Low-Mid Income Families Are Under-Served by Inefficient Banks

By Howard Schulman

American banks are fighting a two-front battle. First, they are vying to attract and retain profitable customers. Second, they are rushing to streamline their cost structures to fend off lean, digital banks. To grow their toplines, they are focusing on capturing growing customer segments.

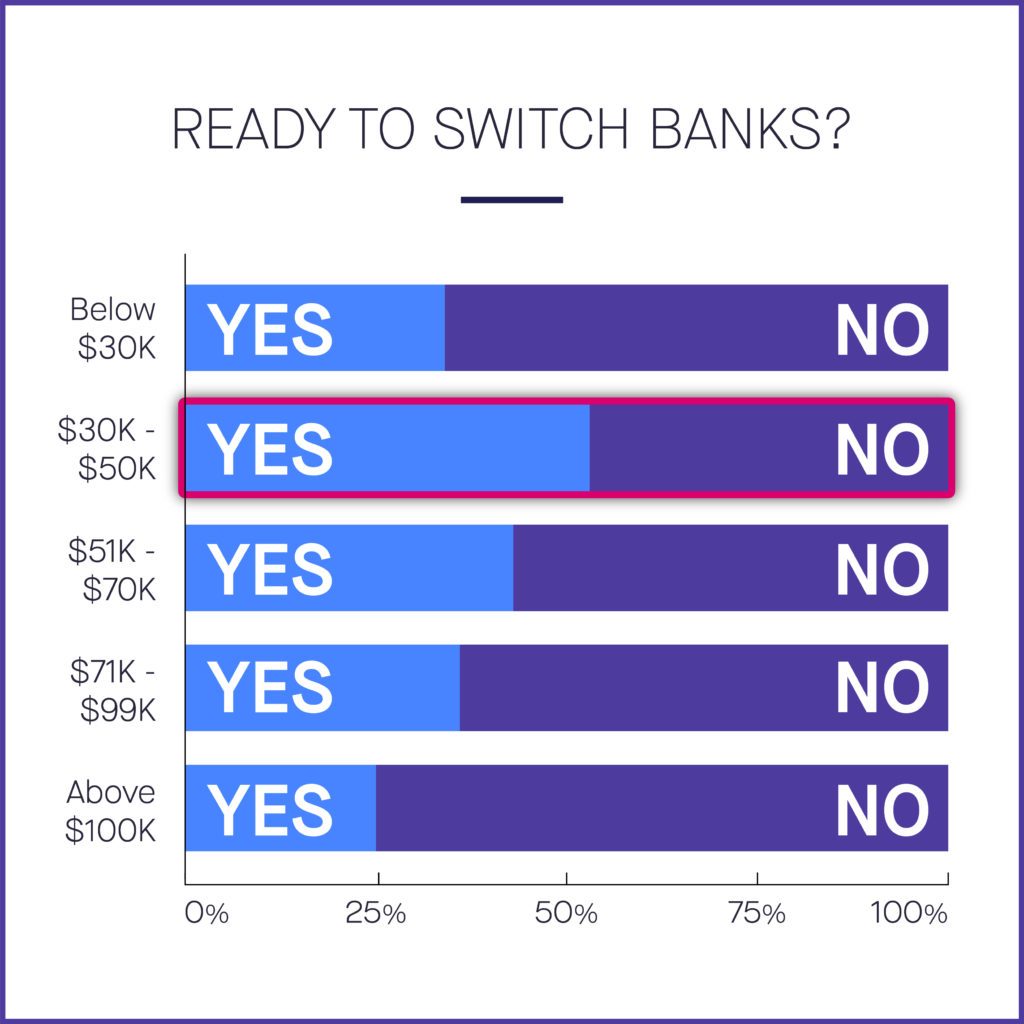

But a new survey shows that traditional banks are actually alienating a key demographic through antiquated customer interactions. In fact, it turns out that the retail banking onboarding experience is so unpleasant and burdensome that key segments are ready to leave them.

A new survey recently commissioned by Lightico details how Americans interact with their bank. It found that low and middle-income Americans (those with income between $30,000 and $50,000) are heavily burdened and frustrated by banking procedures.

This group is fed up with being asked to complete cumbersome banking activities like printing, signing, scanning and mailing paper forms and visiting retail bank branches for transactions. Additionally, they are particularly open to switching to banks that offer simpler, more convenient, mobile and digital experiences.

