How Banks Can Choose the Right Customer Onboarding Software in 2021

By Leor Melamedov

A great customer onboarding experience has the power to increase conversions, improve banks’ reputations, and boost efficiencies. In the “new normal” of remote banking transactions, it’s imperative that banks in 2021 choose onboarding software that’s built for digital from the ground up.

In addition, banks have to play double duty when deciding on digital customer onboarding software. On the one hand, the software must aid in staying compliant with regulations including KYC, AML, Dodd-Frank, and others. On the other hand, the software must be intuitive and easy for both customers and agents to use.

With all these considerations, it can be challenging to decide which onboarding software is best suited for a bank’s needs. Here, we’ll explain why the right customer onboarding software can make or break a bank’s success, and a few questions to ask that can make evaluating potential solutions easier.

Why the Choice of Customer Onboarding Software Matters

Banks are constantly faced with choices about which banking technology to invest in. From the core system to robotic process automation (RPA) to loan origination software (LOS), there is no end to the types of technologies that can enhance banks’ processes.

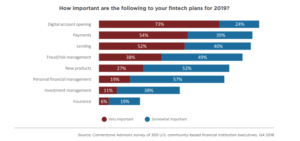

But digital customer onboarding is an overwhelming priority for banking executives, even compared to other important technologies:

And with good reason. Bad onboarding — whether due to insufficient digital processes, excessive customer touchpoints, over-reliance on manual processes, or some combination of these — can seriously hurt banks’ success.

Here are some of the costs of cumbersome, slow onboarding processes:

Loss of revenue: In 2020 alone, the global commercial banking market lost $3.3 trillion due to abandoned applications during onboarding.

Loss of business to digital-first competitors: 78% of banks say they have lost customers to neobanks.

Failure to satisfy meet customer expectations: A survey conducted in the middle of the coronavirus pandemic found that 79% of customers want more all-digital processes from their bank in the future.

Wasted time: On average, it takes 26 days for financial institutions to onboard new customers. Clients are contacted on average four times during the onboarding process. For corporate clients, they were contacted on average eight times. This represents significant time wasted for both customers and the agents who serve them.

Of course, it’s not that banks think this is acceptable. Most banks are keenly aware that current onboarding processes are broken and costing them in multiple ways. But the fear of being non-compliant with banking regulations leads to adding new KYC onboarding requirements. For instance, the perception that hard copies are more compliant means that banks commonly redirect customers to a physical branch during the digital onboarding process.

Banks urgently need a way to streamline onboarding while ensuring regulatory compliance. And adopting effective and intuitive onboarding software is often the best way to undo the damage of traditional onboarding.

Customer Onboarding Software For Banks: Factors to Consider

With multiple options for digital customer onboarding software available on the market, banks need to evaluate which will best fit their needs. Whichever software they choose will need to collect customer information and consent, verify customer identity, and open customer accounts.

Common onboarding features may include ID verification, digital document collection, smart eForms, eSignatures, and more.

Some digital onboarding solutions harness AI to determine whether ID and documents are legitimate, facial recognition to compare a customer’s selfie with their photo ID, time-stamps and audit trails to ensure court-admissability, and automated digital workflows to cut down on agent decision-making and manual work.

The process of evaluating customer onboarding software should include a review of key attributes. Here are some of the most important ones:

1. Promotes Compliance With Top Banking Regulations

Understandably, banks’ top priority is staying compliant. Therefore, any onboarding software must meet or exceed the standards of paper-based regulatory paperwork. The software should:

Ensure compliance with KYC, AML FTFCA, Dodd-Frank, CRS, MiFID II, EMIR, and others.

Allow admins to easily update business rules, form fields, and document requirements in response to changing regulations.

Use a robust digital ID verification system that allows customers to instantly submit their photo ID and selfie for automatic verification.

Collect all documents and forms from a secure environment that uses technology such as single sign-on, one-time passwords, audit trails, and HTTPS encryption. The more layers of (seamless) security, the better.

2. Allows Customers to Onboard From Anywhere

Today’s banking customers expect to be able to open a new account from anywhere, and from any device. Customers should:

Enjoy a consistent, intuitive onboarding experience whether they’re completing the process from a smartphone, tablet, desktop computer, or any other channel.

Be free to onboard from a call center, physical branch, drive through, or online.

Be free to onboard without the involvement of devices such as printers and scanners, which limit them to onboarding from specific locations.

Be able to complete the entire onboarding process from wherever they happen to be, without the need to switch channels or visit a branch at any stage.

3. Makes the Most of Agent Talent

Client onboarding software isn’t meant to replace bank agents. It’s mean to augment them. Customers in the process of onboarding should still have access to over-the-phone agents who can walk them through the form-filling and KYC procedures, and answer any questions. Agents should:

Be able to view the customer’s onboarding application in real-time from their own consoles.

Know exactly which documents and forms are required from which customers based on customer type (e.g., business client, high-risk client). Business process automation can make requirements crystal clear.

Facilitate digital ID verification with limited to no manual effort.

Spend less time processing paperwork, and more time on higher-order activities such as offering guidance and relevant cross-selling.

4. Offers Self-Onboarding

The best customer onboarding software can be used in flexible ways. Just as some customers want an agent to guide them through the digital onboarding process, other customers would rather go it alone. This is particularly the case for retail bank customers with simpler needs. Self-onboarding should:

Be able to be entirely completed from within an email body or website.

Allow existing bank customers, whose information is already in the system, to apply for additional accounts without having to repeat information (via pre-populated forms).

Allow new customers to fill out application forms, upload stipulations, read and consent to T&Cs, and apply for credit cards.

Allow customers to get help if they decide they need it by embedding a live chat option and clearly displaying the call center number.

5. Includes API That Plugs Into Core System

Onboarding software shouldn’t and can’t be a standalone technology. It’s meant to integrate into existing systems, allowing banks to maximize their ROI from currently used tools. Onboarding software should include APIs that integrate with:

Existing workflows

CRMs

Agent toolbars

Third-party business applications

Agent call center toolbars

Stay Compliant and Fast With Bank Onboarding Software

The right bank onboarding system allows banks to satisfy regulatory requirements without sacrificing speed and efficiency. With advanced banking technology baked into the software, customers can onboard easily and from anywhere.

Here are some of the immediate benefits banks can get from the right digital onboarding software:

Improved completion rates: Banks no longer see customers abandoning the onboarding process due to lengthy application forms and excess friction.

Fewer callbacks: Customers are able to complete the entire onboarding process in one shot, from one channel. This eliminates the need for them to call again, or for agents to follow up.

Fewer compliance issues: With automated onboarding workflows, agents know exactly which stipulations are required from which customers, preventing compliance lapses.

Improved customer experience: New customers feel they have received the “white glove” treatment even before they hold an active account, contributing to a positive NPS early on in the customer lifecycle.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

And with good reason. Bad onboarding — whether due to insufficient digital processes, excessive customer touchpoints, over-reliance on manual processes, or some combination of these — can seriously hurt banks’ success.

Here are some of the costs of cumbersome, slow onboarding processes:

And with good reason. Bad onboarding — whether due to insufficient digital processes, excessive customer touchpoints, over-reliance on manual processes, or some combination of these — can seriously hurt banks’ success.

Here are some of the costs of cumbersome, slow onboarding processes: