How to Maximize Insurance Policy Sales in a Remote World

By Leor Melamedov

The coronavirus pandemic has meant lagging business for most industries, but not insurance. In fact, since the height of the pandemic, many insurance companies have seen an uptick in new policy sales. While this is obviously a welcome development for insurers, there is a catch: Many providers were accustomed to face-to-face sales and struggled to transition to selling policies in a fully remote environment.

Even while the lockdown is starting to be lifted across the U.S., but the pandemic continues to rage on. So while people are now allowed to conduct business in person, that doesn’t mean they feel comfortable doing so. Offering a streamlined, fully remote insurance sales process ensures that nothing will stand in the way of interested customers getting the insurance coverage they need and want.

Growing opportunities to serve new policyholders

Americans took a financial hit during the pandemic, and they continue to suffer from financial uncertainty even now that lockdowns are being lifted. As a result, consumer confidence as of June 2020 remains at the same low level it reached in April, according to McKinsey.

Yet consumers’ financial worries haven’t curbed their interest in expanding their insurance coverage. A recent Lightico study found that 21% of U.S. consumers are currently looking for new auto or home insurance, with 19% interested in expanding their life insurance coverage.

Interestingly, those consumers who were directly affected by the coronavirus — either because they were infected or someone they know was infected — show double the interest in purchasing new insurance plans. It’s likely that having experienced or witnessed a worst-case scenario come true increases risk-prevention behavior, such as purchasing insurance. Yet consumers as a whole seem to demonstrate high intent to buy insurance.

Missed opportunities due to insufficient remote communication

Opportunities to sell new policies may be high, but insurance companies shouldn’t rest on their laurels. Quite the opposite. Customers who wish to purchase policies or modify existing ones face obstacles when it comes to smooth communication with their providers.

