New Survey: Banks Are Losing Business Due to Bulky Security Measures

By Leor Melamedov

Lightico surveyed 1,329 American consumers to gauge their experiences with online banking, especially as it relates to security and ease of use.

We found that while a majority of customers trust online banking, existing security measures too often lead to access issues. These access issues aren’t just a source of temporary frustration for consumers, but often drive customers away. Cumbersome security doesn’t just mean a diminished customer experience, but lost business opportunities.

Fortunately, security and a clean digital experience no longer need to be at odds thanks to the latest digital security solutions.

No Question About It — Seamless Security Matters in Banking

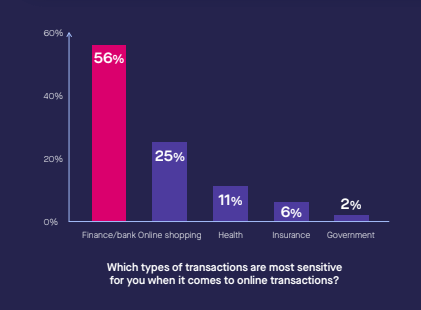

Customers care more about strict security when it comes to online banking than any other online transaction. 56% of the customers we surveyed say banking transactions are the most sensitive type of online transaction they undertake in their daily lives. The second most sensitive area, online shopping, received just 25% of the vote.

This sensitivity rises to even greater levels among high-income individuals, of whom 70% consider banking to be the most sensitive online transaction.

Banks are for the most part doing a good job implementing security measures (although some groups, such as senior citizens, still need more reassurance). Online banking is riddled with features, including antivirus software, firewalls, SSL encryption, and multi-factor authentication designed to safeguard customers’ accounts from data breaches. All of these are features are built to ensure customers’ peace of mind during digital transactions.

High-Friction Security Remains the Norm

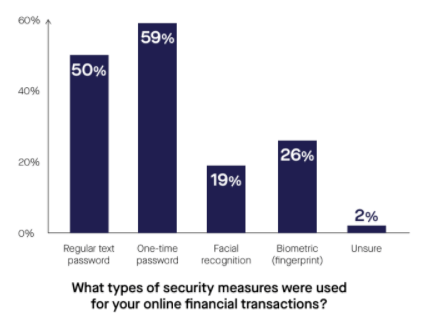

Our survey sought to discover which types of security measures customers encounter the most during online banking sessions, and how it impacts their customer experience.

By and large, consumers most frequently encounter text-based passwords.

One-time passwords (OTPs) are particularly prevalent, with 59% of consumers saying they’ve been asked to use them during their recent online financial transactions. OTPs are advantageous security-wise because they aren’t vulnerable to replay attacks; they are random and work for a single session only.

Regular text passwords are also commonly encountered at a rate of 50%. To lessen the probability of phishing attacks, banks often require customers to change their password every few months. This causes friction as customers must keep track of constantly changing passwords, many of which have complex requirements.

The True Cost of Cumbersome Security

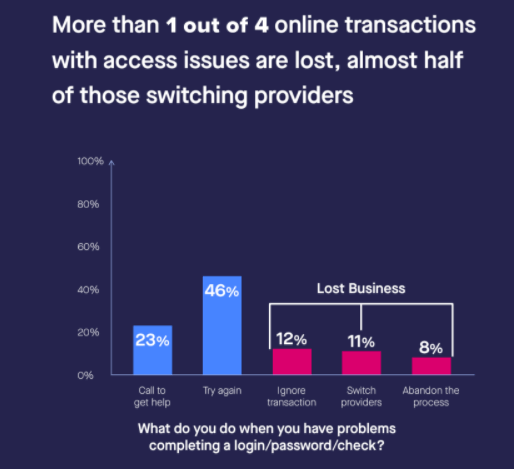

Complicated and ever-changing passwords, along with CAPTCHA and other security checks, are a frequent cause of access issues. For example, customers who fail to correctly enter their password after several attempts may be blocked from trying again within a certain period. And what happens when customers fail to access their accounts?

