Why eSignatures Matter More Than Ever in The COVID-19 Era

By Leor Melamedov

Even before the coronavirus pandemic struck, Americans’ interest in digitally interacting with their banks, insurance companies, auto lenders, and many other institutions was at an all-time high. But the crisis set off unprecedented demand for eSignatures and other types of digital frontend solutions.

Here are some of the reasons why the newest generation of eSignatures and related digital customer interaction solutions are here to stay as we enter into the “new normal,” post-lockdown era.

Lockdown habits have become entrenched

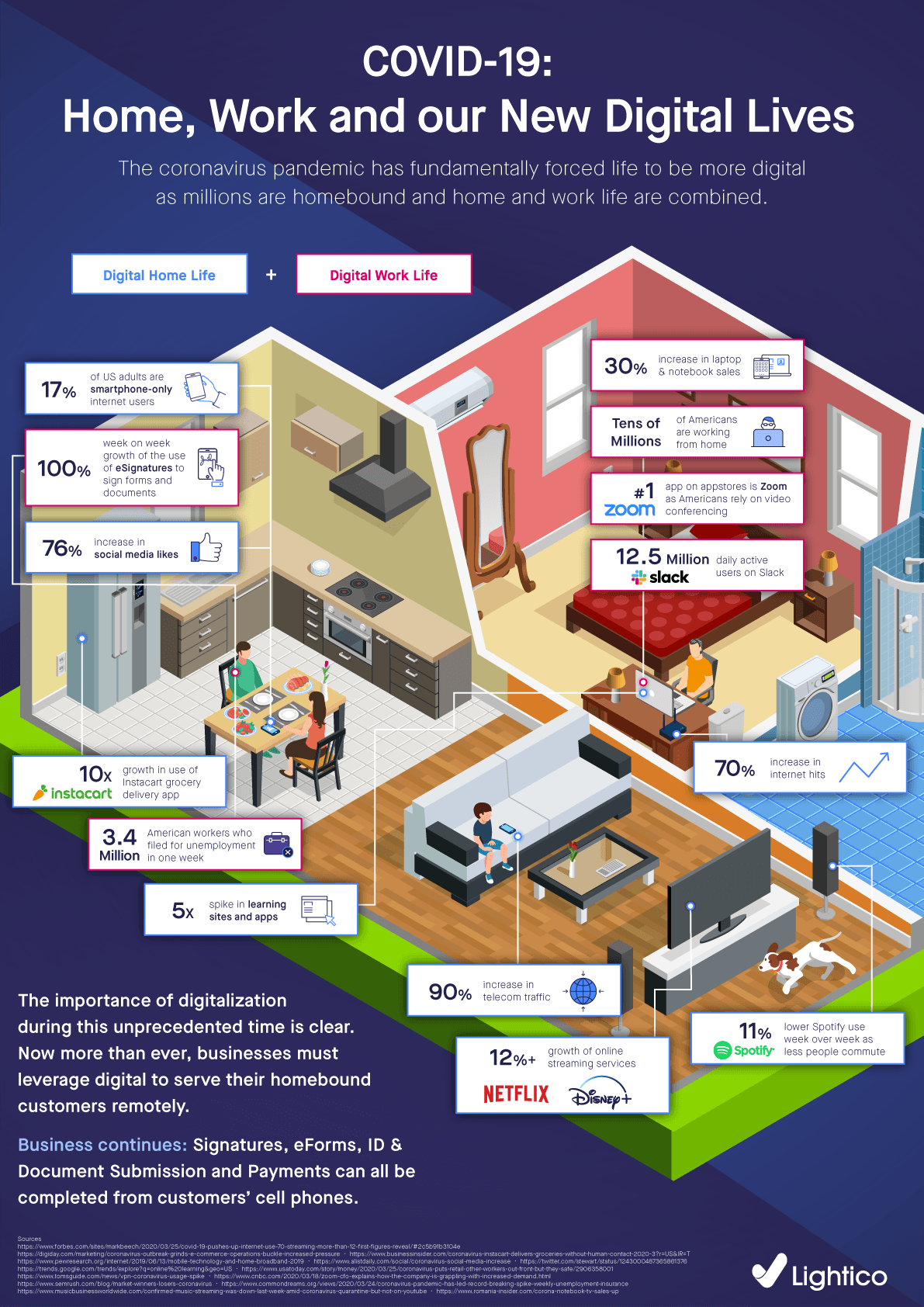

For nearly two or three months, people established new remote habits in an attempt to avoid the pathogen. People whose jobs could be done remotely flocked to Zoom and worked from home; the Internet became the bloodline for both professional and social interaction; telemedicine boomed as patients tried to bypass potentially infected clinics.

