Overworked Call Centers & Inefficient Branches: Why Banks Need Self-Service More Than Ever

By Gaby Young

Easy-to-use self-service options for banking customers were already a high priority for financial institutions before the COVID-19 pandemic came along. Today? They're downright critical.

Speed, efficiency and convenience have increasingly become staple consumer expectations, and automated workflows are a vital digital transformation investment for banks to meet these needs and give customers the convenience to complete tasks from wherever they are.

That convenience translates directly into the kind of profitability that comes with long-term customer loyalty by accelerating key banking processes that drive revenue such as loans, lines of credit, credit cards, and more.

But when self-service options are incomplete for many of the banking processes customers depend on — increased overhead costs banks significantly: Call centers are flooded with mundane customer issues that should be Do-it-Yourself. Branch staff wastes time with servicing while rightly hearing questions from customers about why they can’t just do this online.

Adding work to processes that should be self-service frustrates banking employees and slows productivity. This friction also spills over to the customer experience.

The less efficient these banking workflows are and the more effort they make their customers go through just to do business — the further away banks find themselves from gaining their loyalty.

Research by Gartner shows that an overwhelming 96% of customers become disloyal after having a high-effort interaction.

Broken Customer Journeys Mean Self-Service Simply Isn’t Working for Banking Customers

In recent years banks have invested in developing web pages, portals, and mobile applications. Let’s take a look at how banks’ current attempts at delivering self-service options actually play out in the experience of their customers. One of the ways we put these processes to the test was to hear first-hand the experiences of college students trying to apply for bank accounts and credit cards from 3 major banks on mobile apps and online.

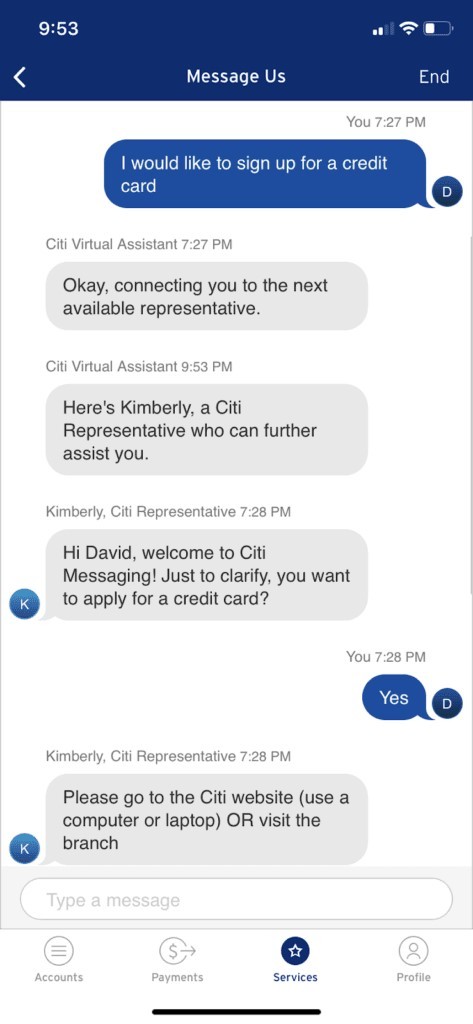

One student was having trouble finding where they can apply for a credit card on Citi Bank’s mobile app, so they clicked on the live chat option on the site.

In the screenshot below, you can see why this flow was such a customer experience fail. First, after the student makes it clear from the start that they’d like to sign up for a credit card, they are told they’re going to be connected to a representative — but they don’t hear back for over 2 hours.

When they finally do hear back, instead of being guided online through all the steps they need to take to apply for a new credit card, they’re essentially bounced off of the app and asked to either visit the bank’s website or trek out to a branch — exactly the opposite of a self-service option for this prospective customer.

This is one of just many broken customer journeys that force consumers to chase banks just to be their customers.

Whether a customer needs to complete the simplest of tasks like a change of address, or applying for a high-value transaction such as a line of credit, the majority of banking workflows today re-route customers across different channels — and more often than not the slowest and least convenient one for them.

The reasons why these self-service journeys are so frustrating and difficult to complete are digital silos and legacy processes.