Nothing good, especially as far as the banks are concerned. 46% of consumers we surveyed say they try again to gain access, though there is likely a limit to their persistence. 23% call a customer support hotline to get help. More concerningly, 12% simply ignore the transaction, 11% switch providers, and 8% abandon the process. In other words, more than one in four online transactions with access issues are lost, with almost half of those leaving the financial institution altogether.

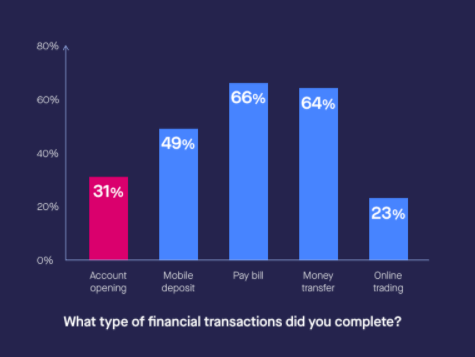

Many of these transactions are related to servicing, such as paying bills, transferring money, making a mobile deposit, or online trading.

But a sizable number of online transactions are connected to opening an account. 31% of consumers surveyed have opened a financial account online in the past three to six months. Customers who face cumbersome security measures during the onboarding process never even get a chance to become paying customers, representing the most painful lost opportunity of all.

Consider that the average banking customer lifetime value is $45,600 (for a customer lifespan of eight years, and both business and personal accounts). Each prospective customer that fails to complete the onboarding process represents $45,600 down the drain. Banking executives seem to be aware that onboarding problems are costing them; a Forrester study found that over 64% of banks report lost revenue due to problems in their onboarding processes. When they scratch the surface, they’ll find that many of these onboarding issues come down to unwieldy security and compliance measures that thwart customers from easily opening accounts and receiving important services.

More Seamless Security Requirements Needed

Of course, banks won’t — and shouldn’t — reduce their commitment to security due to these issues. If customers lose trust in online banking to protect their money, they’ll simply avoid digital channels altogether. The good news is that banks don’t need to choose between security and ease of use.

Many of today’s cutting-edge security measures fit seamlessly into customers’ journeys rather than disrupt them. Yet they go woefully underused. Our survey found that just 26% of banking customers encountered biometric fingerprint logins and a mere 19% used facial recognition in the last three to six months. This is unfortunate because such features promote high levels of security without the hassle and access issues characteristic of text passwords. These types of effortless login systems should be more readily adopted and promoted to customers as the default form of access.

In addition to more intuitive login methods, embedding security features, such as photo ID verification, digital signatures, and PCI-compliant payments, into key touchpoints all enable customers to complete online banking tasks securely and seamlessly.

In this way, non-intrusive security measures allow banks to maintain or even grow their profit margins through digital channels.

Maximizing Opportunities, Minimizing Churn

By moving away from cumbersome security checks, passwords, and requirements, and towards the latest technologies, banks can ensure continued business growth despite the need for increasingly stringent security. In today’s world, security and convenience finally go hand-in-hand.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Customers care more about strict security when it comes to online banking than any other online transaction. 56% of the customers we surveyed say banking transactions are the most sensitive type of online transaction they undertake in their daily lives. The second most sensitive area, online shopping, received just 25% of the vote.

This sensitivity rises to even greater levels among high-income individuals, of whom 70% consider banking to be the most sensitive online transaction.

Customers care more about strict security when it comes to online banking than any other online transaction. 56% of the customers we surveyed say banking transactions are the most sensitive type of online transaction they undertake in their daily lives. The second most sensitive area, online shopping, received just 25% of the vote.

This sensitivity rises to even greater levels among high-income individuals, of whom 70% consider banking to be the most sensitive online transaction.

Banks are for the most part doing a good job implementing security measures (although some groups, such as senior citizens, still need more reassurance). Online banking is riddled with features, including antivirus software, firewalls, SSL encryption, and multi-factor authentication designed to safeguard customers’ accounts from data breaches. All of these are features are built to ensure customers’ peace of mind during digital transactions.

Banks are for the most part doing a good job implementing security measures (although some groups, such as senior citizens, still need more reassurance). Online banking is riddled with features, including antivirus software, firewalls, SSL encryption, and multi-factor authentication designed to safeguard customers’ accounts from data breaches. All of these are features are built to ensure customers’ peace of mind during digital transactions.