Industries that had previously required customers to complete a process by coming into a physical location had to immediately offer and promote viable digital alternatives to keep customers and employees safe.

The result of companies’ push for digital was that even groups that normally wouldn’t have opted for digital transactions got exposure to it. Whereas in the past, eSignatures might have sounded intimidating to older users, many have had to use it for safety reasons. Along the way, they got a taste of the convenience of being able to sign from anywhere –– and they’re not eager to go back to traditional processes.

A recent Lightico survey confirms this phenomenon, finding that 79% of banking customers want more all-digital processes with their bank. Even safety measures won’t make people want to come back to sign in person; only 26% of banking customers say they want in-branch banking with safety-related precautions in place. Clearly, people are in no rush to go back to the old ways of doing things with lines, paperwork, and bouncing between channels.

2. eSignatures reduce costs

The coronavirus is taking a financial toll on companies, making it necessary to carefully assess every expenditure.

According to a Berenberg study of 38 European and U.S. banks, banks will suffer an estimated 8.5% decline in revenue in 2020, and 30% fewer earnings than was expected for this year. Cutting unnecessary operational and overhead costs will be a priority given this reality.

Paperwork is a prime example of waste given today’s digital alternatives. Processing paperwork costs companies a tremendous amount of money both in terms of the monetary value of manpower hours spent, and the costs of accoutrements such as envelopes, stamps, printers, and scanners.

On the other hand, digital tools such as mobile eSignatures are far more economical thanks to the lower processing costs and scalability.

Research shows that a typical customer transaction at a physical bank location costs banks $4 per transaction, while banking from a desktop or laptop computer costs just $0.09 per transaction. Most cost-effective of all is mobile banking, which costs financial institutions a mere $0.019 per transaction.

3. eSignatures save precious agent time

Agents’ time is limited, and ideally much of it should be spent on higher-value activities such as guiding and advising clients. Instead, it is largely spent on manually processing physical paperwork, chasing customers for signatures and documents, and handling mistakes in forms that need to be filled out again.

In addition, for many companies, the “Great Lockdown” has brought reduced staff and limited servicing capabilities. Many contact centers are also swamped with phone calls, often related to requests for financial relief such as loan deferments. Companies are expected to do more with fewer resources, making digital tools essential for keeping up with consumer demand for services.

4. Data integrity of digital forms vs. paper

The coronavirus has made many customers and businesses question the supremacy of in-person business transactions. But maintaining the integrity of sensitive customer data is critical, whether it’s with digital or paper documents and forms.

The good news is that digital signatures are often even more secure than wet signatures on paper. That’s because digital signatures rely on two cryptographic keys, a public key and a private key, to ensure that the eSignature is valid. Furthermore, a trusted certificate authority (CA) guarantees the integrity of these keys, ensuring that the technology that enables the eSignature is secure.

Meanwhile, wet signatures are comparatively easy to forge. For example, a person with a very simple signature, or whose signature has a lot of variation, is a prime target for forgeries. There is no such risk with eSignatures, which rely on advanced cryptography methods to ensure data integrity.

5. Compliance and validated audit trails

When the authenticity of a wet signature is being investigated in a court, the signature’s appearance is typically compared to other signatures. Handwriting experts are called in, and judgment calls have to be made to decide whether a signature is fraudulent or real. As previously stated, simple or variable signature styles are often difficult to authenticate as genuine beyond a shadow of a doubt.

Furthermore, even if the initial signature was genuine, tampering after the fact is always a possibility.