A Huge Opportunity Needing Digital Intervention

There are 38 million people who fall into this income bracket and are being put off by needless banking bureaucracy.

While banks have risk and regulatory responsibilities, they don't want to alienate low- to mid-income earners. This group also typically represents people at ages when they are still creating financial habits. So welcoming members of this group is a prime growth opportunity for banks, since they can develop relationships with people who could become lifelong clients.

According to the Bureau of Labor Statistics, the median weekly wage for 20-24 year olds in the second quarter of 2019 was $589. That works out to $30,628 annually. This represents more than 9 million people. Among 25-34 year olds, the median weekly wage was $837, or $43,524 per year. That's more than 29 million people.

That's in addition to the statistic that the largest household income group in the U.S. — $50,000 to $74,999 — makes up 17 percent of U.S. citizens.

These groups cover key demographics ranging in age from 20 to 34. While young and still low/mid earners, their potential should be clear for financial institutions. These are people who are making the first major banking decisions of their lives. From first credit cards to bank accounts and student loans to mortgages, these first banking interactions are crucial for their lifelong loyalty.

Banks' Digital Efforts Still Not Digital

Even in today’s digital, on-demand era, banks seem to be paper-bound. This 2019 survey highlights how a large number of bank clients still have to visit a bank branch or print or sign forms. Lightico's survey found this disproportionately affects those in the $30,000 to $50,000 income bracket.

Despite being able to initiate banking processes from a mobile phone or a website, customers are seldom able to complete any but the simplest transactions digitally and instantly.