Our survey sought to discover which types of security measures customers encounter the most during online banking sessions, and how it impacts their customer experience.

By and large, consumers most frequently encounter text-based passwords.

One-time passwords (OTPs) are particularly prevalent, with 59% of consumers saying they’ve been asked to use them during their recent online financial transactions. OTPs are advantageous security-wise because they aren’t vulnerable to replay attacks; they are random and work for a single session only.

Regular text passwords are also commonly encountered at a rate of 50%. To lessen the probability of phishing attacks, banks often require customers to change their password every few months. This causes friction as customers must keep track of constantly changing passwords, many of which have complex requirements.

Our survey sought to discover which types of security measures customers encounter the most during online banking sessions, and how it impacts their customer experience.

By and large, consumers most frequently encounter text-based passwords.

One-time passwords (OTPs) are particularly prevalent, with 59% of consumers saying they’ve been asked to use them during their recent online financial transactions. OTPs are advantageous security-wise because they aren’t vulnerable to replay attacks; they are random and work for a single session only.

Regular text passwords are also commonly encountered at a rate of 50%. To lessen the probability of phishing attacks, banks often require customers to change their password every few months. This causes friction as customers must keep track of constantly changing passwords, many of which have complex requirements.

Complicated and ever-changing passwords, along with CAPTCHA and other security checks, are a frequent cause of access issues. For example, customers who fail to correctly enter their password after several attempts may be blocked from trying again within a certain period. And what happens when customers fail to access their accounts?

Nothing good, especially as far as the banks are concerned. 46% of consumers we surveyed say they try again to gain access, though there is likely a limit to their persistence. 23% call a customer support hotline to get help. More concerningly, 12% simply ignore the transaction, 11% switch providers, and 8% abandon the process. In other words, more than one in four online transactions with access issues are lost, with almost half of those leaving the financial institution altogether.

Complicated and ever-changing passwords, along with CAPTCHA and other security checks, are a frequent cause of access issues. For example, customers who fail to correctly enter their password after several attempts may be blocked from trying again within a certain period. And what happens when customers fail to access their accounts?

Nothing good, especially as far as the banks are concerned. 46% of consumers we surveyed say they try again to gain access, though there is likely a limit to their persistence. 23% call a customer support hotline to get help. More concerningly, 12% simply ignore the transaction, 11% switch providers, and 8% abandon the process. In other words, more than one in four online transactions with access issues are lost, with almost half of those leaving the financial institution altogether.

Many of these transactions are related to servicing, such as paying bills, transferring money, making a mobile deposit, or online trading.

But a sizable number of online transactions are connected to opening an account. 31% of consumers surveyed have opened a financial account online in the past three to six months. Customers who face cumbersome security measures during the onboarding process never even get a chance to become paying customers, representing the most painful lost opportunity of all.

Consider that the average banking customer lifetime value is $45,600 (for a customer lifespan of eight years, and both business and personal accounts). Each prospective customer that fails to complete the onboarding process represents $45,600 down the drain. Banking executives seem to be aware that onboarding problems are costing them; a Forrester study found that over 64% of banks report lost revenue due to problems in their onboarding processes. When they scratch the surface, they’ll find that many of these onboarding issues come down to unwieldy security and compliance measures that thwart customers from easily opening accounts and receiving important services.

Many of these transactions are related to servicing, such as paying bills, transferring money, making a mobile deposit, or online trading.

But a sizable number of online transactions are connected to opening an account. 31% of consumers surveyed have opened a financial account online in the past three to six months. Customers who face cumbersome security measures during the onboarding process never even get a chance to become paying customers, representing the most painful lost opportunity of all.

Consider that the average banking customer lifetime value is $45,600 (for a customer lifespan of eight years, and both business and personal accounts). Each prospective customer that fails to complete the onboarding process represents $45,600 down the drain. Banking executives seem to be aware that onboarding problems are costing them; a Forrester study found that over 64% of banks report lost revenue due to problems in their onboarding processes. When they scratch the surface, they’ll find that many of these onboarding issues come down to unwieldy security and compliance measures that thwart customers from easily opening accounts and receiving important services.