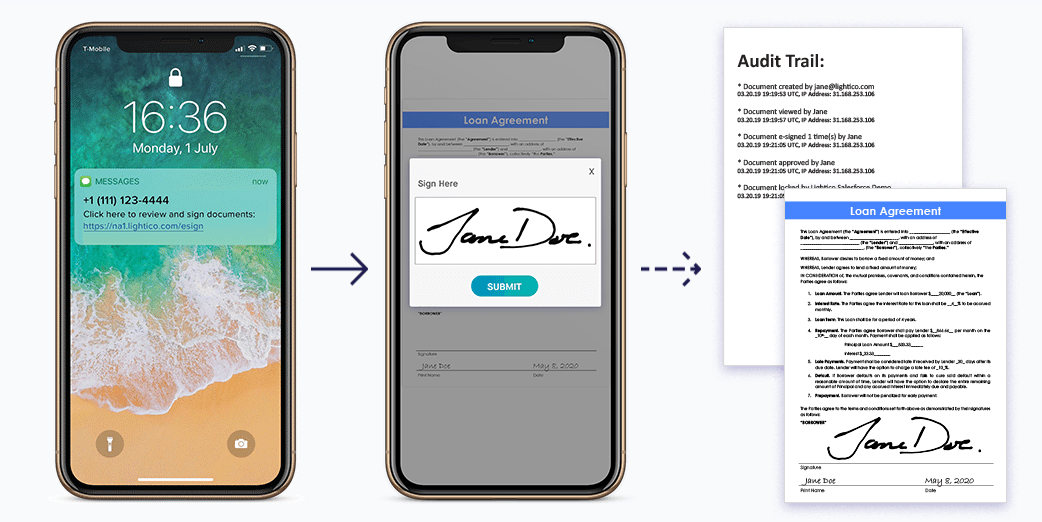

In contrast, if there is ever a legal dispute involving an eSignature, there are more mechanisms in place that can validate or invalidate its authenticity. Furthermore, eSignatures cannot be subjected to tampering as they are securely saved in a CRM with a legally binding, time-stamped audit trail.

But not all eSignatures are equally effective

Organizations interested in meeting consumer demand, reducing costs, and improving agents’ efficiency will always do better by choosing eSignatures over traditional wet signatures. Yet even within the category of eSignatures, there is considerable variation of effectiveness.

The Consumer Financial Protection Bureau (CFPB) found that many banks were actually dissatisfied with the legacy eSignature solutions they were using. That’s because those eSignature solutions require customers to access email to sign, resulting in prolonged, dropped, or repeat calls to contact centers when email access is not readily available.

For this reason, CFPB is temporarily suspending the requirement for banks to require clumsy legacy eSignatures for customers, permitting more intuitive compliance fulfillment like oral consent. This measure is a result of trying to ease the pressures banks face to process a great number of transactions often under suboptimal conditions, where compliance CX is critical.

On the other hand, next-generation eSignature solutions are mobile-optimized, allowing companies to collect eSignatures, receive forms and documents, and verify ID by sending a simple text message link to the customer’s phone that opens to a secure mobile environment.

By collecting customer consent in real time via customers’ mobile phones, companies can stop chasing customers for their signatures, and sell and service with greater efficiency.

Lightico is one such cutting-edge eSignature solution, allowing companies across diverse industries to serve customers in a remote and streamlined manner. Learn more at Lightico.com.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

For nearly two or three months, people established new remote habits in an attempt to avoid the pathogen. People whose jobs could be done remotely flocked to Zoom and worked from home; the Internet became the bloodline for both professional and social interaction; telemedicine boomed as patients tried to bypass potentially infected clinics.

Industries that had previously required customers to complete a process by coming into a physical location had to immediately offer and promote viable digital alternatives to keep customers and employees safe.

The result of companies’ push for digital was that even groups that normally wouldn’t have opted for digital transactions got exposure to it. Whereas in the past, eSignatures might have sounded intimidating to older users, many have had to use it for safety reasons. Along the way, they got a taste of the convenience of being able to sign from anywhere –– and they’re not eager to go back to traditional processes.

A recent Lightico survey confirms this phenomenon, finding that 79% of banking customers want more all-digital processes with their bank. Even safety measures won’t make people want to come back to sign in person; only 26% of banking customers say they want in-branch banking with safety-related precautions in place. Clearly, people are in no rush to go back to the old ways of doing things with lines, paperwork, and bouncing between channels.

For nearly two or three months, people established new remote habits in an attempt to avoid the pathogen. People whose jobs could be done remotely flocked to Zoom and worked from home; the Internet became the bloodline for both professional and social interaction; telemedicine boomed as patients tried to bypass potentially infected clinics.

Industries that had previously required customers to complete a process by coming into a physical location had to immediately offer and promote viable digital alternatives to keep customers and employees safe.

The result of companies’ push for digital was that even groups that normally wouldn’t have opted for digital transactions got exposure to it. Whereas in the past, eSignatures might have sounded intimidating to older users, many have had to use it for safety reasons. Along the way, they got a taste of the convenience of being able to sign from anywhere –– and they’re not eager to go back to traditional processes.

A recent Lightico survey confirms this phenomenon, finding that 79% of banking customers want more all-digital processes with their bank. Even safety measures won’t make people want to come back to sign in person; only 26% of banking customers say they want in-branch banking with safety-related precautions in place. Clearly, people are in no rush to go back to the old ways of doing things with lines, paperwork, and bouncing between channels.