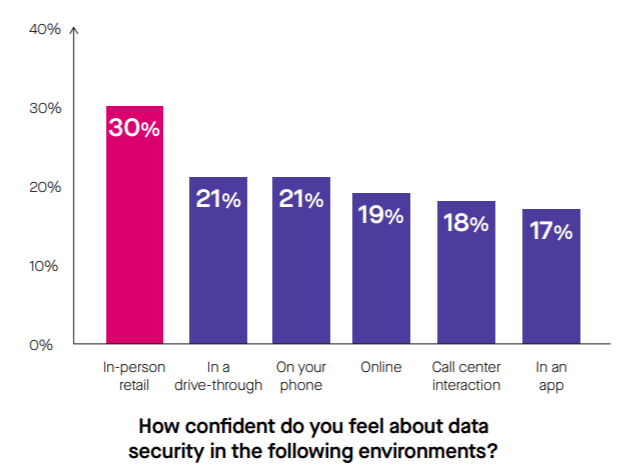

Indeed, the survey reveals that customers continue to perceive in-person banking as the most secure environment. This suggests that while customers may prefer online banking for simple transactions, in-person may still be widely seen as the gold standard when the financial stakes are higher. For banks that want to meet their higher-income customers’ standards, they will need to continue to invest in visible security features.

Not Just Any Security, But Seamless Security

Banks have a delicate balance to be aware of: on the one hand, security measures are needed to reassure customers that their wealth and privacy is secure. On the other hand, customers should be able to complete security checks from a single channel without being bounced around.

That’s where digital-first tools like photo ID verification, biometric fingerprint access, and digital signatures come into play. These non-intrusive tools allow banks to provide their customers with peace of mind without defeating the original purpose of online banking, which is to enable seamless and effortless customer processes.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

In fact, 55% of banking customers say they are likely to visit their bank branch “less often” in the future. Another 26% plan to avoid face-to-face banking altogether. And a mere 10% intend to visit their bank branch more frequently than they do today.

Of course, banks themselves have plenty of incentives to encourage customers to use a wider array of digital offerings. Digital banking is more cost-efficient; McKinsey estimates that banks can save between 20 to 25% by switching to digital processes. It’s more time-efficient; agents can focus their time on better serving customers instead of processing physical paperwork. And of course, an improved customer experience does great things for customer retention and referrals.

In fact, 55% of banking customers say they are likely to visit their bank branch “less often” in the future. Another 26% plan to avoid face-to-face banking altogether. And a mere 10% intend to visit their bank branch more frequently than they do today.

Of course, banks themselves have plenty of incentives to encourage customers to use a wider array of digital offerings. Digital banking is more cost-efficient; McKinsey estimates that banks can save between 20 to 25% by switching to digital processes. It’s more time-efficient; agents can focus their time on better serving customers instead of processing physical paperwork. And of course, an improved customer experience does great things for customer retention and referrals.

The higher-income earners in our survey (those that earn more than $76,000 a year) were significantly more likely to say that financial transactions are more sensitive to them than other types of online transactions. 70% rated financial transactions as the most sensitive, compared to just 51% of the lowest-income earners who said the same. When you have a lot, you have a lot more to lose and that translates into greater levels of sensitivity.

The higher-income earners in our survey (those that earn more than $76,000 a year) were significantly more likely to say that financial transactions are more sensitive to them than other types of online transactions. 70% rated financial transactions as the most sensitive, compared to just 51% of the lowest-income earners who said the same. When you have a lot, you have a lot more to lose and that translates into greater levels of sensitivity.

But this trust cannot be taken for granted. Higher-income earners’ sensitivity to financial matters means that even the appearance of lax security may cause them to shy away from online banking when it comes to important matters like opening an account or transferring large sums of money. Banks that invest significant time, effort, and funds in setting up digital infrastructure will not see the expected ROI if their most desirable customers hesitate to fully embrace online banking due to security concerns.

But this trust cannot be taken for granted. Higher-income earners’ sensitivity to financial matters means that even the appearance of lax security may cause them to shy away from online banking when it comes to important matters like opening an account or transferring large sums of money. Banks that invest significant time, effort, and funds in setting up digital infrastructure will not see the expected ROI if their most desirable customers hesitate to fully embrace online banking due to security concerns.

Indeed, the survey reveals that customers continue to perceive in-person banking as the most secure environment. This suggests that while customers may prefer online banking for simple transactions, in-person may still be widely seen as the gold standard when the financial stakes are higher. For banks that want to meet their higher-income customers’ standards, they will need to continue to invest in visible security features.

Indeed, the survey reveals that customers continue to perceive in-person banking as the most secure environment. This suggests that while customers may prefer online banking for simple transactions, in-person may still be widely seen as the gold standard when the financial stakes are higher. For banks that want to meet their higher-income customers’ standards, they will need to continue to invest in visible security features.