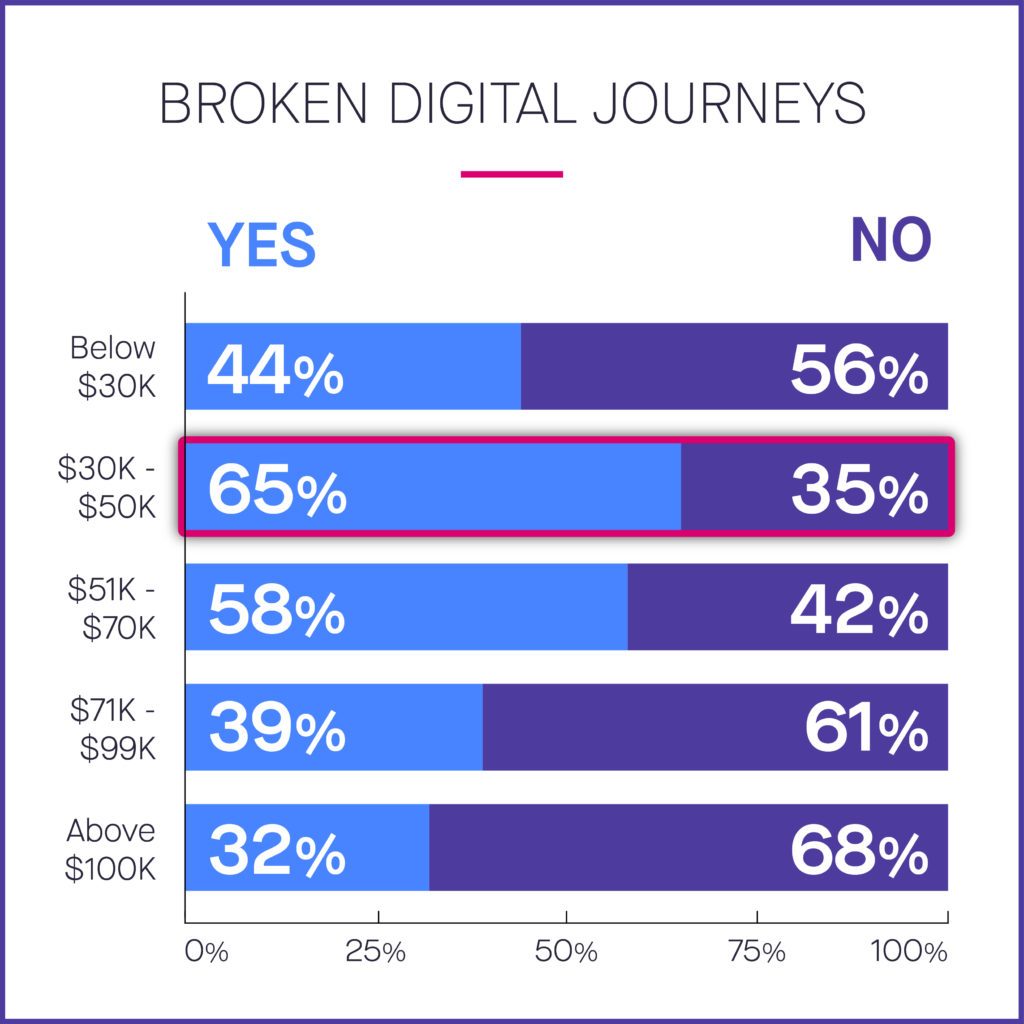

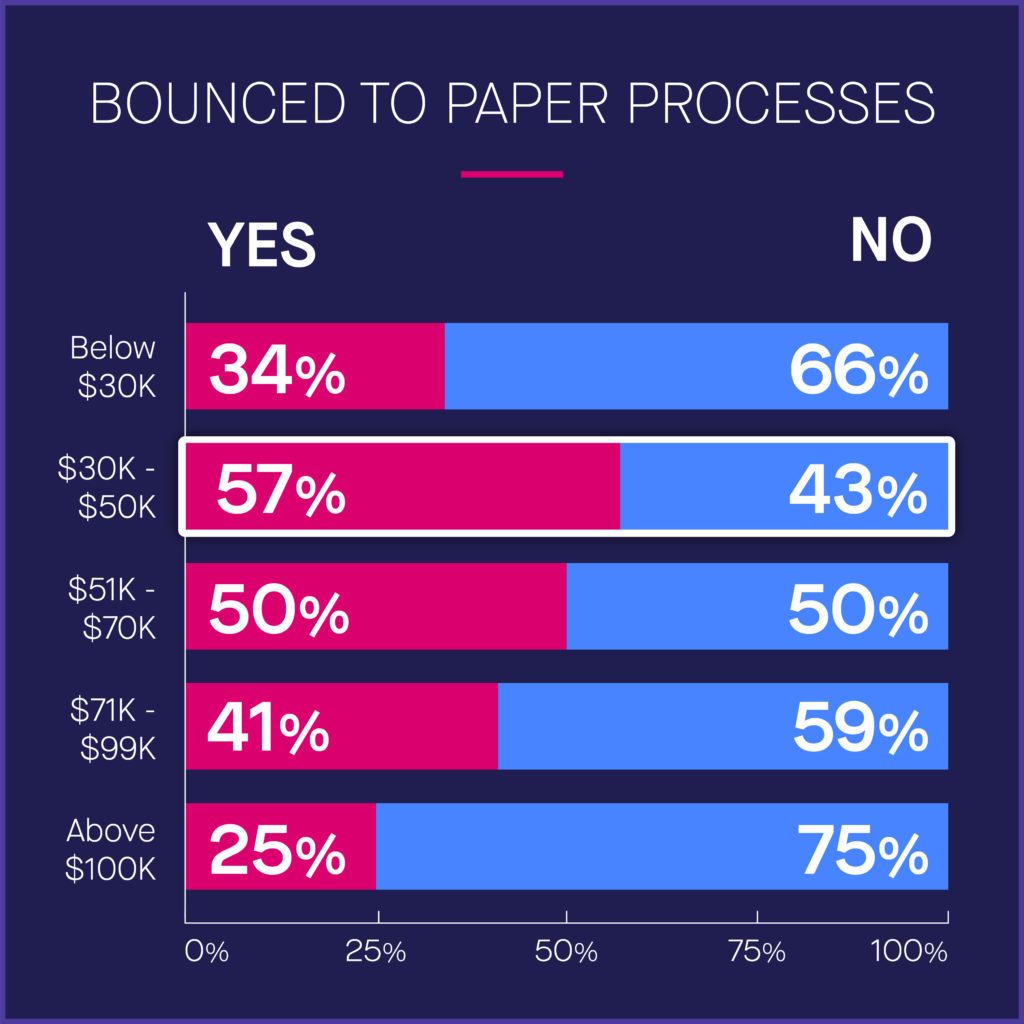

To illustrate the point, almost 65 percent of retail banking transactions were redirected to a physical location from an online banking transaction. And more than 57 percent of digital banking processes were bounced to clumsy print, scan, and email processes.

That percentage was higher than any other income bracket - more than twice those earning $100,000 a year or more. It's especially notable since it happened during a digital process — when customers don't expect to have to visit a branch, or be in an office environment.

This Segment Won’t Stand for Clumsy Banking

So far, these groups have not been too happy with leading banks processes. Lightico's survey found that among the $30,000 to $50,000 income earners, digitized, mobile and instant processes are key to banking satisfaction.

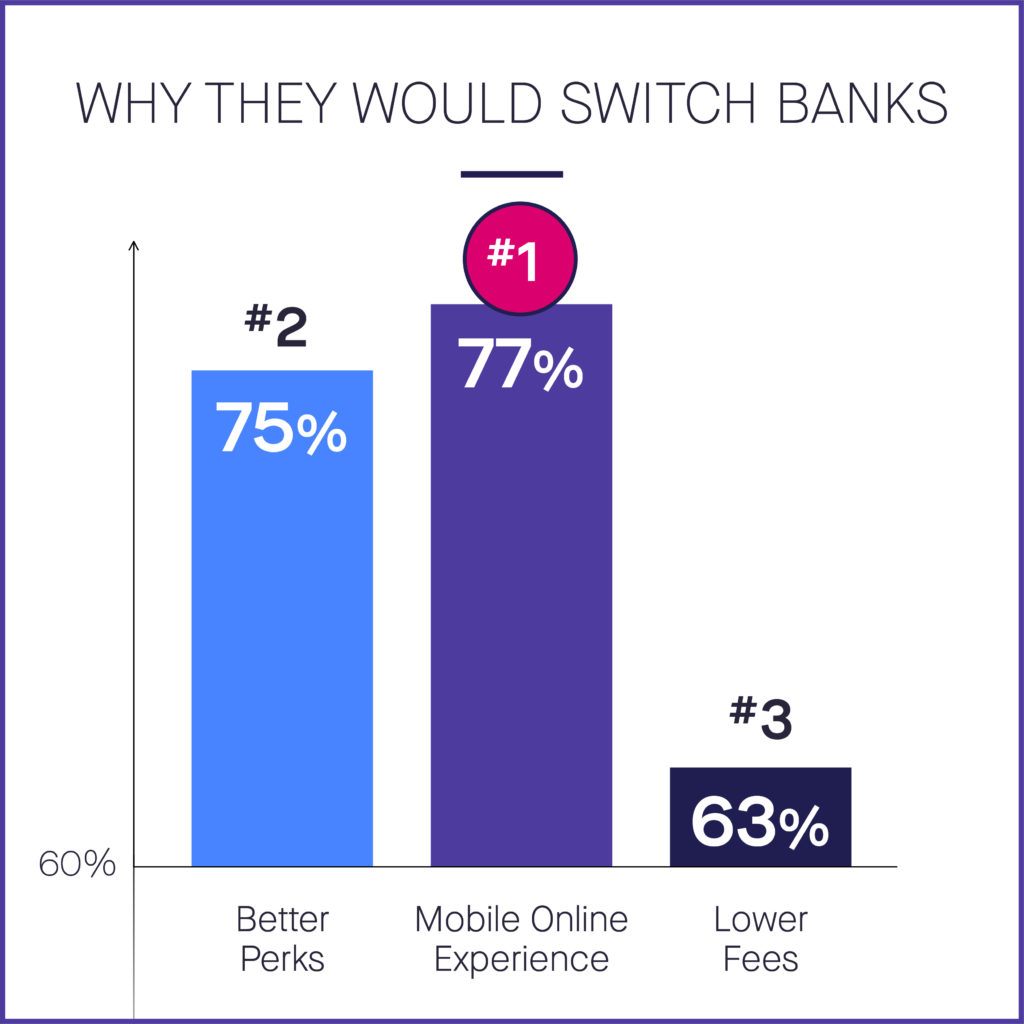

In fact, a great online and/or mobile experience was the number one factor that would lead members of these groups to switch banks.

That factor was cited by almost 77 percent of respondents, beating out better perks at 75 percent and even better customer service at almost 63 percent.

In short, it means these important groups are ready to leave — to another bank that makes it easier for them to complete transactions online.

Why Customers Are Being Mishandled

Historically, many of these digital disconnects could be blamed on regulation. Banks have a responsibility to know their customers (KYC). But even strict federal regulations don't necessarily require the amount of paper that often accompanies client onboarding. A bank must have a customer identification program in place to gather minimum information like name, date of birth, address and identification number.