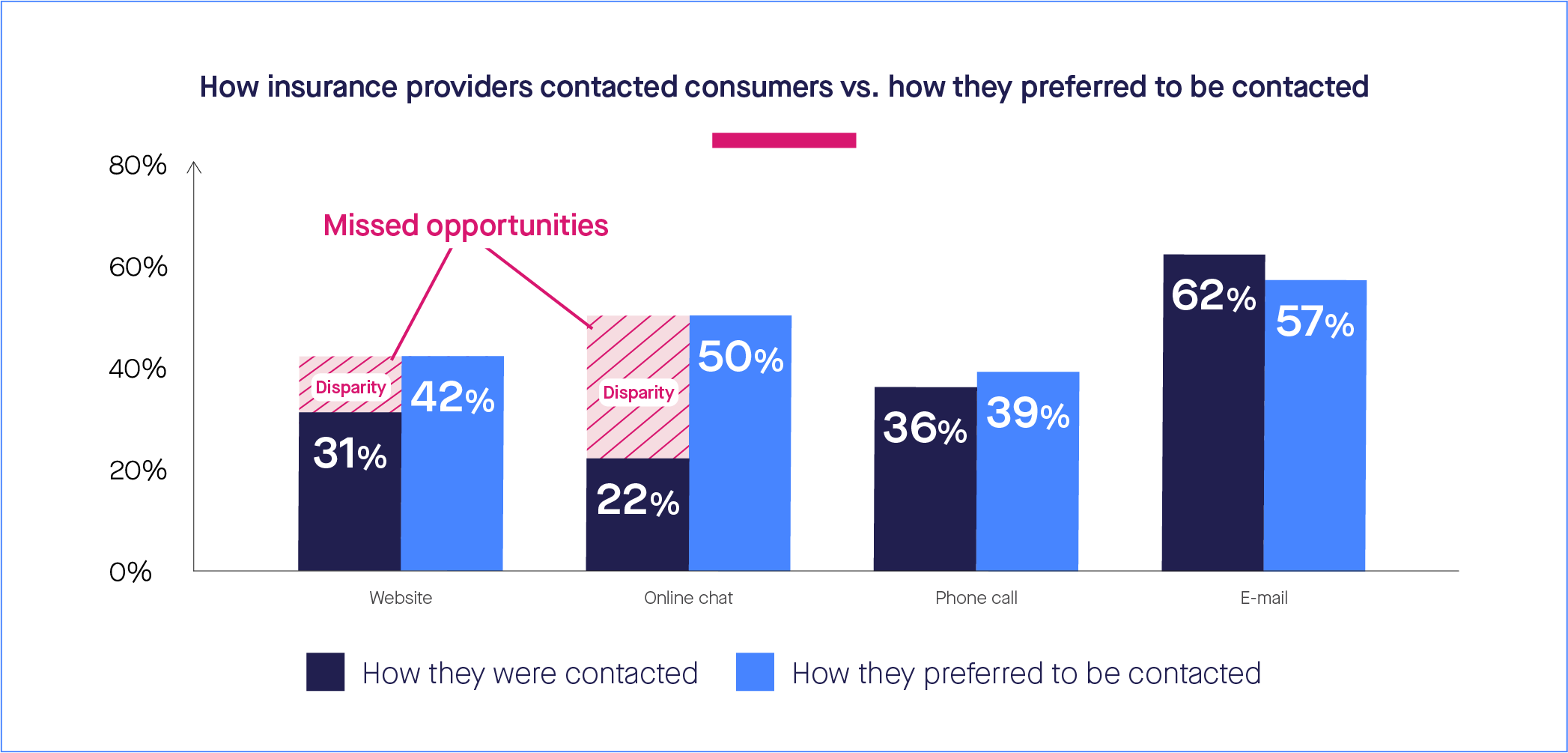

For example, 42% of insurance customers would like information to be communicated to them through their website, yet only 31% of customers actually received relevant information via this channel. In an even more dramatic disparity, 50% of customers would like to communicate with insurance companies through online chat, but only a dismal 22% had the chance to do so.

Overall, a mere 34% of consumers said it was easy for them to communicate with their insurance providers to make modifications to their existing plans. We can easily extrapolate this friction to onboarding, which requires far more information than a modification.

If insurers struggle to provide smooth and reliable remote service to their existing customers who are already in the system, we can only imagine the friction involved with remote onboarding.

Remote capabilities required to expedite policy sales

Unlike current customers, people shopping around for insurance policies are less loyal and rely on ease more than ever. In this saturated insurance market, insurance providers are competing for the attention of these prospective policyholders. Yet fancy advertising campaigns, word of mouth, and even reputation is just the start — if the insurance onboarding process is too cumbersome, customers can easily take their business elsewhere. Therefore, it’s critical that insurance companies invest in intuitive, fully remote onboarding journeys.

By adopting the following capabilities, insurance providers can increase their insurance application completion rates during these remote times — directly boosting sales. They will also benefit from faster deal turnaround time, greater agent productivity, and higher NPS.

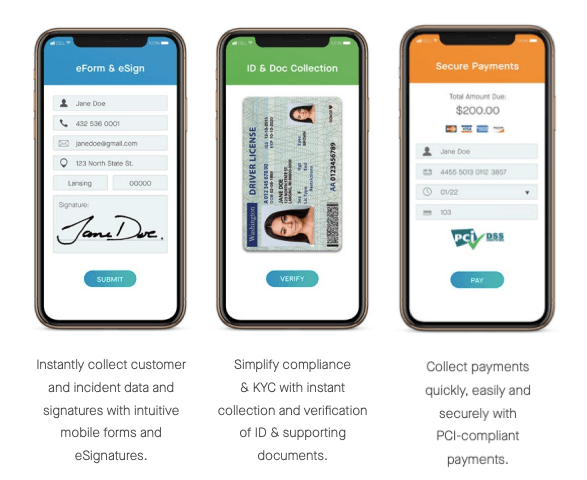

eSignatures

eSignatures are easy and satisfying for customers to complete. Unlike wet signatures, they can simply draw or type their signature, and paste it in the required sections as many times as needed. eSignatures that are optimized for smartphone use are ideal as they allow customers to provide consent without needing computer access or PDF readers.

While increasing completed sales processes is one of the most important benefits of eSignatures, there are also financial savings to be gained: eSignatures slash the transaction costs of policy sales. Recent estimates show that simply digitizing contracts, policies and signatures save $15 dollars per transaction in paper, faxing, scanning costs alone. This saving does not reflect the time and cost saved by not having to chase customers.

2. eForms

eForms streamline form completion, enabling customers to breeze through their insurance applications from start to finish. By using preconfigured, smart eForms, insurers can limit the effort required to complete forms and reduce the rework associated with not-in-good-order (NIGO) documents that result from manual errors on physical paperwork.

eForms use digital rules to reduce the number of fields required to fill, limit the effort required to complete each field, and ensure the data entered conforms with field requirements. As a result, customer information has the highest data integrity: it is complete, legible, and synced with the insurer’s databases.