Digital Silos & Legacy Processes Bounce Customers Out of Self-Service Channels

In their quest to minimize paper-based processes and digitize workflows, banks have brought on board a variety of different point solutions. Entirely separate software solutions are pieced together to complete customer-facing experiences such as submitting forms and required documents, verifying ID, digitally signing applications, and approving legally binding terms and conditions.

The limitations of these siloed systems mean they are capable of handling just one major stop along the customer journey. Implementing these standalone tools typically demands substantial coding by the IT department. They also don’t integrate well with existing systems — and therefore don’t communicate automatically with each other — an inherent flaw that guarantees customers must jump multiple hurdles and repeatedly re-enter the same information multiple times in each new step.

Too many digital touchpoints complicate and slow banking workflows enough, but that’s just one-half of the problem. It’s also the types of touchpoints that frustrate banking customers.

In the absence of automated workflows to complete all of these steps, banks must staff employees upfront just to assist or support customers in completing requests that should easily be completed digitally. And those employees must rely on legacy processes that impose both manual and paperwork on them and the customers they serve.

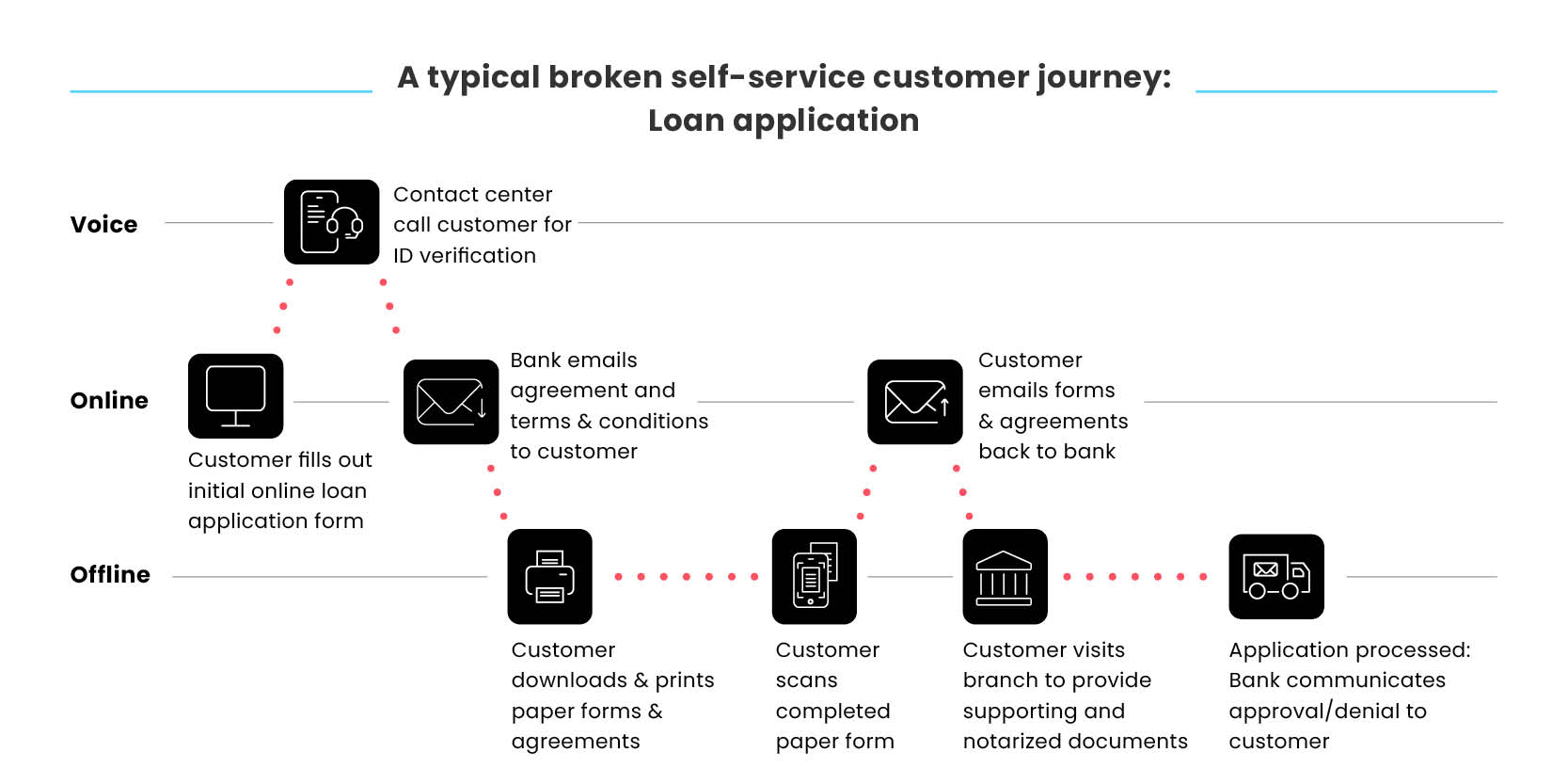

A banking customer applying for a loan may start out using a self-service option from their mobile in hopes they can complete their application while commuting home or juggling one of the many other tasks on their plate.

Many banks today still have limited digital options that make it possible for customers to complete or submit forms and documents online. That’s why as soon as more information is needed, they’ll likely send this customer a busy PDF-based form that they need to read through and try to understand from their small smartphone screen.

If they have questions on important requirements or conditions, they’ll need to put in a call to the contact center and wait to speak to an agent while toggling back and forth from call to PDF form on their phone.

If proof of income or salary records are required, they’ll need to separately attach these files and email them back to the bank, or simply take time out of the next possible workday to visit the branch just so they can be done with the process.

Because of legacy processes and digital silos, far too few banking processes that begin as “self-service” ever end off that way, and it’s customers who bear the brunt of the inconvenience.

With such intense competition from digital-first Neobanks to attract new customers, traditional banks can ill-afford to keep turning banking experiences into a lengthy and arduous process. Today’s customers simply will not tolerate it.

Adding friction to each part of the customer’s experience results in:

Poor onboard rates: More customers abandon their banking journey and fewer end up onboarding due to uncomfortable, time-consuming tasks and repetitive compliance requirements.

Slower Turnaround times: Excessive amount of banking employee time and resources are expended on chasing customers for documents and signatures.

Damaged NPS: Customer satisfaction suffers due to lengthy, unclear, and often painstaking manual processes.