While Fiserv companies must verify that information — their capturing and review of customer information does not have to happen offline. Nevertheless, banks often ask new customers to go through extra KYC steps. That's especially the case if they don't have a credit history or have never banked at another institution.

Key Banking Digital Interactions

Fortunately, there are a number of ways banks can reduce the burdens that create undue barriers for new clients. Technology can help customers onboard and transact efficiently. Simplified digital customer interactions can elevate the client experience while allowing banks to fulfill their compliance responsibilities.

Here are some ways this is being achieved:

Intuitive mobile solutions. Not all customers have banking apps and not all banking apps are fully digital or intuitive. Banks need to design experiences that are fully digital and allow for customers to navigate via the mobile web — not applications. As institutions continue to digitize and simplify, they will reap the loyalty of their customers: the more customer interactions happen online, the more new clients tend to be satisfied with their banking experience.

Digital ID verification. Banks can often fulfill their Know Your Customer and anti-money laundering requirements with digital ID checks either by KBA, OTP or photo ID verification. This makes things easier for clients, quicker for banks, while still meeting ethical and legal standards.

Smart eForms. At one time, the PDF was the standard of digital document technology. Now, new solutions make online document completion even easier. Smart eForms have pre-fill capabilities from bank CRMs and auto-fill options for new clients.

Instant digital signatures. Consent is an essential part of banking transactions, but it doesn't need to happen with pen and paper. Banks can send new or existing clients a link through email that leads to a page where they can give instant, legally-binding consent through a digital signature.

Real-time access to sales reps. Bank customers also need assistance from time to time. That's why customer service ranked so highly as a motivating factor to switch financial institutions. Having real people on hand to answer questions and troubleshoot issues can improve the onboarding experience.

Security protocols.Secure APIs ensure the online banking experience is not only efficient, but highly secure. That way, new and existing customers don't have to worry about their personal data being compromised.

Together, these strategies make banking simple for new banking clients. It gives them a positive onboarding experience that can engender loyalty for years to come.

A New Opportunity To Better Serve Low-Mid Income Earners

Banks have a responsibility to know their customers, and secure the banks regulatory obligations. Nonetheless, when banks ask low to mid income demographic customers to go through extra steps, such as in branch visits, or printing and documents, they risk creating a poor customer experience, thereby potentially losing those customers.

Like Gen Z and Millennials (who are also represented in the low to mid level income), low to mid income customers will jump at the chance to be better served by fully digitally banks.

It’s critical for banks to focus their growth efforts on large and growing consumer segments. With the burgeoning opportunity of low-mid income households, there are obvious digital interventions that can enable forward-thinking banks to optimize the customer experience and provide full regulatory compliance.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Despite being able to initiate banking processes from a mobile phone or a website, customers are seldom able to complete any but the simplest transactions digitally and instantly.

To illustrate the point, almost 65 percent of retail banking transactions were redirected to a physical location from an online banking transaction. And more than 57 percent of digital banking processes were bounced to clumsy print, scan, and email processes.

Despite being able to initiate banking processes from a mobile phone or a website, customers are seldom able to complete any but the simplest transactions digitally and instantly.

To illustrate the point, almost 65 percent of retail banking transactions were redirected to a physical location from an online banking transaction. And more than 57 percent of digital banking processes were bounced to clumsy print, scan, and email processes.

That percentage was higher than any other income bracket - more than twice those earning $100,000 a year or more. It's especially notable since it happened during a digital process — when customers don't expect to have to visit a branch, or be in an office environment.

That percentage was higher than any other income bracket - more than twice those earning $100,000 a year or more. It's especially notable since it happened during a digital process — when customers don't expect to have to visit a branch, or be in an office environment.

In fact, a great online and/or mobile experience was the number one factor that would lead members of these groups to switch banks.

That factor was cited by almost 77 percent of respondents, beating out better perks at 75 percent and even better customer service at almost 63 percent.

In short, it means these important groups are ready to leave — to another bank that makes it easier for them to complete transactions online.

In fact, a great online and/or mobile experience was the number one factor that would lead members of these groups to switch banks.

That factor was cited by almost 77 percent of respondents, beating out better perks at 75 percent and even better customer service at almost 63 percent.

In short, it means these important groups are ready to leave — to another bank that makes it easier for them to complete transactions online.