3. Simplified KYC

Convenience and speed don’t have to be at odds with KYC compliance. The latest technology can actually make digital and remote ID verification more compliant than traditional in-person methods of verifying ID. Customers simply snap a picture of their photo ID, take a selfie using “live” mode, and upload both into the mobile system. An AI-based algorithm automatically scans and compares the two images to verify that there is a match.

This eliminates the sales-killing requirement for customers to scan and email their ID -– or worse, present ID in person.

4. Digital payments

No customer enjoys having to read their credit card information to an insurance agent over the phone. It’s time-consuming and privacy fears always lurk under the surface. Digital PCI-compliant payments via mobile phone improve payment completion rates by up to 20% and eliminate security risks. It’s fast, instant, and convenient — exactly what’s needed in the competitive world of insurance sales.

5. Integrated data

The data sharing and new policy sharing process between insurance brokers, customers, and underwriters should be automated and smooth. Syncing data in real-time eliminates the time elapsed between customer signature and new policy issuance.

6. Focus on CX

Automating and digitizing customer front-end processes enables insurance companies to spend less time pushing paper, and more time on activities that require human input. When insurance agents aren’t bogged down with cumbersome paperwork processes and filing, they are freed up to provide higher-order advice, guidance, and support. And customers who receive this extra value are far more likely to recommend the insurance company to friends and family — another boon for sales.

Sell more insurance policies, faster

With growing consumer interest in purchasing new insurance policies, insurance companies have a unique opportunity to provide a fast and intuitive remote onboarding experience to customers who are currently shopping around.

Lightico offers such an end-to-end frontend solution for insurance providers, including eSignatures, eForms, document collection, digital payments, and ID verification.

Our insurance customers see a tangible impact on their sales and servicing cycles. Madanes Insurance, for example, closed 50% more policies on the first call and slashed its cycle time by 80% by adopting Lightico’s platform. Read the full case study here.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Opportunities to sell new policies may be high, but insurance companies shouldn’t rest on their laurels. Quite the opposite. Customers who wish to purchase policies or modify existing ones face obstacles when it comes to smooth communication with their providers.

For example, 42% of insurance customers would like information to be communicated to them through their website, yet only 31% of customers actually received relevant information via this channel. In an even more dramatic disparity, 50% of customers would like to communicate with insurance companies through online chat, but only a dismal 22% had the chance to do so.

Overall, a mere 34% of consumers said it was easy for them to communicate with their insurance providers to make modifications to their existing plans. We can easily extrapolate this friction to onboarding, which requires far more information than a modification.

If insurers struggle to provide smooth and reliable remote service to their existing customers who are already in the system, we can only imagine the friction involved with remote onboarding.

Opportunities to sell new policies may be high, but insurance companies shouldn’t rest on their laurels. Quite the opposite. Customers who wish to purchase policies or modify existing ones face obstacles when it comes to smooth communication with their providers.

For example, 42% of insurance customers would like information to be communicated to them through their website, yet only 31% of customers actually received relevant information via this channel. In an even more dramatic disparity, 50% of customers would like to communicate with insurance companies through online chat, but only a dismal 22% had the chance to do so.

Overall, a mere 34% of consumers said it was easy for them to communicate with their insurance providers to make modifications to their existing plans. We can easily extrapolate this friction to onboarding, which requires far more information than a modification.

If insurers struggle to provide smooth and reliable remote service to their existing customers who are already in the system, we can only imagine the friction involved with remote onboarding.

Unlike current customers, people shopping around for insurance policies are less loyal and rely on ease more than ever. In this saturated insurance market, insurance providers are competing for the attention of these prospective policyholders. Yet fancy advertising campaigns, word of mouth, and even reputation is just the start — if the insurance onboarding process is too cumbersome, customers can easily take their business elsewhere. Therefore, it’s critical that insurance companies invest in intuitive, fully remote onboarding journeys.

By adopting the following capabilities, insurance providers can increase their insurance application completion rates during these remote times — directly boosting sales. They will also benefit from faster deal turnaround time, greater agent productivity, and higher NPS.

Unlike current customers, people shopping around for insurance policies are less loyal and rely on ease more than ever. In this saturated insurance market, insurance providers are competing for the attention of these prospective policyholders. Yet fancy advertising campaigns, word of mouth, and even reputation is just the start — if the insurance onboarding process is too cumbersome, customers can easily take their business elsewhere. Therefore, it’s critical that insurance companies invest in intuitive, fully remote onboarding journeys.

By adopting the following capabilities, insurance providers can increase their insurance application completion rates during these remote times — directly boosting sales. They will also benefit from faster deal turnaround time, greater agent productivity, and higher NPS.