Helping Customers Help Themselves Through Digital Completion

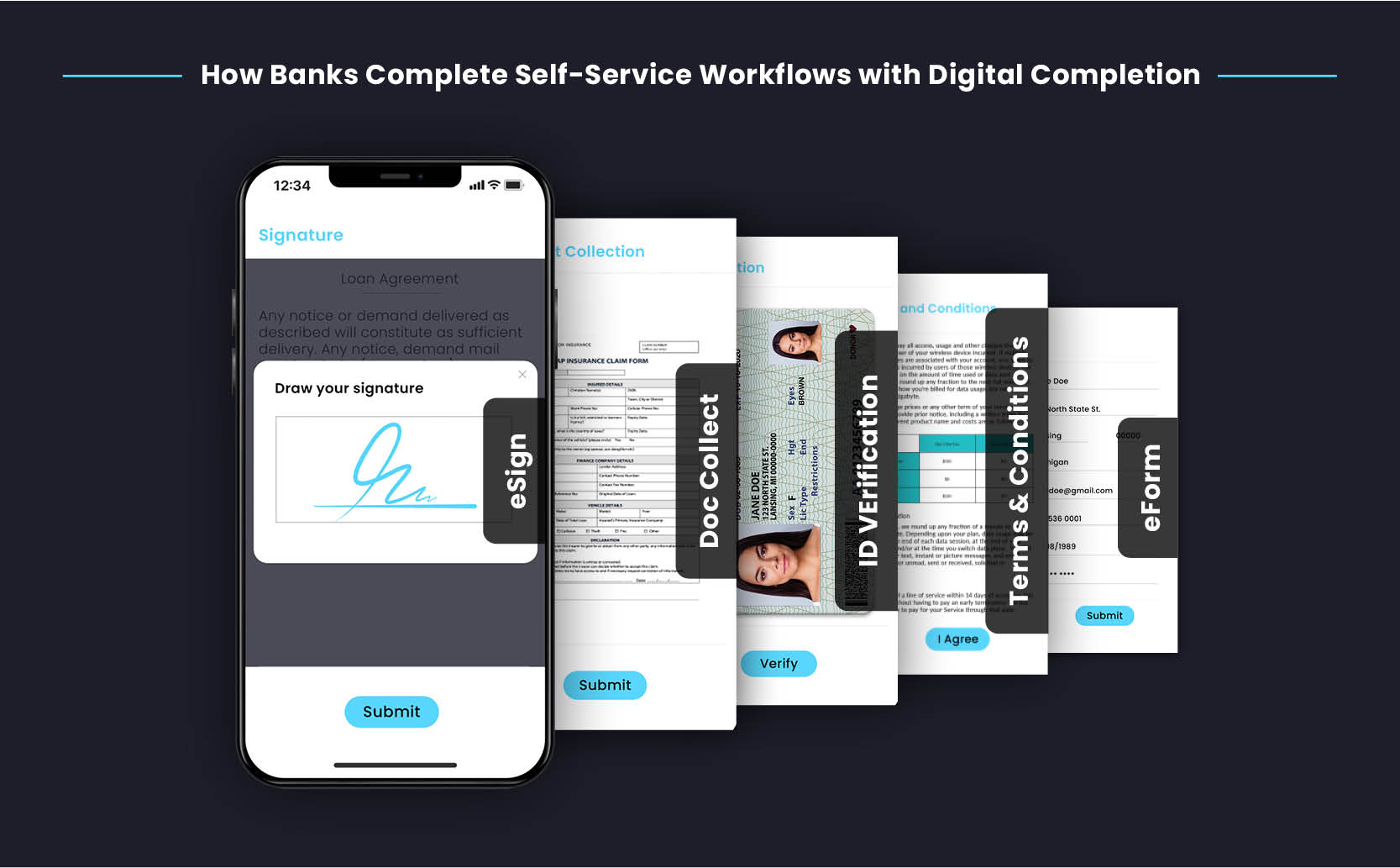

Automated digital workflows are designed to eliminate the digital silos and legacy processes holding banking capabilities back from delivering digitally complete self-service options for their customers.

A Digital Completion solution integrates these workflows seamlessly into your bank’s existing infrastructure using flexible APIs. To scale yet customize workflows across a wide variety of customer-facing banking processes, a digitally complete workflow should require no code by IT, and should allow project managers to set up their own business rules and make adjustments on the fly by applying conditional logic.

This allows for one completely digital self-service customer experience from start to finish. After first engaging the bank, a customer receives an SMS or email with a link that starts an interactive session through Interactive Voice Response (IVR), website engagement, or any other self-service link option.

This intuitive digital session guides the customer through workflow tailored for precisely their use case, allowing them to complete eForms and digitally sign them, verify ID, upload supporting records or documents, and instantly grant consent to the terms and conditions of an agreement.

Financial institutions currently digitizing self-service workflows:

Increase First-call Resolution

Improve self-service rate

Simplify document/form collection in the customer’s channel of choice

Reduce staff overhead

Ensure consistent compliance

Improve customer experience and NPS

Automated and digitally complete journeys are designed for the speed of life of today’s customers so they can get banking tasks done from their mobile or most preferred channel. Customers can run through self-service requests just as easily as their favorite consumer apps by tapping and swiping through each step in one simple and user-friendly digital session.

By replacing digital silos with these fully remote processes, banks can speed and simplify banking processes for their customers, helping them accelerate application cycles and drive revenue growth while minimizing the risk of losing prospects during onboarding. And by making it effortless for customers to open banking products and services, they’re equipped to compete in the digital age and win the long-term loyalty of today’s generation of customers.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

This is one of just many broken customer journeys that force consumers to chase banks just to be their customers.

This is one of just many broken customer journeys that force consumers to chase banks just to be their customers.

Because of legacy processes and digital silos, far too few banking processes that begin as “self-service” ever end off that way, and it’s customers who bear the brunt of the inconvenience.

With such intense competition from digital-first Neobanks to attract new customers, traditional banks can ill-afford to keep turning banking experiences into a lengthy and arduous process. Today’s customers simply will not tolerate it.

Adding friction to each part of the customer’s experience results in:

Because of legacy processes and digital silos, far too few banking processes that begin as “self-service” ever end off that way, and it’s customers who bear the brunt of the inconvenience.

With such intense competition from digital-first Neobanks to attract new customers, traditional banks can ill-afford to keep turning banking experiences into a lengthy and arduous process. Today’s customers simply will not tolerate it.

Adding friction to each part of the customer’s experience results in:

Financial institutions currently digitizing self-service workflows:

Financial institutions currently digitizing self-service workflows: