Banks and financial institutions today put tremendous focus on their processes for detecting and preventing fraud — but too often they ignore the customer impact of fraud claims.

Consider what goes on in the heart and mind of a banking customer when they first suspect they may be a victim of fraud. Many if not most of us have already been there as consumers: You notice that cringe-worthy minus right next to a troubling transaction amount or withdrawal while checking your banking account summary. Naturally, your anxiety spikes up in an instant. And that anxiety won’t completely subside until you contact your bank and feel assured that they are working on resolving the problem and getting you back your money.

That’s the mindset of a customer when they first contact their bank or financial institution to report a fraud complaint. How their bank manages the fraud claim process is pivotal to either extinguishing that fire and ensuring customer trust — or fueling it even further and risking burning the relationship with their customers for good.

So while preventing fraud is vital for banks and financial institutions who are constantly handling high-value deals or transactions, managing incoming customer fraud complaints requires a much more delicate, transparent, and expeditious approach.

Digital Silos Are Slowing Down the Fraud Resolution Process

Banks and financial institutions today have already poured money into solutions that help digitize different stages of the fraud claims process on both the front and back end, such as ID verification, digital signatures, eforms, and solutions that help customers upload supporting documents to aid fraud investigation.

But there are two major roadblocks that keep these investments from delivering the speed and convenience banks need to quell the fire of fraud anxiety and resolve these claims swiftly: Digital Silos and legacy processes.

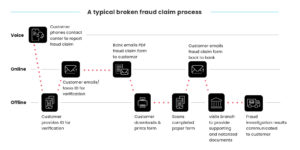

Rolling out disparate point solutions to patch together all steps of the fraud claims journey is like expecting people to know how to escape a building in case of a fire without showing them the way to the nearest fire escape.

That’s what digital silos do to the fraud claims process. Systems for e-signatures, eForms, ID verification, and document collection don't talk to one another, prolonging and complicating the entire fraud claim process.

For example, a customer may connect with the bank’s contact center to report a fraud complaint, but then they may be directed to open an email and fill out and sign lengthy fraud claims form.

Many steps during the fraud claim process require separate forms and documents, while others require uploading documents and verifying the customer’s ID. None of these various siloed solutions talk to each other, necessitating multiple and uncomfortable steps for the customer.

Legacy Processes Are Risking Customer Churn

Being forced to use manual, legacy processes for e-signatures and eForms also add to this choppy customer journey - all at a time where insecurity and stress are running high.

Consumers are often on-the-go and have trouble making sense of a clunky and crowded PDF-based document from their mobile device, and they’re likely to have questions on how to fill out different sections before signing away.

Many customers will call the contact center right back and ask for live assistance - speaking to an agent while toggling back and forth to the small and hard-to-read PDF on their smartphone.

Then, they’re usually asked to download an e-signature app from the play store just for this specific moment so they can sign the form and get it back to the agent.

If they’re not comfortable, they’ll drop everything and pay a visit to the branch where they can vent their frustration,but it doesn’t end there. Completing requirements of their fraud claim means they’ll need to find transaction records and any other documents to help make their claim and start the investigation. For some transactions, documents may well need to be notarized, requiring another visit to a notary public.

This disjointed workflow hardly alleviates stress for a customer hoping to resolve their fraud claim ASAP. Customers that are frustrated by being bounced from channel to channel like a ping pong ball may throw up their arms and stop engaging for days or weeks, delaying the investigation and completion of the process for both sides.

These digitally incomplete journeys delay the bank’s ability to efficiently resolve the customer’s fraud claim, prolonging turnaround times, and risking false starts and open cases that lag. Worse yet, they can lead to service-level issues and escalate to legal disputes and regulatory complaints.

And looking at the larger picture, a negative fraud claim experience can and will often result in customer churn and lowered NPS for banks and financial institutions.

Simplifying & Digitizing the Fraud Claim Process

Getting your customers through the fraud claims process quickly, efficiently, and painlessly as possible requires connecting all steps of that journey seamlessly into one end-to-end experience.

A Digital Completion solution is designed to do just that, by integrating all customer interactions with the bank, all documents that need to filled and signed, and all supporting documents and records they need to provide to eliminate gaps in turnaround time and empower banks with all of the information they need to investigate a fraud claim and solve it quickly.

Instead of jumping from phone call, to email, to branch, downloading apps for one incident, and filling out and signing PDF forms, all of these customer-facing steps are combined into one simple and intuitive session guiding them from start to finish.

Customers instead can simply click on an SMS link, and complete forms and upload documents in an interactive session designed for mobile. Just as importantly, they are guided with live agent assistance throughout, walking them through every step of the way until the process is complete.

The time it takes to complete those choppy old fraud claim journeys? That’s dramatically chopped, too. Banks and financial institutions that are leveraging digitally completed journeys are seeing:

Completion rates increase by 25%

Fraud claims resolved 67% faster

60% fewer touchpoints

Improving these key banking KPIs not only helps banks cut expenses and resources wasted on administrative tasks, it gives their customers the fast and convenient experience they need, right at the time they need it to calm stress and anxiety and trust their bank is equipped to resolve their fraud claim with as little headache as possible.

That trust and confidence pays off and helps banks and financial institutions strengthen customer loyalty and grow lifetime value with their customers.

Ready to Deliver Faster, Compliant Customer Journeys?

Reduce manual work, strengthen compliance, and improve customer experience.

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

The time it takes to complete those choppy old fraud claim journeys? That’s dramatically chopped, too. Banks and financial institutions that are leveraging digitally completed journeys are seeing:

The time it takes to complete those choppy old fraud claim journeys? That’s dramatically chopped, too. Banks and financial institutions that are leveraging digitally completed journeys are seeing: